WYNN - Wynn Resorts: Strategic Withdraw From Digital Gaming

2023-08-14 02:37:31 ET

Summary

- Wynn Resorts has decided to pull back from the online gaming market due to low profitability and slower growth compared to its brick-and-mortar operations.

- The company's core business has shown resilience and growth, with a significant increase in revenue and a turn towards profitability.

- While a solid business the current valuation doesn't provide enough upside for us and we list it as a 'Hold'

Wynn Resorts (WYNN), a brand synonymous with opulence and top-tier entertainment, ventured into the dynamic world of online gaming through WynnBET, seeking to replicate their offline success in the burgeoning digital arena. Recently they announced their pullback in that market. While this shift might appear counterintuitive given the momentum of online gaming, a closer look at their financials and operational metrics provides clarity. The core business of Wynn Resorts, particularly its brick-and-mortar operations, has shown remarkable resilience and growth. Contrastingly, the digital venture, while promising, has lagged in profitability and has grown at a relatively slower pace. In light of these dynamics, we have categorized Wynn Resorts as a 'Hold'. This stance is driven by our analysis that while the company has considerable strengths and potential, its current valuation seems to fully encompass these positives, leaving limited upside at the present price point. In the subsequent sections, we delve deeper into the intricacies of Wynn's operations, financial health, and strategic moves, providing a comprehensive overview to inform investment decisions.

Wynn's Digital Endeavor: A Brief Affair?

Wynn Resorts, known for its luxury, unmatched hospitality, and premier entertainment, took a leap into the digital realm with WynnBET. Their objective wasn't just to bring their signature luxury experience online but also to seize a share of the surging online gaming market. With established players like MGM and Caesars already in the scene, WynnBET's introduction was seen as a well-timed move to help capitalize on the market trends.

However, in a surprising turn, the company has decided to shutter its operations in several states, citing extensive marketing costs and more lucrative global investment avenues. Now, with Wynn Resorts retracting its digital footprint in select jurisdictions, the future of WynnBET, especially in states like New York and Michigan, remains uncertain. While they will continue to provide the app in the states of Nevada and Massachusetts (both state where they currently have resorts)

While this may seem like a shock considering PENN’s recent ESPN announcement I believe the move makes sense. The division was not profitable and had shown minimal growth with revenue climbing from $43 Million in the first half of 2022 to $46.4 Million in the first half of 2023 a growth rate of ~7.1% while their casino revenues jumped dramatically with a 154% YoY jump. Focusing on their core business instead of negative adjusted earnings of the Wynn Interactive seems like a smart move especially with larger players moving in to the space.

Q2 Overview

In the midst of the excitement surrounding WynnBET, it's crucial to recognize the primary revenue sources for Wynn Resorts. Their latest financial data underscores a revenue upswing, moving from $909 million in Q2 2022 to a whopping $1.6 billion in Q2 2023. Furthermore, their transition from a $130 million loss in Q2 2022 to a net profit of $105 million in Q2 2023 signals a robust turn towards profitability.

In the first six months of 2023, they allocated dividends amounting to $28.7 million. Given a net income of $129 million, this represents a 22% payout ratio. It's noteworthy that a significant chunk, $128 million to be precise, of this half-year's net income was realized in the second quarter alone. The quarter also saw a stock buyback worth $12 million. Additionally, they restructured their debt portfolio by issuing $1.2 billion in long-term debt, using it to settle $1.1 billion of existing obligations, effectively refinancing their debt.

Although there's a noticeable surge in revenues, operating expenses have also escalated, moving from $961 million to $1.35 billion. However, it's essential to highlight that while revenues soared by 75%, expenses only climbed by 40%. This demonstrates the company's significant operational leverage. Managing costs amid such a demand surge can be daunting. However, as the surge from reopening stabilizes, we anticipate an expansion in margins, especially given their focus on upscale clientele.

For a property-centric enterprise like Wynn, high interest expenses are expected. The dynamics of rising interest rates present both opportunities and challenges. The interest expense increased year-over-year from $154 million to $190 million. However, a silver lining is seen in the interest income which jumped from $2.7 million to $44.1 million, effectively countering the surge in interest expense with a boost in interest income.

