WYNN - Wynn Resorts Stock: Headed For Solid Q1 2024 As Golden Calendar Looms

2024-01-17 18:19:59 ET

Summary

- Wynn Resorts is undervalued by 25% and has significant growth potential in the premium mass segment of the Macau market.

- Wynn's debt profile is manageable and the company is expected to have strong earnings in 1Q24.

- Wynn will benefit from a positive gaming calendar in both Las Vegas and Macau, including the Super Bowl and Chinese New Year, which will drive record-breaking revenue.

Above: Wow the customers and keep wowing them to build a fortress in the upscale customer segment no matter where you develop--Steve Wynn.

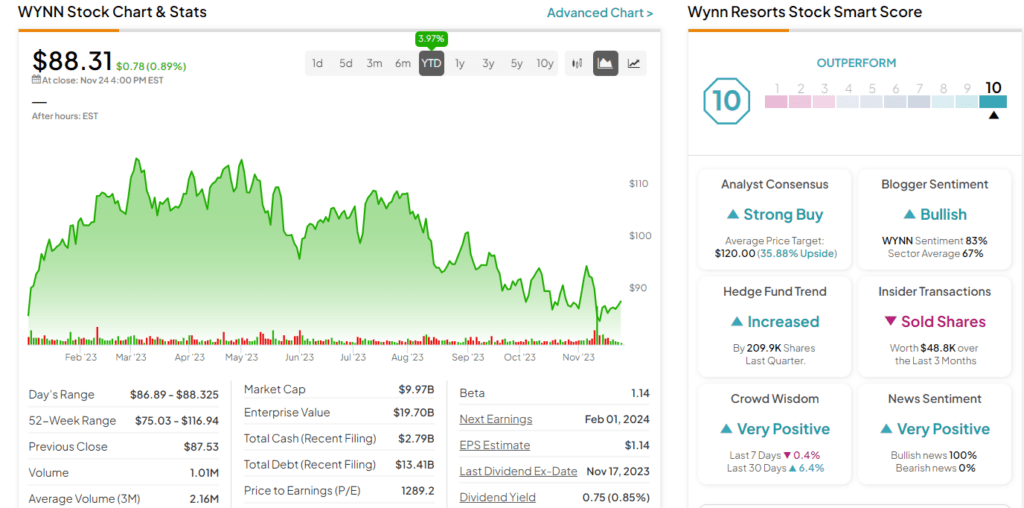

Timeline : On November 27, we posted our view of Wynn Resorts, Limited ( WYNN ) on Seeking Alpha, a day on which the stock traded at $86. Our call then: The stock is undervalued. Our price target ("PT") projected by the end of Q1 2024 was $120. Intrinsic value estimates by alpha spread were: Best case $221; base case $148; worse case $123. Thus Wynn is undervalued by 25% at this point.

But the projected terminal 5 year value by AS does not factor in possible dilution by the rapid growth of other Asian markets competitive for China tourists to Macau’s post covid cycle such as the Philippines and Cambodia. Within five years, add the possibility of Thailand entering the sector as well.

At writing, Wynn trades at $94, or $12 higher, indicating the stock still has much runway ahead if you buy my premise.

{kind=link}

Premise of the investment: What’s changed

The outlook for the macro China economy is getting darker by the month. Some sources are dropping estimates of 2024 GNP growth to as low as 2%. Ironically, as we sifted through our archives accumulated since our years in gaming c-suites that factor macro cycles gaming win variants, we found that China-based GGR reveals this phenomenon: VIP segment play understandably slows. (In addition to declining junket activity already in place.) When this happens, we discovered, there is a clear upside move in the premium mass sector that replaces VIP and, in fact, expands total win.

That results from VIPs downscaling gaming budgets ,as well as the fact that upscale segment of mass play does not appear to be impacted negatively from macro China economic slowdowns.

Wynn’s strong suit is and has always had a fortress position in the premium mass segment.

Taking this into account, we believe Wynn will achieve a 16.7% share of the Macau market in 2024. The Macau gaming industry EBITDA grew by 6% in this past 4Q23 to $1.95b. Wynn EBITDA margin hit 28.5%, up y/y.

google

Above: A good entry point now before Q1 2024 possible strong earnings beats due to both Vegas and Macau gaming calendars hugging.

Capsule debt profile

Wynn’s debt profile is seen by some hedgies we spoke to in connection with this article as giving something of a negative cast to the stock regardless of the current entry point. It is indeed heavy, but not daunting in our view. It will comfortably meet a capex forward spend estimated at $400m in Macau:

Total debt: $11.6b down from $12.4b in 2020.

Cash on hand: $3.5b overall stable for last three years.

Current ratio: 2.66 within a range we believe that is comfortable with maturities going forward.

January to date: We have looked at this month to date as a possible precursor of what to expect in Q1 2024 where we expect our PT to hit close or at $120. Morgan’s latest estimate of this month’s GGR is $2.23b during the first 14 days. The average higher slice of the mass segment which Wynn has marketed to post covid is up 105% to 110% above the pace of GGR in baseline 2019.

Wynn Las Vegas continues to overperform. We are looking for ~$533m in 2023 EBITDA for Wynn Las Vegas. On a relative scaled basis, Wynn will continue to be the highest earning properties in Las Vegas this year. We are looking for the Vegas properties to produce ~$700n in free cash flow ("FCF") for 2024.

