XOM - XLE: Be Protected The Next Oil Bull Market Will Be Wild!

2023-04-20 09:45:35 ET

Summary

- In this article, I present my view on the oil market, using multiple timeframes and catalysts.

- We're dealing with a structural shift in supply, a surprisingly supportive policy change from OPEC, and higher odds of a forced Fed pivot down the road.

- I believe owning energy is important. Not just high dividends but inflation protection will likely remain key for risk management for many years to come.

Introduction

Roughly 17% of my dividend (growth) portfolio consists of energy stocks. I started buying aggressively in 2020 for two reasons:

- I needed a source of income to maintain a somewhat decent average dividend yield. This was part of my dividend strategy and my long-term tax strategy.

- I expected a long-term oil bull market, which meant I had to buy some protection, as I expected this to negatively impact other (non-energy) segments.

In 2021 and 2022, we saw what happened when inflation rises to above-average levels, pushed higher by factors that include high energy inflation.

High inflation triggered a rotation from growth to value stocks, as it wasn't attractive anymore to buy companies that would eventually make money at some point in the future. Discounting it wasn't attractive. Since early 2021, S&P 500 value stocks have outperformed S&P 500 growth stocks by almost 20 points. During this period, energy stocks added 127% - excluding dividends.

Together with my defense holdings, energy stocks protected my wealth against high inflation.

In this article, I will explain why I expect a second wave of energy inflation and why it's so important to incorporate energy in pretty much every dividend and non-dividend portfolio.

As an example, I will use the Energy Select Sector SPDR ETF ( XLE ) , which includes a wide variety of energy stocks. Also, because of my Exxon Mobil ( XOM ) and Chevron ( CVX ) investments, I essentially own half of this ETF anyway.

So, let's get to it!

My Energy Bull Case

This may have been the longest introduction to an article I've written this year. However, I believe it's important to highlight the angle I'm trying to play here.

As I have written in multiple articles, I am not rooting for an oil price supercycle - even though it may look like that, given my frequent coverage of my bullish thesis and my energy investments.

Most investors forget that the massive bull run between the Great Financial Crisis and 2021 mainly benefited tech/growth stocks. This was only possible because inflation was at subdued levels most of the time during this period. It allowed major central banks like the Fed, ECB, BoE, and BoJ to maintain accommodative policies.

This created a mix of low inflation, low rates, and loads of cash that were pushed into the hottest areas like tech and similar growth stocks.

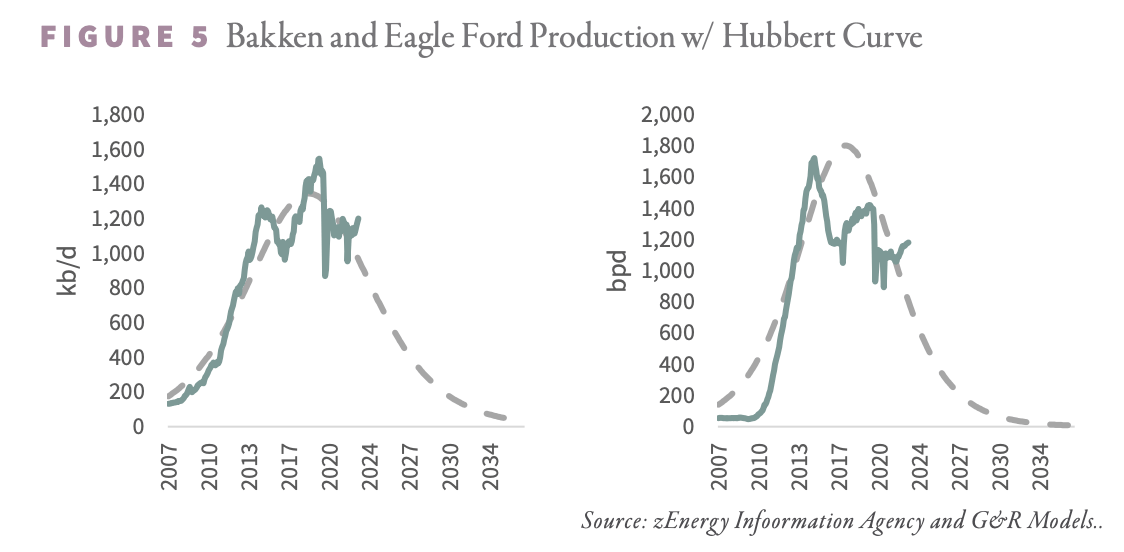

Furthermore, it's important to acknowledge that there are secular reasons that support the long-term oil bull case. As I explain in almost all of my energy-related articles, the period between the Great Financial Crisis and the pandemic benefited from the shale revolution in the United States. It allowed oil companies to use unconventional methods to significantly boost oil and gas production. Especially natural gas prices suffered from it, as supply growth was so high that prices remained subdued at very low levels. It was somewhat self-inflicted harm from drillers but great news for the economy, which requires cheap oil and gas to thrive.

