SLB - XLE: Good Value Amid Industry Consolidation

2023-10-31 00:02:11 ET

Summary

- Exxon Mobil and Chevron's massive acquisitions signal a significant shift and consolidation within the energy sector.

- XLE appears investible as its components sport improved financial health, solid profitability, and attractive valuations.

- That said, oil prices remain a serious risk. We're bullish both fundamentally and technically, but a demand shock could dent returns massively.

- We rate XLE a cautious "Buy" on the back of improving industry health and ongoing supply trends.

In case you missed it, it's been a busy month for the energy industry.

On October 11th, Exxon Mobil ( XOM ) announced that it would acquire Pioneer Natural Resources ( PXD ) for $59.5 billion in an all-stock transaction. A few weeks later, on October 23rd, Chevron ( CVX ) announced that it would acquire Hess ( HES ) for $53 billion in another all-stock deal.

While acquisitions are common in the energy industry as companies look to expand vertically and horizontally, two transactions of this size in such quick succession suggest that there's something going on under the hood in the energy landscape worth paying attention to.

Today, we're breaking down these recent transactions and their rationale in order to get a better understanding of how the energy sector is evolving. Then, we'll analyze the largest ETF in the space, (XLE), to see whether or not the fund is a good way of playing the sector's potential future success.

Sound good? Let's dive in.

Recent Deals

As we just mentioned, October saw two goliath transactions in the energy space, as Exxon purchased Pioneer for ~$60 billion, and Chevron purchased Hess for ~$53 billion.

In our view, there are a few reasons why Exxon and Chevron decided to acquire Pioneer and Hess, respectively.

Consolidation & New Resources : The oil and gas industry is constantly consolidating, as companies seek to gain economies of scale and improve their profitability.

This drive is constant in all industries, but acquisitions are typically very accretive in the energy sector given the physical footprint of the companies that operate there.

For example, when a software company buys another one, it's typically so it can acquire customer relationships, a specific technology, or a key individual. The effectiveness of these approaches can be mixed.

However, in the energy sector, land and claims are non-fungible, which means that two companies can't own and operate on the same resources at the same time. This means that bolting on assets to increase footprint is incredibly simple - all you need to do is buy them from the companies that own them (or acquire them outright).

Pioneer has a large presence in the Permian Basin, while Hess has a significant stake in the Stabroek block in Guyana. By acquiring these companies, Exxon Mobil and Chevron are gaining access to new reserves and production potential.

Additionally, equipment and resources are somewhat standardized across the industry, so Exxon and Chevron will be easily able to deploy the acquired industrial assets to their most optimal use within the expanded scope of the combined company.

Improved Industry Health : While acquisition and consolidation makes sense generally within the energy sector, these recent transactions are likely the result of improved industry health across the board.

For one, heightened oil prices since mid 2021 have allowed energy companies, which have historically carried balance sheet issues, to 'right the ship' enough to the point where acquisitions are now feasible again.

Moves like this were off the table in 2020 as companies struggled to survive, but now that things have improved and the industry's financial footing is much improved, they're back on the menu.

