XRX - Xerox Holdings Corporation: The Juggernaut Of Yesteryear Is Disappearing

2023-04-11 09:49:54 ET

Summary

- Year-on-year flat revenues and margin contractions look worrisome.

- The management has some initiatives in store to increase margins, however, these may take years.

- The financials of the company are underwhelming.

- A simple DCF analysis with a slight expansion in margins still suggests the company is not a good buy.

- The only reason for a hold and not a sell recommendation for current investors is the hope that Carl Icahn is successful in unlocking shareholder value.

Investment Thesis

With the recent annual report delivering margin expansions and revenue growth in the 4 th quarter, I wanted to take a closer look at Xerox Holdings Corporation ( XRX ) in more detail, as I am very curious to see what could be in store for this once huge player in the business of printers and copiers going back 40+ years. Upon further research into the company's financials over the last decade, I see, just as I predicted, that the company's revenues have been going down every single year, as working conditions shift away from the full-time office environment to a more relaxed, hybrid working, paperless era. If the company is not going to shift its business strategy to adapt to this new environment, I believe the company is not going to last long and will continue to lose its competitiveness to sharper, more ambitious competition that does not lack vision.

My recommendation, for now, is a hold, until the company proves that it can navigate the shift to higher margin revenue generators, which includes digitization, cloud solutions, and products that may not involve the paper products of yesteryear, as well as Carl Icahn’s ability to unlock shareholder value.

Briefly on the Latest Annual Report

The 4 th quarter saw a decent performance. Non-GAAP EPS was $0.89, revenue grew 9% y-o-y, adjusted margins were up 440bps and the company is still generating quite a big amount of free cash flow. In terms of the full year's results, it does not look very good. Revenue was flat, according to my financial model, gross margins have contracted 153bps, EBITDA Margins contracted by 241bps, and EBIT by 156bps while net margins slightly improved from -6.5% to -4.5% due to fewer impairment charges this year than last year.

I was not surprised to see that a company that used to be a dominant player in the photocopier game has lost its edge in recent years, with the population becoming more environmentally friendly which enabled a quick adaptation to a paperless environment.

The Way of the Dodo?

Am I being too dramatic? The last time I worked in an office environment was in the summer of 2020, right when everyone was put into lockdown, and we were going to be coming back a couple of months later. I haven't seen the office since then, as I decided to quit just a few months after the pandemic hit. Even before the lockdown, we swiftly switched to a paperless environment. We didn't have to walk to an old printer to print a copy for a manager to sign and then just put all the pages into a drawer not to be touched again. It was necessary for audit purposes only. PDFs became the new norm which saved time and freed up drawer space for my porridge and peanut butter.

Do we have on our hands another Blockbuster or Kodak in the works? The company has lost profitability and efficiency over the years and if it continues that way, it may end up being just like the aforementioned big players in their respective spaces in their heyday.

So, what is the management doing to shift its business to the future that will most likely involve less need for paper than ever before? There are a few things that I found to be quite promising, but in my opinion, will take quite a long time to become meaningful in terms of generating serious revenue for the company.

One interesting innovation I saw is the new CareAR, which sounds like something geared toward the future, however, it is a technician on call if available, who will diagnose the problem of the Xerox machine via mobile phone, and provide visual guidance by drawing on the phone for clear instructions. You can also discuss what the problem is and get educated, all while the technician can see the problem live. This sure does sound like it is future-proof, however, if we see less demand for Xerox’s machines in the next 10-20 years, I don’t see how CareAR can survive without shifting its business also.

The way forward is digitization. Many companies like Xerox that were founded many decades ago embraced digitization and improved their profitability efficiency significantly. One interesting example I found is Quiet Logistics’ (owned by American Eagle Outfitters (AEO)) shift to implement robots to pick out the products in the warehouse and bring them up to the front where the products can then be packaged. This meant that human workers didn’t need to walk 12-16 miles a day to get the products from the back, which increased productivity by 80% over time.

XRX has been dabbling in 3D printing space for a bit now, even though, I thought the 3D printing fad collapsed around 2013 or 2014, many people are saying that by 2030, we will likely see many applications of 3D printing in different industries like healthcare, automotive and aerospace industries.