While the chart below isn't updated, it is a great visualization of the shale revolution and its impact on production in the United States.

Our World In Data

As I just briefly mentioned, oil and gas companies harmed themselves by boosting production. It caused supply to rise. In times of slowing demand, oil and gas prices were prone to steep declines. It happened in both 2015 and 2020 when a number of weaker players in the industry went bankrupt.

Now, these companies have learned from their mistakes. The trigger was a shift in policies. Western (progressive) governments are pushing for net zero and an end to fossil fuels. This has caused a total regime shift, which includes limited outside funding (like banks lowering O&G funding), less insurance coverage from major players, and a high likelihood that support will fade even faster once the industry suffers from lower prices again.

On top of that, we're dealing with a decline in inventory quality. As I wrote in a recent article , the shale revolution is dying. While we're not beyond peak oil, we are now seeing slower growth rates as a lot of players are running out of high-quality reserves. Especially in that situation, oil companies are going to be more careful and limit production growth.

{kind=link}

Furthermore, energy companies figured out that there's another benefit that comes with not boosting production as if there's no tomorrow: using free cash flow to fuel shareholder distributions!

While making sure that supply doesn't grow too fast, oil companies are rewarding their shareholders.

According to the latest data, oil producers spend less than 40% of cash on new drilling. The long-term average is at 100%, which wasn't sustainable anyway.

Bloomberg

Looking at the bigger energy companies in the United States, most spent more on dividends and buybacks than on capital expenditures in 2022.

Bloomberg

So far, so good. Now, there are new developments that are important to discuss.

Demand Fears, OPEC, and The Fed

The first part of this article explains why I believe that we're in for a prolonged oil price uptrend. However, this uptrend is expected to come with regular declines caused by demand fears and whatnot.

Hence, it's important to stay on top of things, as new developments have major impacts on the mid-term outlook.

One factor is OPEC.

Earlier this month, OPEC decided to cut its output. That was a surprise, to put it mildly. This is what I wrote on April 3:

Gary Ross, a former oil consultant who now works as a hedge fund manager at Black Gold Investors LLC, noted that OPEC+ is taking proactive measures to increase prices and free them from the grip of macro sentiment.

Starting next month, the cuts made by OPEC+ will result in a reduction of about 1.1 million barrels of crude oil per day. This figure will rise to 1.6 million barrels a day from July due to the extension of Russia's existing supply reduction. It's worth noting that Russia originally decided to lower production in March as a response to western sanctions resulting from its invasion of Ukraine.

Less than two weeks later, OPEC came out saying that it expects oil demand to rise, which is not what one would expect from a group that just vowed to cut its output.

As reported by the Wall Street Journal , the Vienna-based OPEC cartel has maintained its previous prediction that crude oil demand will increase by 2.3 million barrels per day in 2023, despite some of its biggest members announcing plans to cut output by over 1 million barrels per day.