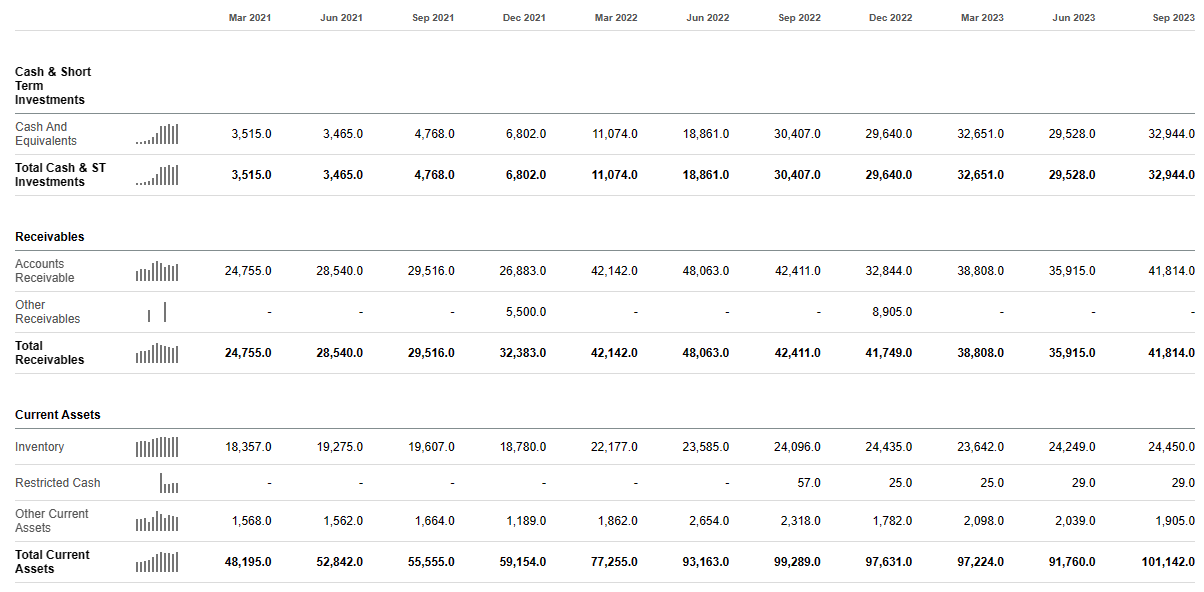

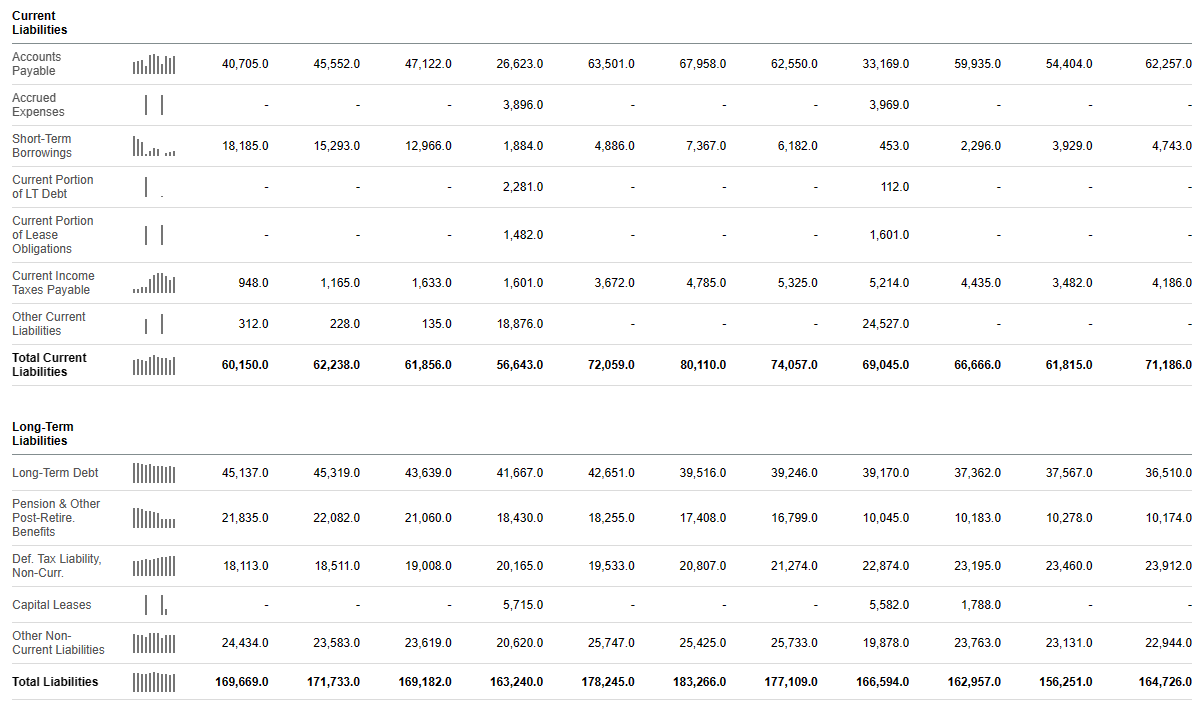

You can see this in Exxon's balance sheet. Cash has skyrocketed, providing much needed flexibility, while liabilities have remained stable, with long term debt actually decreasing over the last few years:

{kind=link}

{kind=link}

In that way, these transactions can be seen as bellwethers of more robust industry health.

Secondly, oil prices are currently at the upper end of their range from the last decade or so due to the war in Ukraine, chronic underinvestment in production capacity, and other factors.

This makes it a good time for oil and gas companies to make acquisitions, as they can expect to generate strong cash flow from expanded operations.

XLE: The Top Energy Fund

So, the recent transactions are evidence of improving profitability and stability in the energy sector. But is the industry investible?

Let's have a look at XLE, the top ETF by AUM that invests in the sector.