To me this sounds like a natural progression from a 1960s paper printer company to the futuristic 3D printer company of tomorrow, however, it seems like the management isn’t very excited about this opportunity as in the latest 10-K report , the company has paused growth investments at Elem, their 3D printing business. Bummer.

If that is not exciting for them, then another digital solution that the company provides is Xerox Services, specifically for accounts payable. This service, with the help of AI, helps extract material from printed and scanned documents into business workflows, and archives and integrate it into the cloud. This could be an interesting revenue generator if the company manages to scale it.

The termination of the Fuji-Xerox joint venture means that the company has lost quite a big portion of the Asian market. The company said it would sell under its name but that was quite a big blow to the company.

While there are ways the company can improve efficiency and shift its plans towards digitization and become less reliant on revenues from its physical products, that shift is very far from being realized. Does that mean it's going to go the way of the dodo? It may survive for a while longer as the demand for its products is still quite healthy. Furthermore, the company is already starting to adapt its offerings that accommodate home office users. Right now, I think that the company is going quite slow in the evolution of the business and it is going to be a long process.

Financials

Let’s look at the company’s books to see how well the company is equipped for the future. The company has quite a good amount of cash on its hands, although that is down around 43% from the year prior. The company also has more debt than the market cap. It has been consistently reducing it over the last 5 years, however, with how the company is operating, it will certainly employ more leverage to keep itself afloat for a while longer in my view.

Operating profit still covers the interest expense on debt; however, interest takes almost half of it. If the company is going to continue this trajectory, it will be quite hard to come up with the cash needed to pay the interest on the debt.