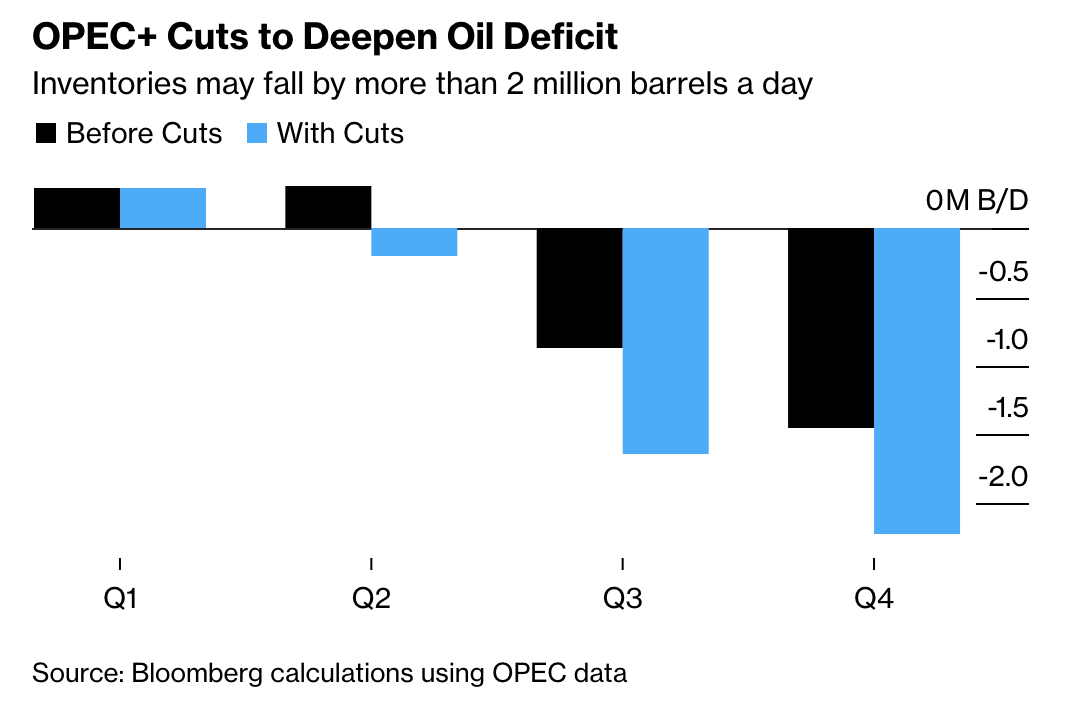

OPEC's own analysts have a different view of the market than those members. The group expects that demand will reach 103.27 million barrels per day in Q4 of 2023, up from 101.55 million barrels per day in Q1, while supplies from non-OPEC producers are expected to remain steady at around 67.6 million barrels per day.

The result can be seen below. It is now expected that oil markets could see a much wider deficit going into the second half of this year.

{kind=link}

Furthermore, we're in a situation where the market is starting to realize that oil demand isn't slowing. Despite environmental policies, higher EV adoption, and renewable energy, global oil demand continues to rise.

Global oil production, however, is seeing very slow growth, which adds to expected longer-term deficits.

With that being said, OPEC is creating a tricky situation. After all, while further tightening in the oil market is long-term bullish, it does put pressure on the economy, which suffers from sticky inflation and slowing demand.