The fund's top holdings include Chevron and Exxon in addition to EOG Resources ( EOG ), ConocoPhillips ( COP ), Schlumberger ( SLB ), and Marathon Petroleum ( MPC ):

{kind=link}

Let's dive in and see how these companies have performed over recent years.

XOM & CVX

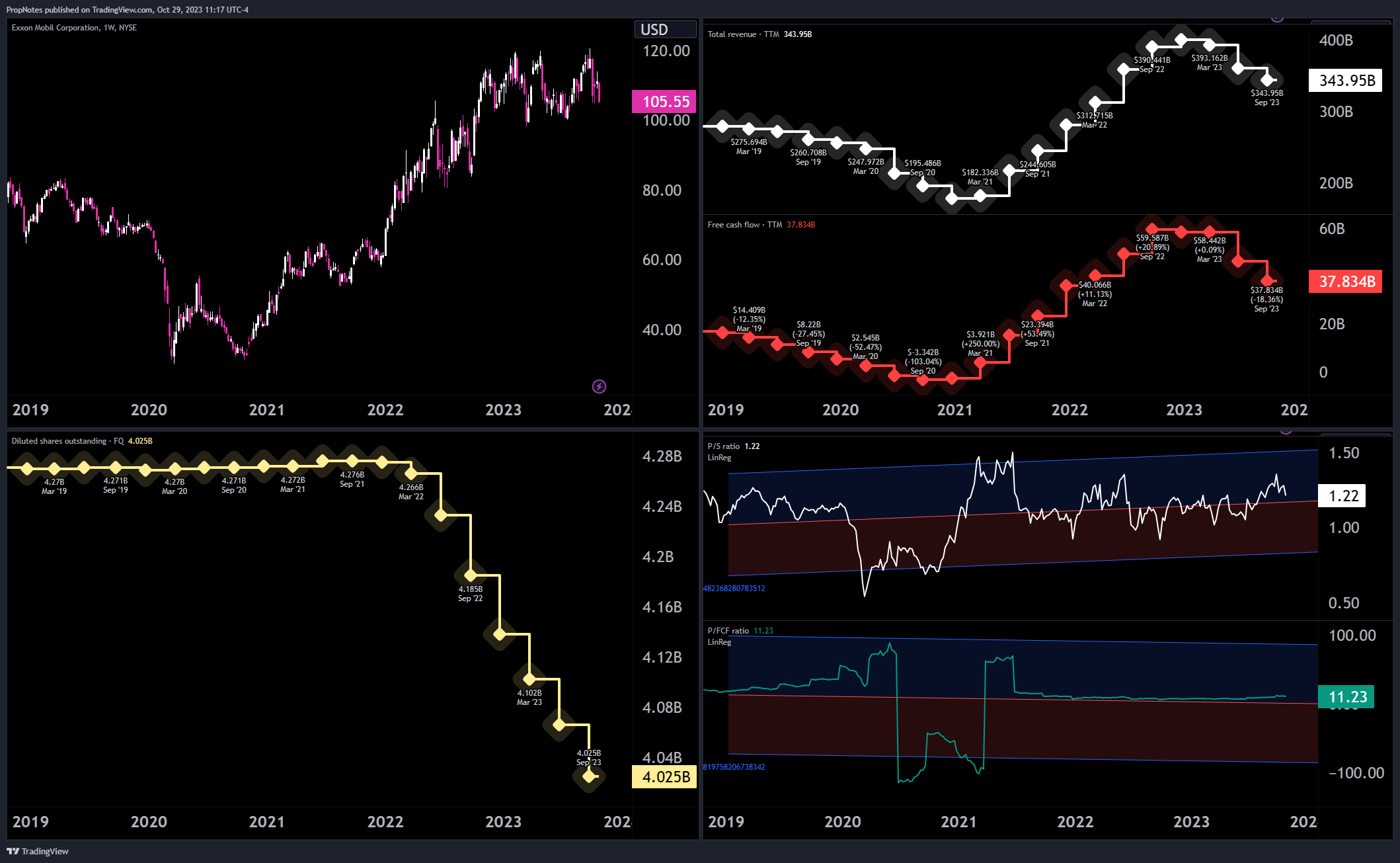

First up is Exxon. The company is an energy behemoth, churning out revenues and profits like clockwork:

{kind=link}

While top and bottom-line multiples are in the middle of their relative ranges, the company is buying back stock aggressively in order to increase EPS. These capital returns are also coupled with increased dividend payouts. This extra cash is a great sign of improved stability - Exxon has the working capital in excess to deploy back to shareholders.