This reflects that Las Vegas has had a record-breaking year in gaming, with Nevada officials posting that the state won $15.1b from gamblers in 2023.

Double-barreled catalysts weeks ahead in Vegas and Macau

As we have already noted in our piece on MGM (SA Jan 10 TH ), both operators will benefit from an explosively positive gaming calendar just ahead. MGM will also see a huge spike in its BetMGM sports betting platform due to SUPER BOWL action that Wynn will not on its lower revenue WynnBet site.

However, Wynn’s market share in Macau is considerably larger than MGM. For that reason, we see revenue potential offsetting with Wynn Macau enjoying ~a 6.5% lead in market share there. However, MGM’s Vegas footprint’s larger room scale is among market share leaders in Vegas. Our point here that both will benefit as will Caesars Entertainment (CZR) and others from this knockout historic calendar aligned with their strengths. You have a meeting of forces not likely to be repeated anytime soon: Super Bowl in town, betting on game, big time A-List entertainment events, 100% hotel occupancy, and visitor numbers potentially off the charts.

Here’s the golden gaming calendar: The Super Bowl game February 11th, first time ever in Las Vegas expected to draw as many as 350,000 to 400,00 visitors. Hotels will hit as close to 100% occupancy as possible.

Allegiant stadium sold out with 65,000 fans.

Chinese New Year: February 10 th . Macau expects record breaking arrivals between 150,000 and 200,000 celebrants.

Assuming no unusually low hold percentages on the baccarat game in both markets, expect record breaking revenue streams for the month of February that will form the basis for outstanding Q1 2024 operating results for Wynn.

{kind=link}

Above: In general, a Wynn hotel standard room outclasses and outsizes most competitors and justifies a higher average rate.

Wynn continues to trade at a premium above peers long after the departure of Wynn himself in 2018

Ever since the opening of the old Golden Nugget casino hotel in Atlantic City in 1980, shares of the company have traded at a premium due to Wall Street’s conviction that Steve Wynn personally was a brilliant innovator.

The AC Nugget outperformed us all despite its small casino, its outlier location and relatively over the top luxe design that best mimicked a time travel visit to the glamour of old Las Vegas. Thus literally until the appearance of the super luxe Borgata in 2003, the Wynn property was the only one where customers had a sense of a Vegas visit during their trips there.

In 1987, Wynn sold the Nugget to the old Bally Park Place (defending against a greenmail assault) for $440m, leaving the town to build what became the Vegas Mirage in 1990. In ’87, I had moved from the Caesars c-suite to Bally's Park Place, where I was immediately dispatched to the rechristened Bally's Grand to bring a new management culture to a property.

Bally's management felt that under Wynn the property had been overindulgent in comping unworthy customers and spending far too much on operational amenities and food costs.

I told the CEO this was wrong-headed thinking, as the Nugget customers expected no change to their favorite casinos due to the acquisition by Park Place. The CEO disagreed and told me I’d find that on balance our EBITDA would rise and the customer base would be stable.

He was wrong.

Long after, when I had moved on to the Senior VP position at Trump Taj Mahal, I met with Steven Wynn during a business visit to Vegas. We had a lunch and talked old times in AC. I joked about how Bally austerity had changed the image of what had been the Nugget. “I remember players calling me complaining that the soap in the spa was 'cheapo hotel soap.'”

The complaints sprung from a Bally's edict to reduce the cost of everything to just manageable standards for good hotels. Among the victims was the French milled soap we used in the spa, much of which was continually pilfered by players, many of whom had enough personal wealth to buy any soap factory in the world. I shared this memory with Wynn.

Paraphrased, from memory, his reply:

“It’s one of those little things that accumulate in players heads which builds an entire image of a place. You do not fool with that. It tells who you are and what you think of them. The more soap these players stole, the better the customers felt about our joint back home. There was a direct path from what we overdid to EBITDA that beat the pants off our competitors.”

The above exchange tells more about why Wynn shares still consistently trade at a premium above peers than ten pages of charts and diagrams issued from banks and analysts.

Wynn management today is still dining out on that message, as it were. That’s over 40 years ago.

There was a hiccup around the turn of the century, when Wynn’s wolfing down of multibillion dollar French impressionist art caused Wall Street fans to turn sour on the stock and paved the way for Kirk Kerkorian to swoop in and buy the Mirage for relative peanuts. He went on to build the Bellagio.

I bought heavily into Wynn shares $18 and created a fund that sent my three sons to top colleges courtesy of Wynn returns.

Wynn learned his lesson. Ever since, the company has led the profit parade in Vegas and is first among peers in the upscale segment in Macau. Its Encore Boston property has largely overcome initial deficiencies in its slot business.

The business model created by Wynn from the late 1970s remains largely intact since his departure in 2018. No one is suggesting that he is not missed to a degree, but the succession of operators from the c-suite on down have borne out the durability of the business model created decades ago.

Overall, we are undaunted by the prospect of the macro China economy’s sharp decline that could have a major impact on forward Macau GGR. We also believe that the spread between where Wynn Resorts, Limited stock currently trades and the prospects just ahead with their catalysts, forms the basis for our BUY guidance, looking at ~a 25% current undervaluation.

For further details see:

Wynn Resorts Stock: Headed For Solid Q1 2024 As Golden Calendar Looms