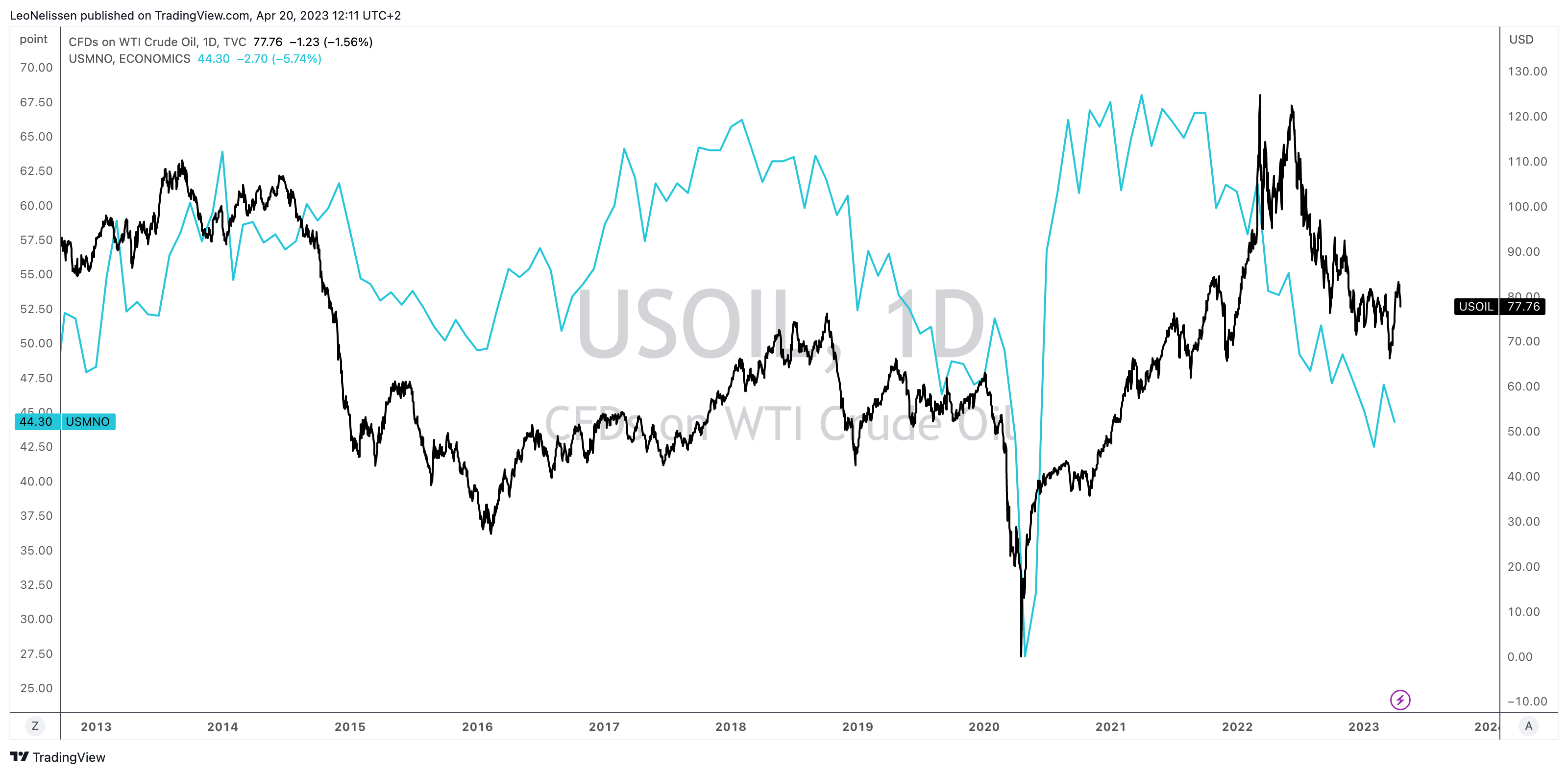

The chart below elaborates on this. It displays the price of WTI oil (the black line) and the ISM Manufacturing New Orders Index. It's no surprise that oil is cyclical. However, oil is still at levels comparable to the prior oil price peak of 2018. I believe that this would not be the case if the supply situation were any different (less tight).

{kind=link}

Based on this context, it's likely that oil prices could remain rangebound for a while. I expect that could be the range between $60 and $90.

OPEC has made clear that it will defend $70. However, I still expect that prices in the $60s are possible if economic growth declines any further.

However, this does not at all change my long-term bull case. If anything, it could provide us with buying opportunities.

It is now highly likely that the Fed will put itself in a spot where it is forced to pivot. While I expect rates to remain elevated going well into the second half of this year, there will likely be a point where economic growth is too weak to justify maintaining high rates. It's likely that a macro event could trigger a more sudden, steeper series of rate cuts, as the Fed tends to break things when hiking.

Bank of America

Historically speaking, this is very inflationary. It would trigger new bets on a looser long-term Fed policy and ease financial conditions. That's inflationary.