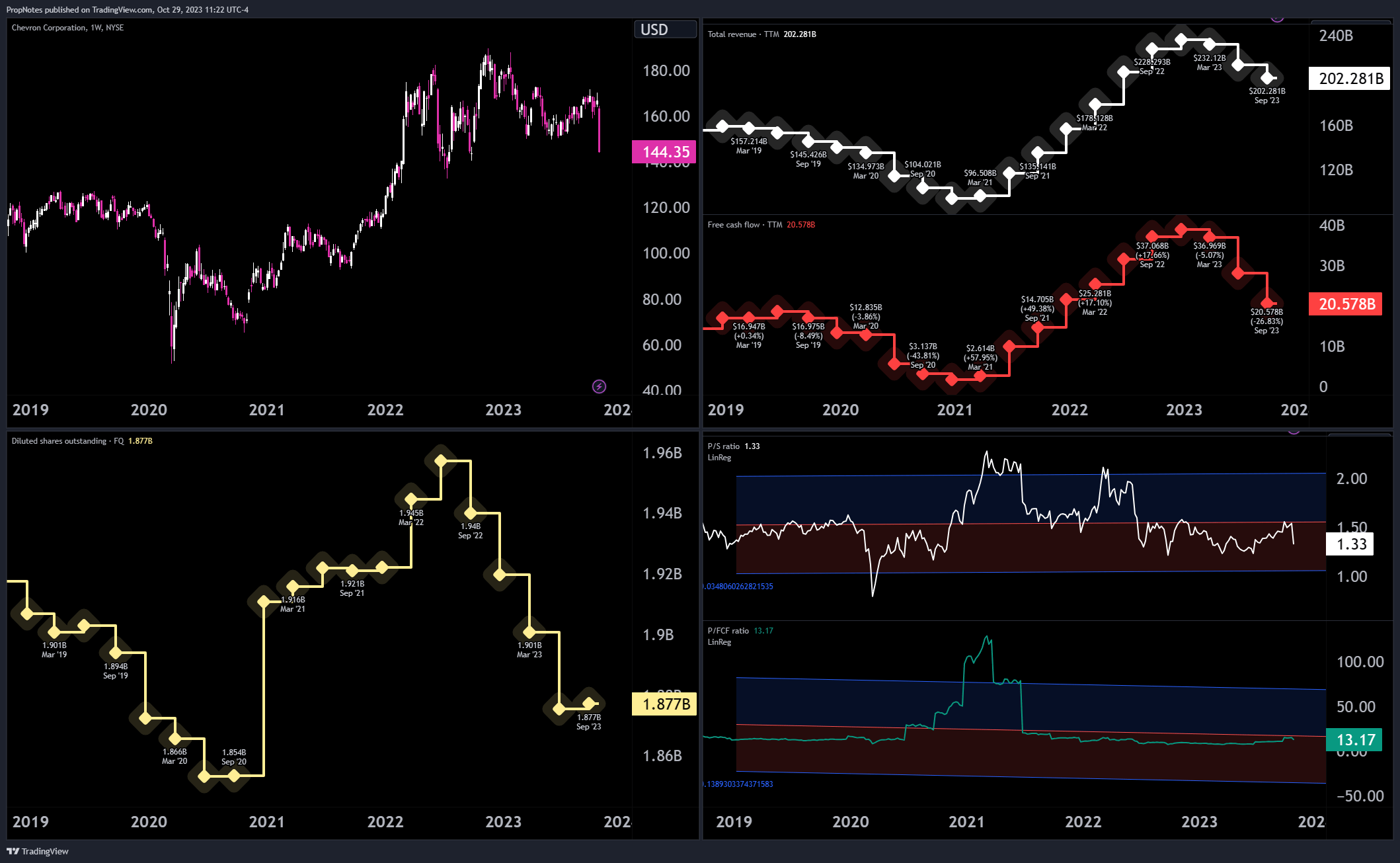

Chevron, often thought of as second fiddle to Exxon, has done well in recent years as well, growing revenue to more than $200 billion, and FCF to > $20 billion:

{kind=link}

Revenue and free cash flow have rebounded with the price of oil, and while the company isn't buying back shares, the stock price, especially when measured on its top line multiple, looks relatively attractive.