How we view the business

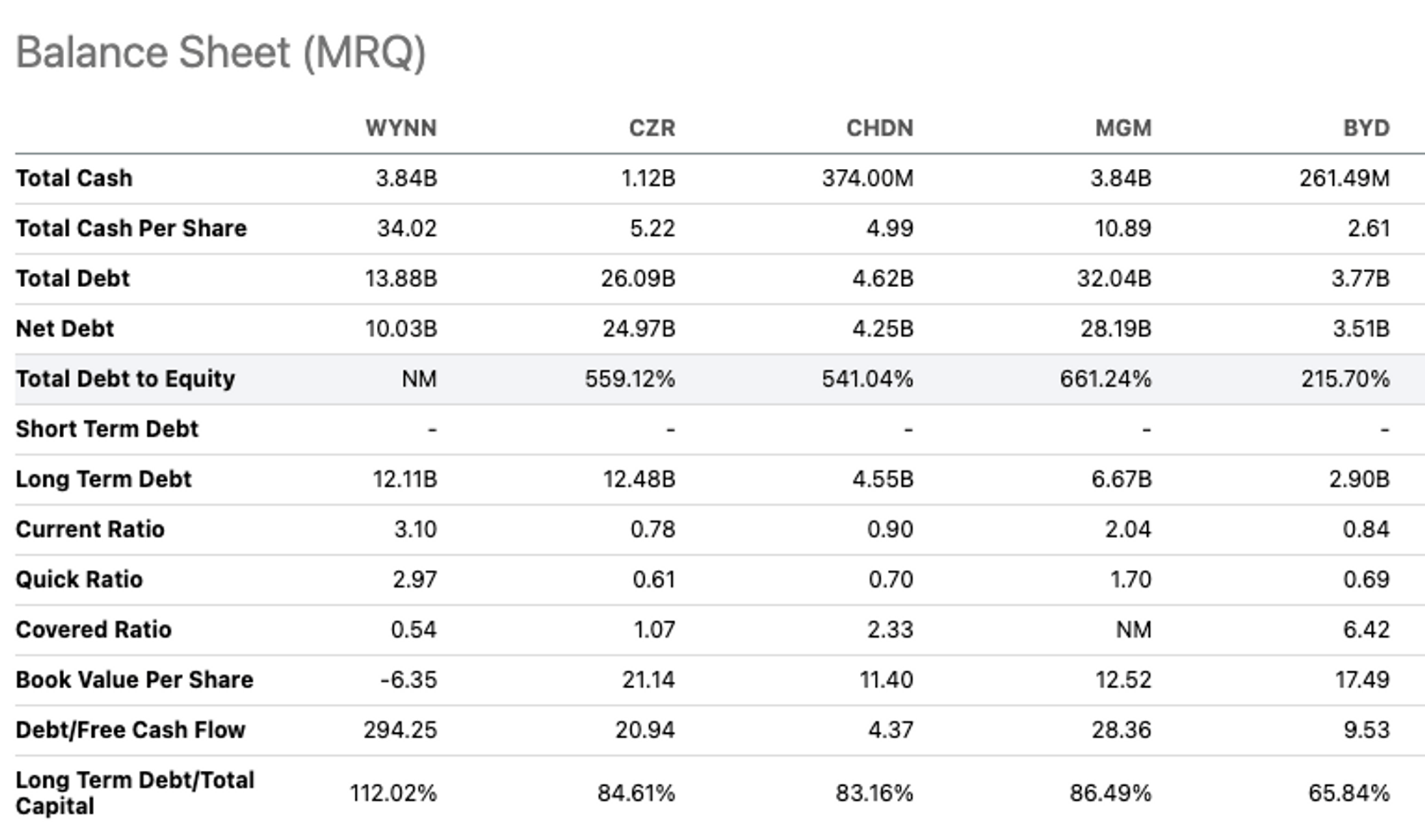

Shifting focus from online gaming appears to be a strategic decision, in our perspective. WynnBET, while a novel venture, was a minor and costly endeavor in comparison to Wynn's core operations, contributing to less than 3% of their revenue. Operating this non-profitable segment in a fiercely competitive market did not seem sustainable, making their decision to exit understandable. The resurgence of Chinese visitors to Macau casinos significantly bolstered Wynn's revenue and earnings in the first half of the year. However, the costs associated with reopening are a challenge to streamline. Wynn's strategy to attract VIP players to both Macau and Vegas in the latter half of the year will likely be pivotal for their operational success. Their financial health seems robust, with a cash reserve of $3.6 billion set against a long-term debt and lease obligation of $13.7 billion. The recent announcement about the tender offer for their 2025 Notes indicates their intent to refinance and reduce outstanding debt.

From an investor's standpoint, we appreciate when a company returns capital through share buybacks, dividends, or by judiciously reinvesting in growth or debt reduction. Currently, Wynn is allocating 22% of its payout ratio towards dividends and investing 11.4% of net income in share repurchases, meaning about 33% of net income is directly benefiting investors. Given the current consensus EPS for 2023 is approximately $3.30, we anticipate dividends to stay around $.25 for the remaining two quarters.