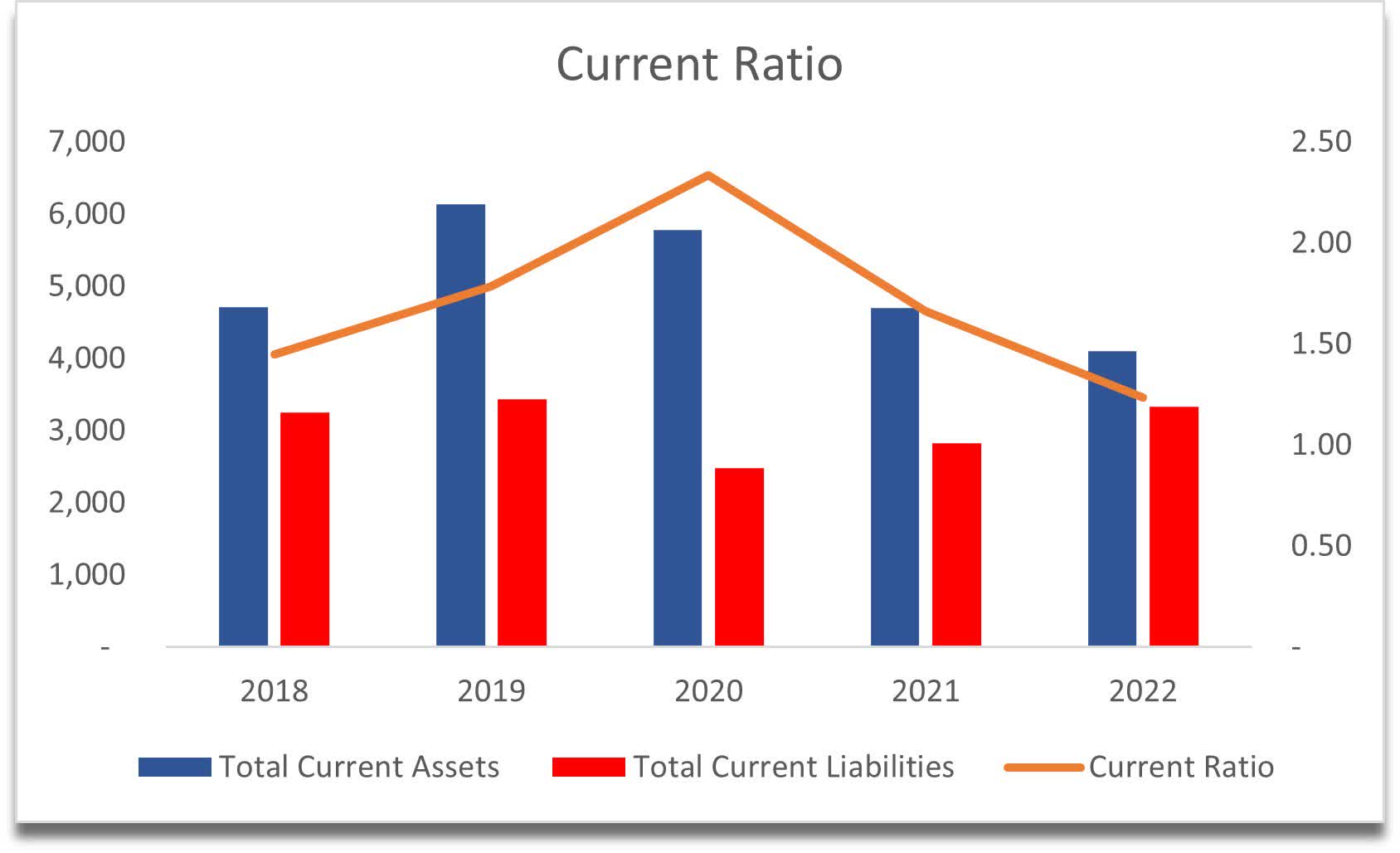

The company’s current ratio has been deteriorating also; however, it is still above 1 for now, which suggests the company does not have problems meeting its short-term obligations.