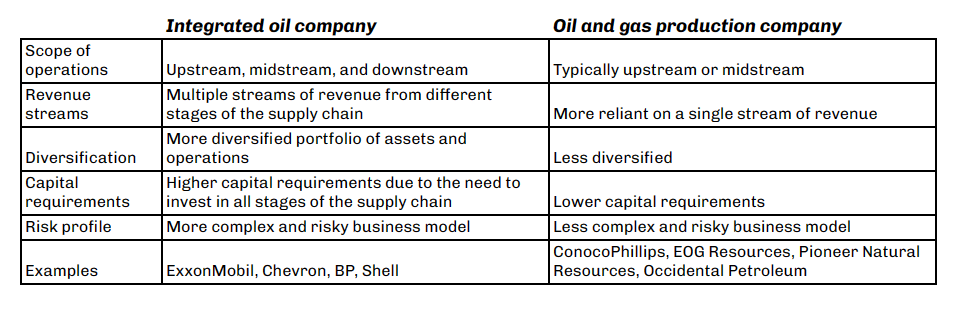

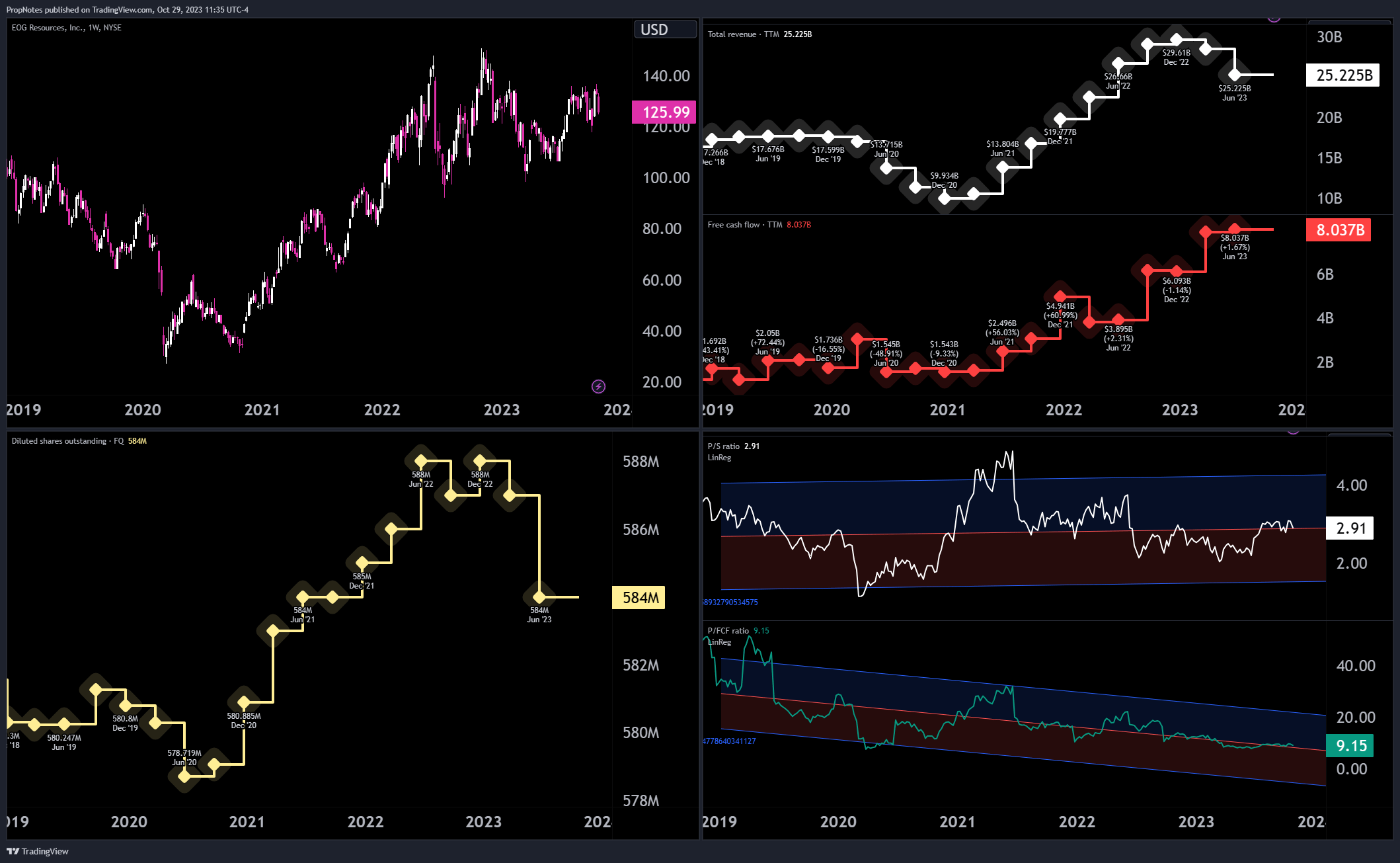

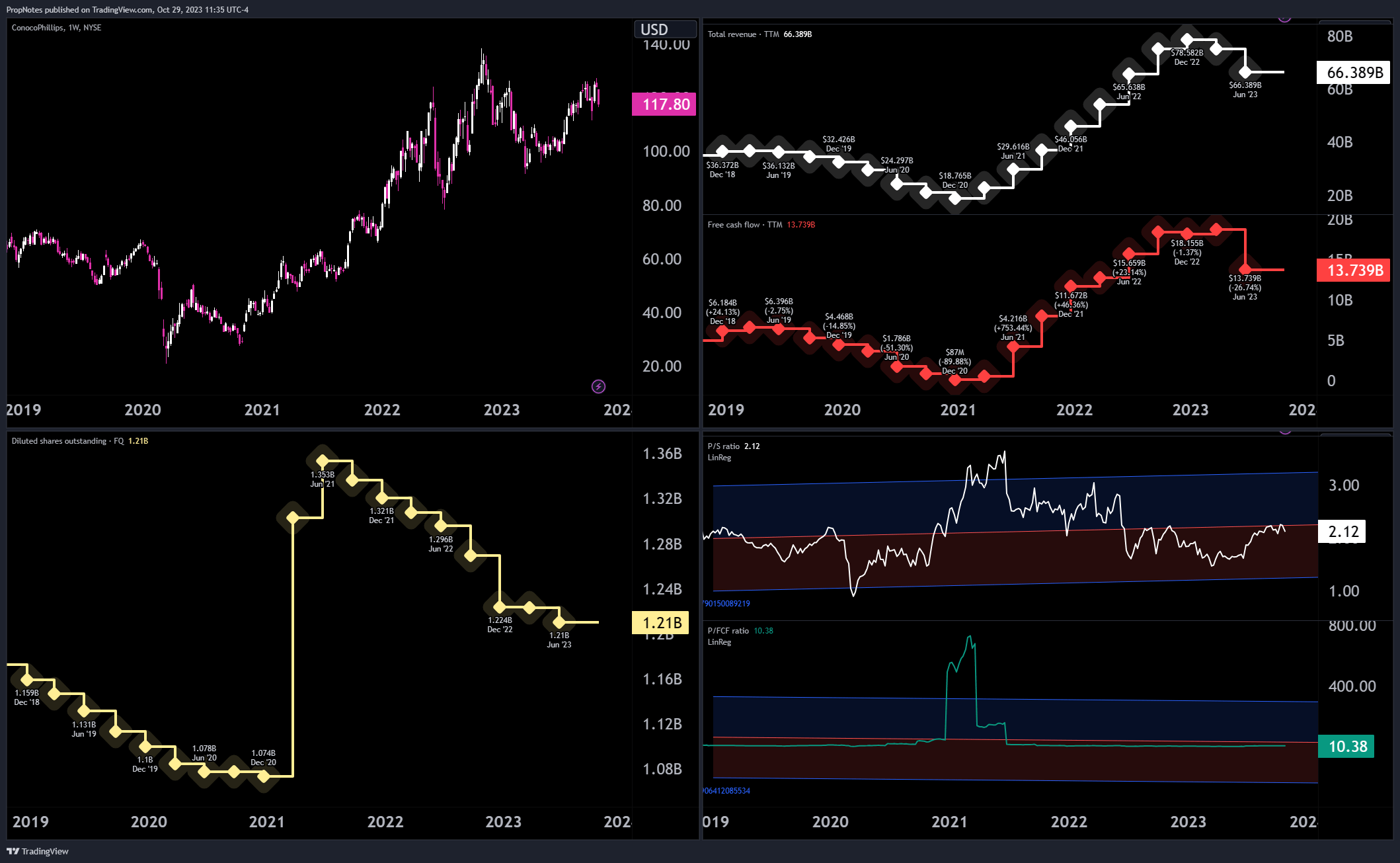

EOG & COP

While Exxon and Chevron are fully integrated oil companies, the next two companies, EOG Resources and ConocoPhillips, would be more accurately described as production companies. You can see the differences here:

{kind=link}

Production is a less diversified business model than being fully integrated, but it does allow for higher operating leverage to oil prices. Thus, when oil does well, EOG and COP do really well.

You can see that in their respective, recent financial results, as cash flows have exploded from pandemic lows:

EOG (TradingView) COP (TradingView)

{kind=link}

{kind=link}

Additionally, prices remain reasonable, around 9-10x free cash flow.

