WYNN - Wynn Resorts: Turnarounds Are Hard. Most Companies Don't Make It

Summary

- Wynn has a crushing debt load that they need to reduce.

- Competitors have more growth opportunities and use their capital more effectively.

- At the moment, there are more arguments against an investment than for one.

Thesis

I think that Wynn Resorts (WYNN) is in a very difficult position right now. They will have more revenue coming back in 2023 as a result of the opening of China, but in my opinion that is not enough because the company has several problems. Even before COVID, they had margin problems, poor returns on capital and not enough free cash flow. So you are more or less betting on a successful turnaround. In the following paragraphs, I'm going to explain why I don't think Wynn is a good place to invest at the moment.

Short Introduction

In Macau, Wynn operates and owns 72% of the two resorts, Wynn Palace and Wynn Macau. In Las Vegas, they are the operators and owners of 100% of Wynn Las Vegas and Encore at Wynn Las Vegas. They also opened Encore in Boston on June 23, 2019. In addition, they own a 74% interest in Wynn Interactive, which operates the OSB and IGaming businesses.

Analysis

Wynn Resorts today released corporate results for the quarter ending Dec. 31, 2023. Let's take a look at those.

{kind=link}

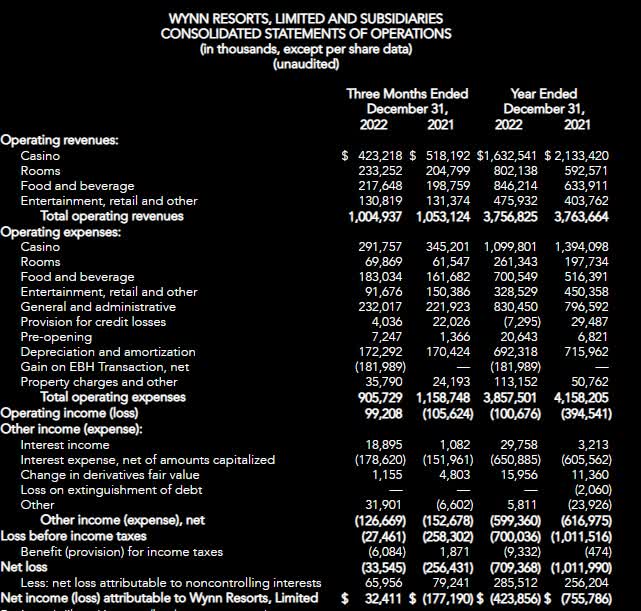

Here, as with the competition, you can see that rooms, food and beverage revenues have increased. This is due to the fact that the prices for hotel rooms can be adjusted at any time. Food and beverage prices can also be adjusted quickly. Casino revenues, on the other hand, fell sharply in 2022. However, this is due to the two Macau casinos as you can see from the two graphs below. The net income loss has also become smaller and the probability that a profit will be achieved in 2023 is high.

{kind=link}

{kind=link}

In my opinion, the opening up of China will be a boost to revenues in Macau, but also in the US, because the Chinese are good gambling customers.

Margins

{kind=link}

Here you can see that the operating margins have already decreased before COVID. Until the end of 2014, they were still in the 20% range and then they fell sharply. The question now is, can they reach margins of 20%+ again in the next few years or will they continue to be in the low range? Competitors like Red Rock Resorts (RRR), for example, have achieved operating margins of 30%+ here in recent years.

Return On Capital + Return On Equity

{kind=link}

If you look at the figures for return on capital and return on equity for the last 11 years, you will immediately notice that some of them are negative. While the competition here has achieved values of 20%+, Wynn has not been effective with capital. A very important characteristic is that there are good investment opportunities and these are exploited with a high return on capital. In January 2022, plans were announced to open a resort in the United Arab Emirates in 2026 . This shows that there are growth opportunities, but better returns on capital would be very desirable. For me, one of the most important metrics for an investment is an annual ROC of 20%+ over 5 years. Wynn Resorts is nowhere near that at the moment.

Shares Outstanding

{kind=link}

Unlike Churchill Downs (CHDN), which is aggressively buying back its own shares, Wynn's shares outstanding have increased in recent years. An effective way of returning money to shareholders is to buy back their own shares, which is also done by many competitors in the gaming industry. Wynn, on the other hand, issued 7,475,000 new shares on February 11, 2021 to repay an equity offering from the proceeds. The debt situation and COVID have just been a drag on the company. But in a first step, they bought back almost 3 million shares by December 31, 2022, to counteract the dilution.

Debt

{kind=link}

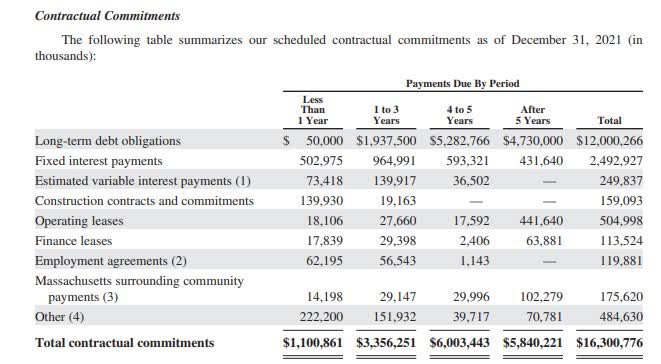

Here's a recap of the contractual commitments from last year's 10-K. In addition, a sale-leaseback arrangement was concluded for Encore Boston, which generated approximately $1.7 billion in cash. Current cash and cash equivalents of $3.65 billion are offset by current and long-term debt of $12.12 billion. Nevertheless, you can see that the debt situation at Wynn is worrying. Whether the opening of China can help to reduce these debts quickly cannot yet be answered. A popular argument in this regard is that the value of the real estate is higher than the current market capitalisation. This provides a nice hedge, but selling these assets would obviously be a big loss for the company.

The following chart also shows the sobering free cash flow per share figures. The gaming industry is usually known for its free cash flow generating companies. Wynn's free cash flow has been negative at times, even before COVID.

{kind=link}

Risks

At the moment they are completely dependent on their Macau, Las Vegas and Boston operations. As you can see from the situation in China, this is a greater risk than for companies that are more diversified. In addition, there is no guarantee that future cash flows will be sufficient to meet obligations. And the current interest rate situation may make further financing difficult. Furthermore, competitors have so far dominated the OSB and IGaming markets.

Conclusion

Wynn has had a difficult time because of its closed resorts in Macau and its mounting debt. They have also not been as good at capital allocation as their rivals in the past. But they do have their new 10-year gaming concession agreement in Macau, which could be very profitable in the future. However, my view is that there are more attractive opportunities in the gaming sector at the moment. Margins, ROC and free cash flow all underperform peers. And those are important things that drive the share price. Given the debt situation and the very low ROC figures in the past, which showed that Wynn Resorts was not a good capital allocator, I do not recommend investing at the moment but if they can reduce debt and increase ROC going forward, they would be interesting because of their Macau operations.

For further details see:

Wynn Resorts: Turnarounds Are Hard. Most Companies Don't Make It