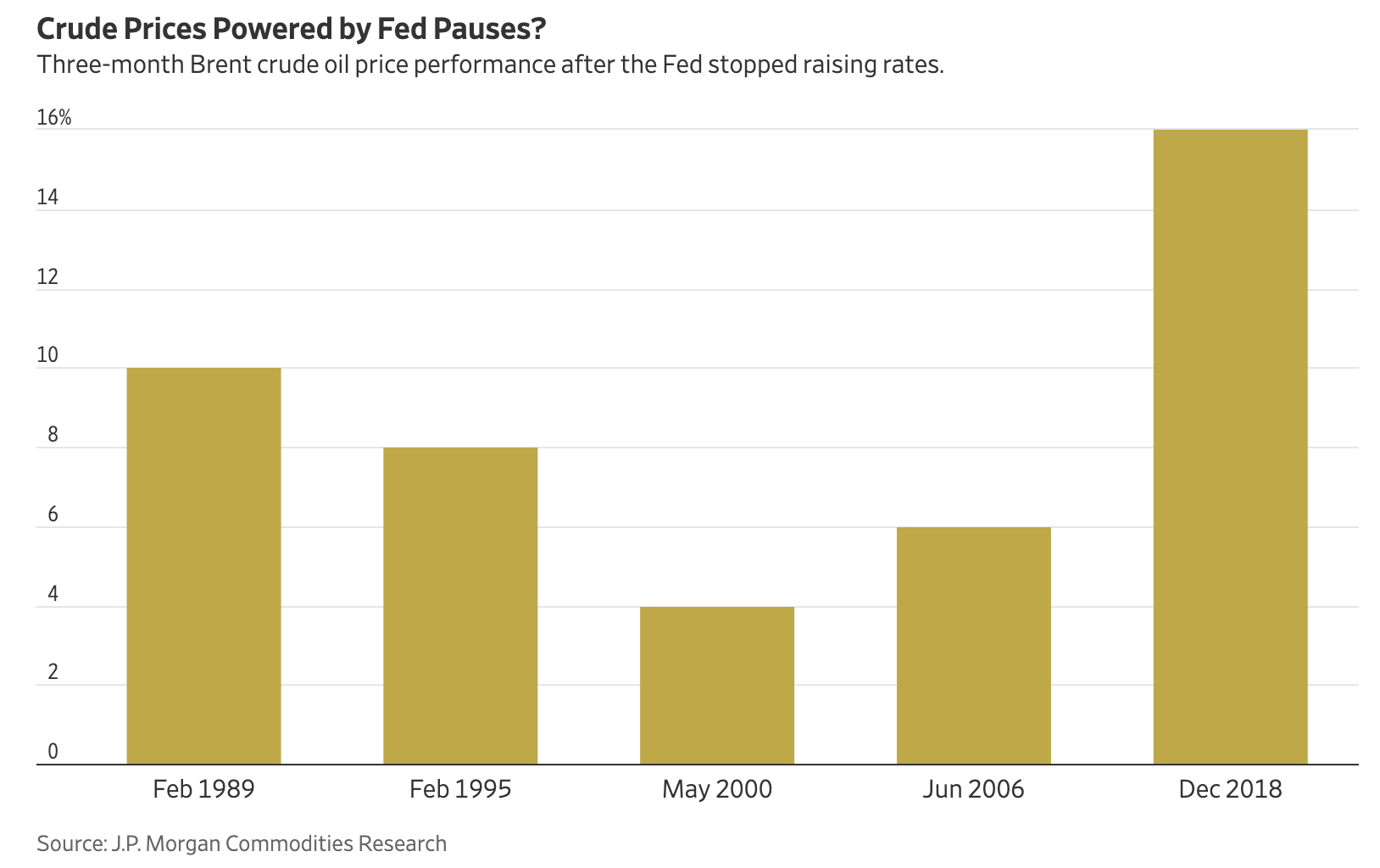

It's also backed by data. Going back to the 1980s, Fed pauses have caused oil prices to appreciate quite significantly.

{kind=link}

A move like this could be amplified by a weakening dollar and a rebound in growth expectations.

It's exactly this scenario that leads me to believe that we could see a second wave of inflation with oil prices remaining in triple-digit price territory for an extended period of time - until the Fed is forced to tighten again.

About XLE

Based on everything said so far, XLE is a proper way to buy inflation protection and income. This passive ETF, with an expense ratio of just 0.10%, mirrors the S&P 500 energy sector. It has roughly $40 billion in assets under management and a history that goes back to 1998.