{kind=link}

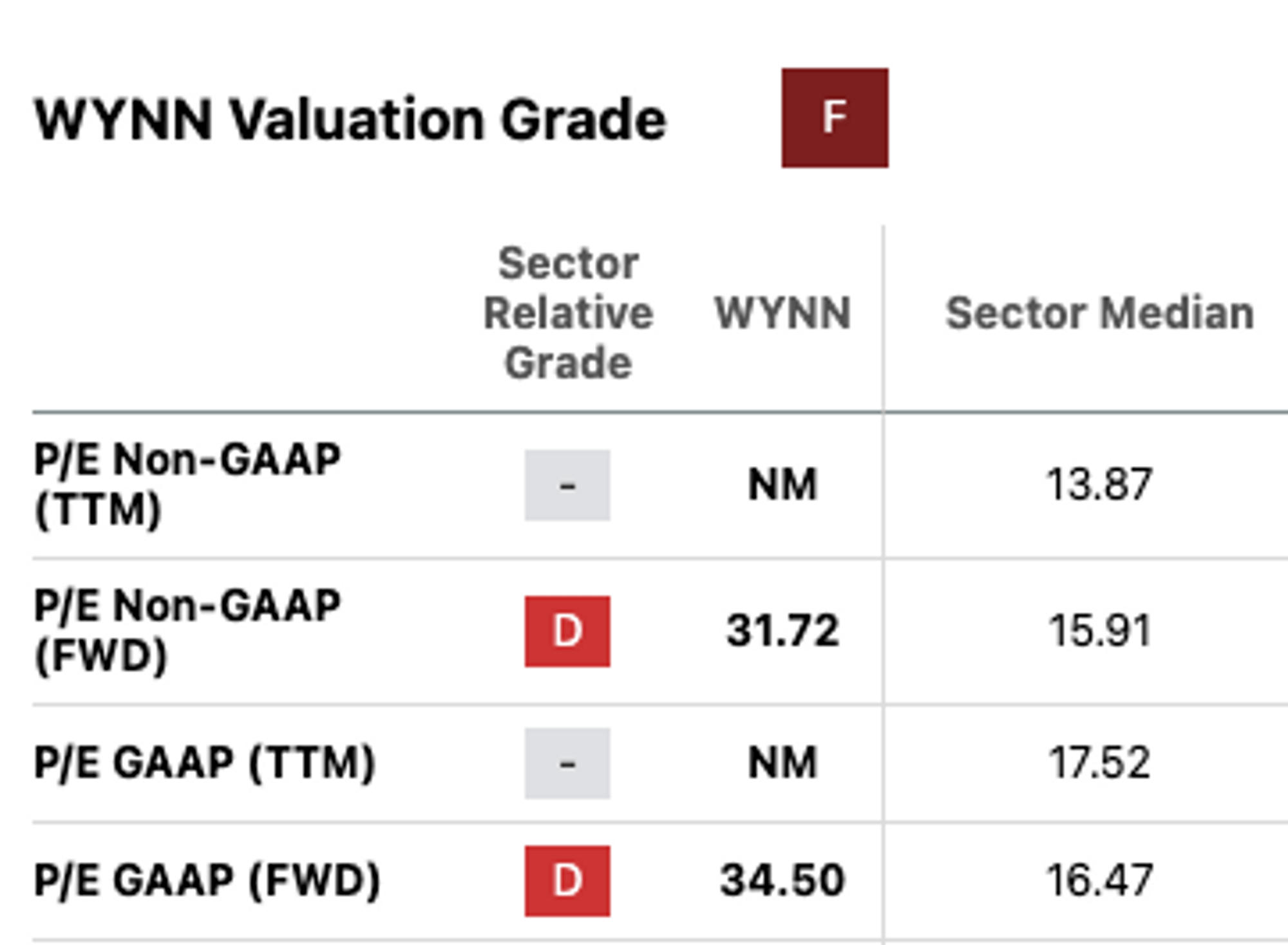

While recent earnings over the past year make any P/E ratio assessment potentially skewed, especially when compared with competitors with less exposure to the Macau market, it's evident that Wynn's current trading position is somewhat elevated. However, a balance sheet analysis paints a different picture. Wynn boasts one of the highest Cash to Debt ratios in the industry and is actively enhancing cash flows, evident from projects like Wynn Al Marjan Island. A substantial cash reserve not only ensures favorable financing terms but also provides opportunities for future acquisitions or benefits for investors. To us, the value of such liquidity is paramount and should be factored heavily into any valuation and investment in the space.

{kind=link}

Conclusion

{kind=link}

Given Wynn Resorts' extensive international footprint, a primary emphasis on delivering unparalleled VIP experiences, and a robust cash reserve, we are confident that the company is well-capitalized to bring its strategic vision to fruition. This unique combination places them in a favorable position to navigate the complexities of the global hospitality and entertainment market.

However, while we are inherently bullish about the company's business model and operational strengths, we have reservations about its current valuations. Despite their substantial cash reserves, the prospects for dividend growth appear uncertain. For us, a commitment to shareholder value is paramount. While Wynn's current allocation of 33% of its net income towards dividends and share buybacks is commendable, we believe a more aggressive capital return strategy would make the stock more appealing.

Trading at a forward P/E of 22x for 2024, the valuation seems somewhat stretched for us. It's imperative to strike a balance between recognizing the company's strengths and ensuring an attractive entry point from an investment perspective. At the current price point, while Wynn's business model is intriguing and holds potential, we find it challenging to justify this purchase. We believe that the stock is fairly valued at these levels. If we witness an uptick in dividends and more aggressive share buybacks, our interest might be reignited. Until then, while we admire the company's operational prowess, we will be observing from the sidelines, awaiting a more compelling entry price.

For further details see:

Wynn Resorts: Strategic Withdraw From Digital Gaming