These companies haven't been as disciplined about their share counts, but they're beginning to pour more cash into buying back stock, which is a trend in the right direction.

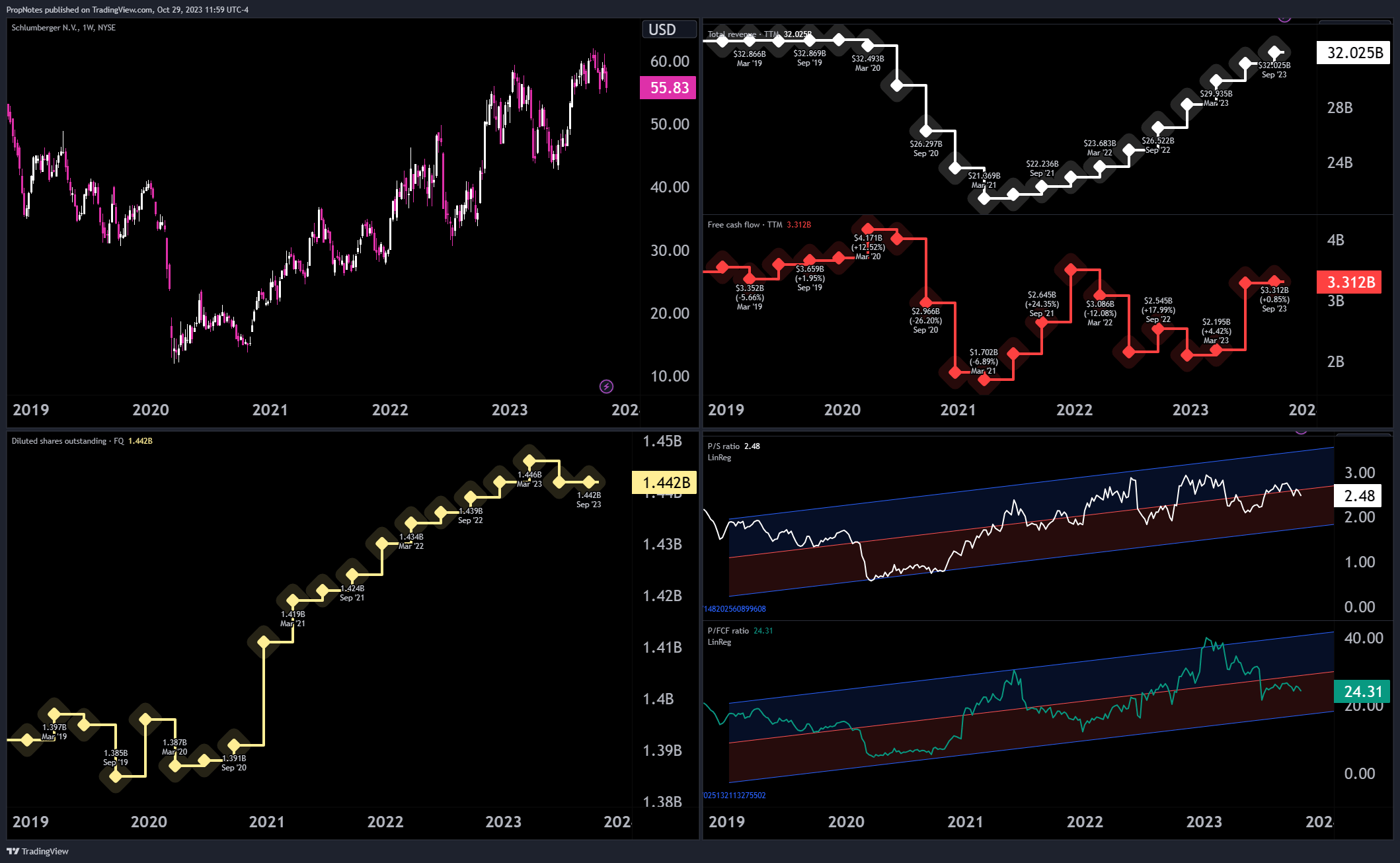

SLB & MPC

Finally, we've got SLB and MPC, which are the largest the largest oilfield services and refining companies in the fund, respectively.

As an oilfield services company, Schlumberger's main job is to assist in the discovery of new reservoirs and the development of new wells. This business has grown to encompass ancillary businesses, like drilling, extraction, and light processing / transportation, in addition to other decarbonization initiatives.