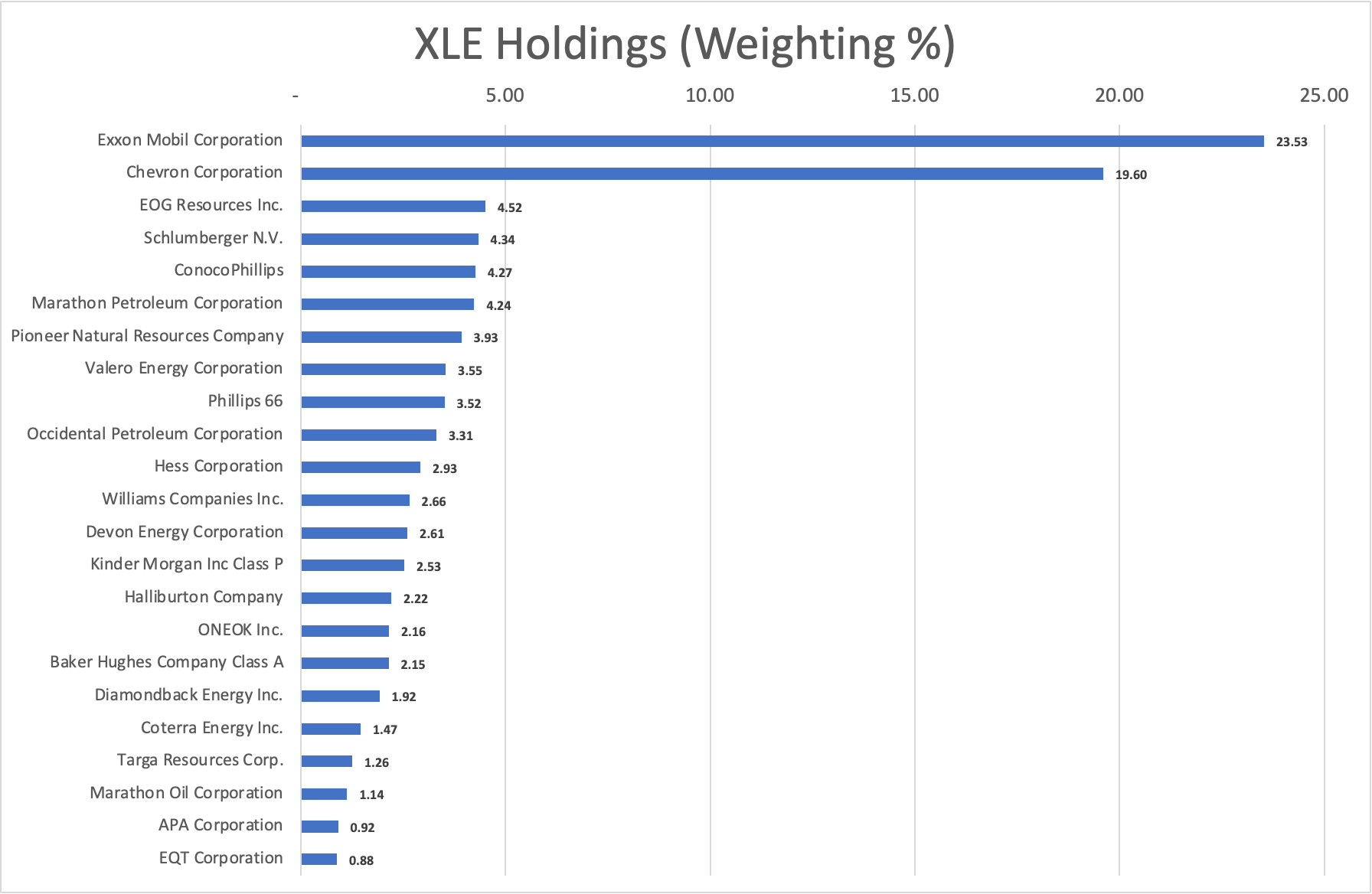

It has just 23 holdings and an average weighted market cap of $206 billion, which is an indication of a heavy top.

As the overview below shows, Exxon Mobil and Chevron have a combined weighting of more than 43%.

Leo Nelissen (State Street Data)

{kind=link}

9% of this ETF consists of energy equipment and service companies. However, the ETF also includes midstream and downstream companies. These are included in its oil, gas & consumable fuels category. The ETF holds all three major refinery stocks, Valero Energy ( VLO ), Marathon Petroleum ( MPC ), and Phillips 66 ( PSX ). It also holds major midstream companies like Williams ( WMB ), Kinder Morgan ( KMI ), and ONEOK ( OKE ).

I own Valero Energy in my dividend portfolio, which means that I have essentially copied 47% of this ETF. This was not my intention. It just happened.

Moreover, thanks to its holdings, the ETF has a dividend yield of 4.0% and an additional tailwind from aggressive buybacks, which I expect to last.

I also expect XLE to outperform the market on a long-term basis, albeit not without regular corrections.

Needless to say, there are many ways to benefit from rising oil prices, which is why I will continue to discuss opportunities for a wide variety of investors.

Takeaway

Investing in the energy sector has become more challenging due to recent structural changes, which I view as a long-term positive for the industry. There is a high probability that oil prices may surge into the triple-digit territory once demand hits its bottom, thanks to the OPEC cuts and their expectations of stronger-than-anticipated long-term demand.

Nevertheless, I anticipate that oil will remain rangebound for the time being due to the impact of the oil cuts on inflation, slowing economic growth, and high interest rates. Therefore, oil prices may find it difficult to reach new highs.

However, if the Federal Reserve were to make a forced pivot, it would be a likely trigger for higher oil prices, which would historically be bullish. If this coincides with increased demand expectations, it could potentially result in a second wave of inflation.

Therefore, I strongly recommend holding energy stocks for both their potential capital gains and dividends, and I believe that having some exposure to the energy sector is critical in the current energy and inflation environment, which was not necessary before the pandemic.

For further details see:

XLE: Be Protected, The Next Oil Bull Market Will Be Wild!