{kind=link}

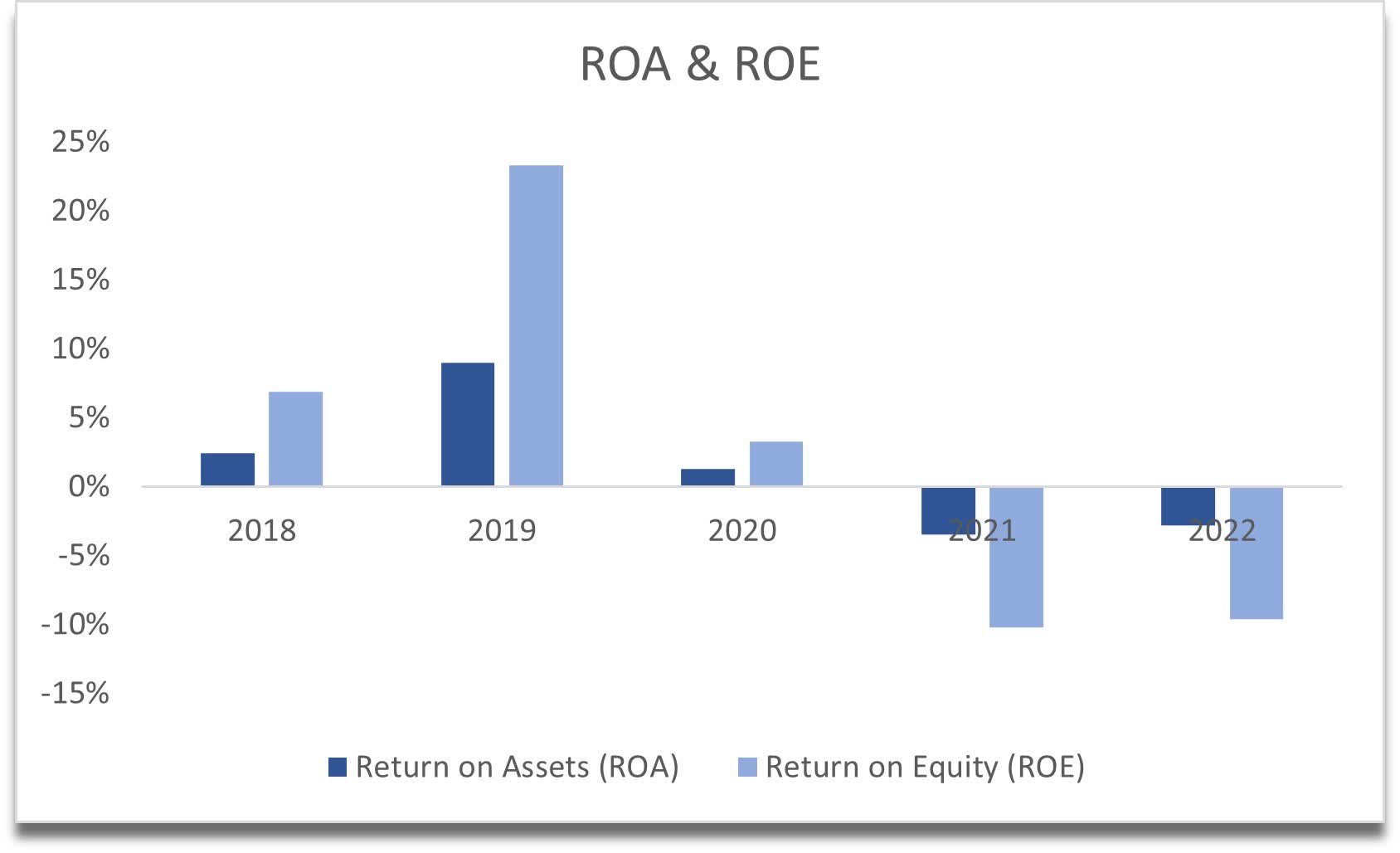

The next metrics show how the company has lost its edge in efficiency and profitability. ROA and ROE have turned negative since the pandemic hit and have not been able to recover yet, due to the fact that the shift towards home offices and a paperless environment stayed.

{kind=link}

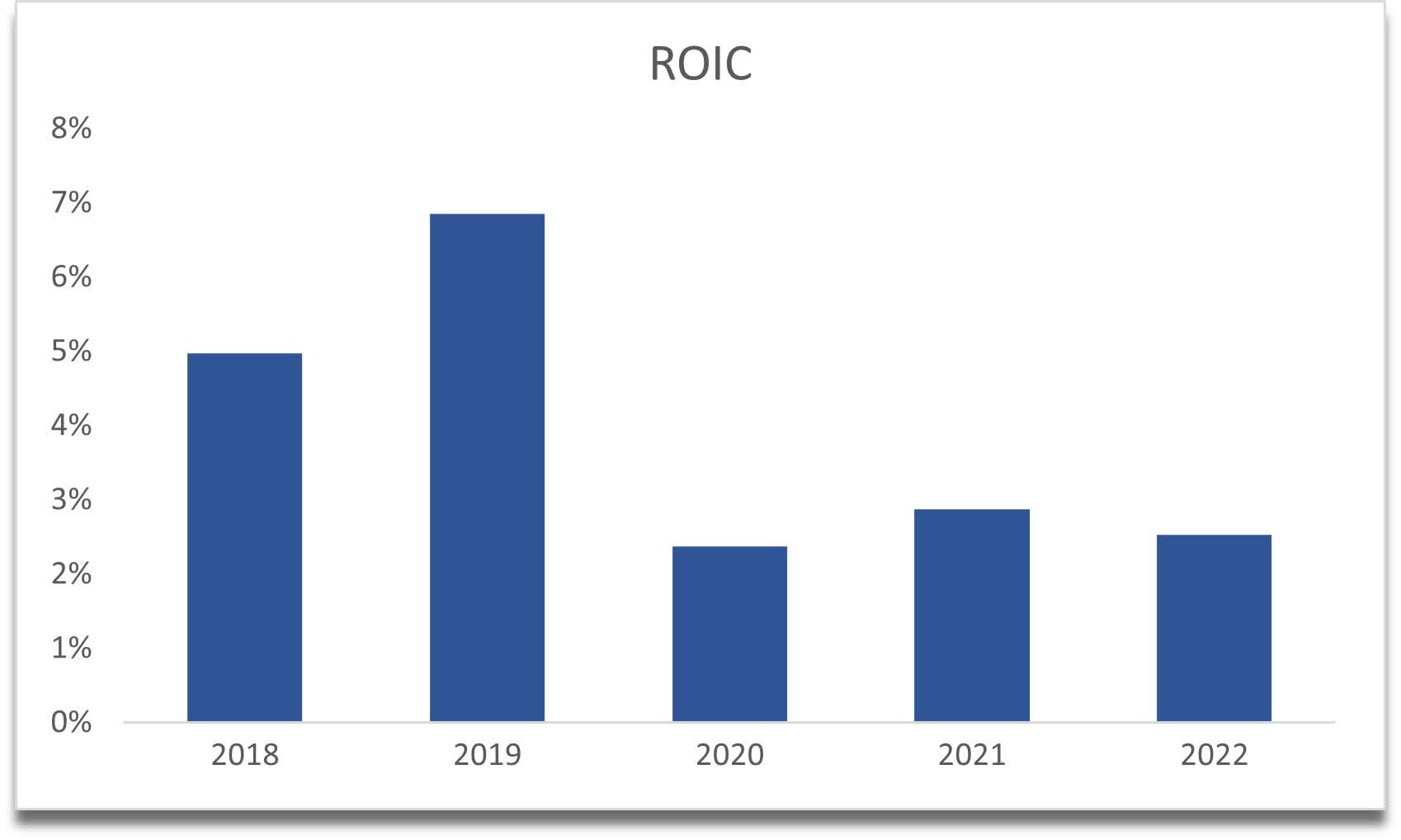

The same goes for ROIC. I believe the company has lost its competitive advantage and the moat it once had has deteriorated, maybe irrecoverably.

{kind=link}

Overall, I see a lot more bad than good here. The company is a bit overleveraged for my liking and it looks like it will continue to employ leverage in the future if the past is any indication. I’ve covered many other stocks that have much healthier balance sheets, so it's not looking good for XRX.

Valuation

Back in 2013, the company was able to generate over $20B in revenue. Fast forward 10 years and XRX is doing 64% less in sales. The company has not seen a single year of increasing revenues in the last decade. There is no reason for me to model revenue increases in the future as I don't believe XRX will be able to achieve any type of relevant catalyst that would make revenues propel much higher. Nonetheless, I went with slight increases in revenue year-over-year just to be more generous (0.5% increase every year).

What can make the company more profitable and reward its shareholders is if it can become more efficient. With the above innovations that the company is trying to achieve, I modeled that the company will be able to increase its gross margins by around 500bps by ’32 and net margins by a whopping 10% (from -5% to +5%) by ’32. I usually like to go conservative in my assumptions, but the company is doing a great job by presenting quite beaten-down numbers already and if I go even more conservative the company would be outright un-investable.

Seeing that I am also not a fan of the company's balance sheet, I decided to have a larger margin of safety added to the intrinsic value calculation. Here I feel like a 35% discount is sufficient.

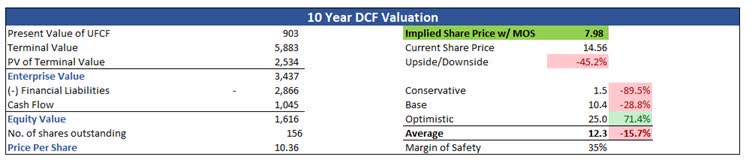

My conservative, base, and optimistic scenarios give quite a large range of possible valuations for the company, but if we take an average then the company is worth around $7.98 a share, implying around 45% downside from current valuations.

{kind=link}

In Conclusion

It is hard to tell if XRX will be around for many years. Next 10 years? Probably. But if we go further out, it does become more worrying that the company will disappear. No one would have thought that the juggernaut of the 60s and 70s would see its fate questioned but here we are. There are better companies out there for sure that I have no problem believing will be around for many decades, for that reason I am not going to invest in XRX any time soon. Some current investors may be hoping that Carl Icahn will do something about the whole company and turn it around by splitting the company, but the man is 87 years old right now, and maybe he is just in it for the nostalgia that he may have had with the product back in the heydays and doesn’t want such an iconic company to go away. That’s just my guess.

The main reason for recommending a hold and not a sell in this situation is that Mr. Icahn may succeed in unlocking the future potential of the company, although it will take quite a while. The opportunity costs of being a new investor of XRX stock are outweighed by better investments out there right now. Even in terms of dividend income, there are better options in my opinion.

For further details see:

Xerox Holdings Corporation: The Juggernaut Of Yesteryear Is Disappearing