This has been a winning model, earning consistent FCF margins and a premium multiple vs. the industry, even though share count continues to expand:

{kind=link}

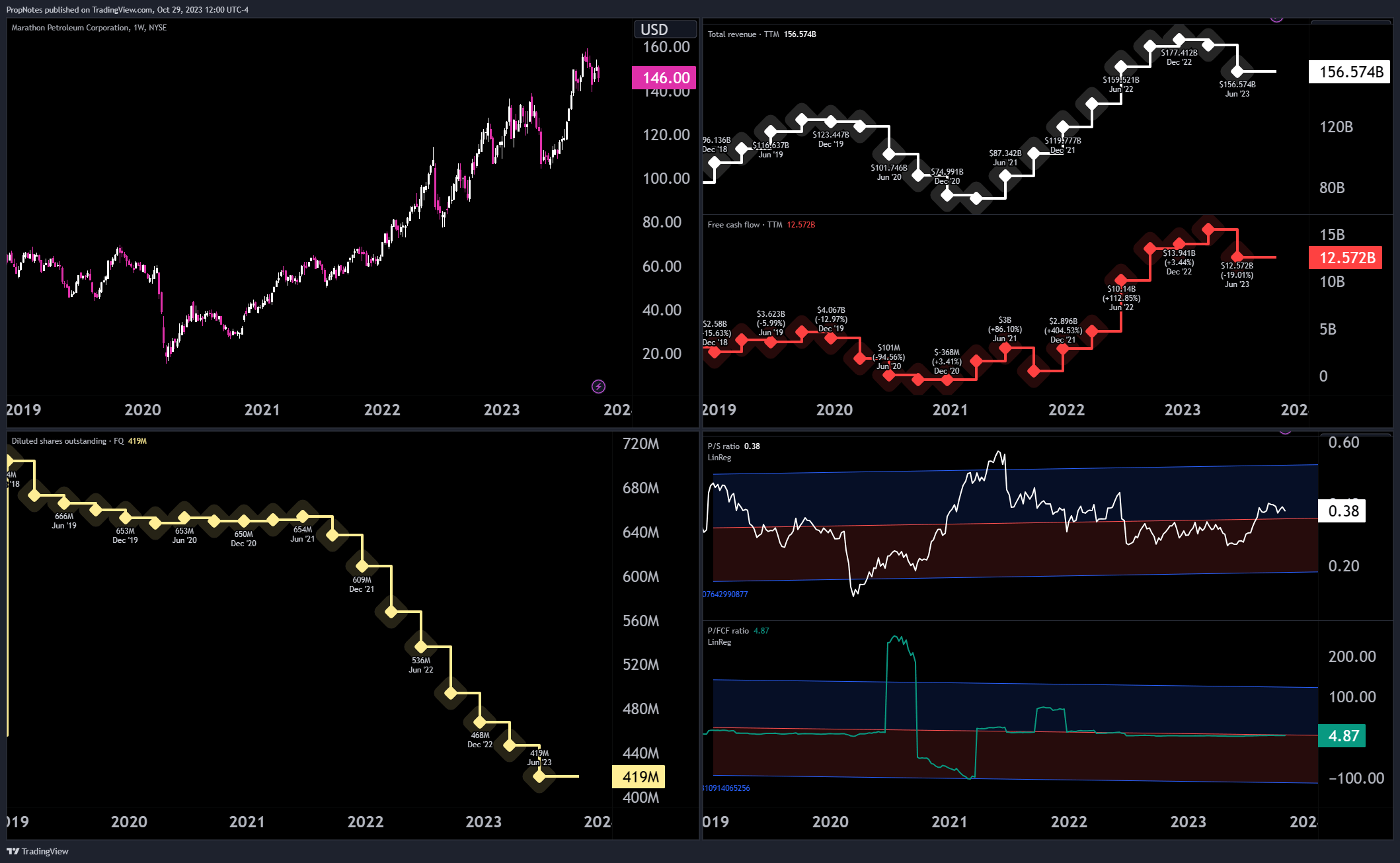

Last but not least, Marathon is the largest refiner in the fund. We've written about the company before , but suffice it to say that the firm is a well-run refining machine, capable of producing solid financial results in all markets while taking advantage of good ones.

The recent refining capacity constraints have led to surging profits, and a corresponding increase in the buyback:

{kind=link}

Taken together, these 6 companies account for nearly ~60% of the total assets in the fund, before taking into account the new XOM and CVX deals which are expected to close in the first half of next year.

Overall, in our view, these companies are high quality businesses that have done well in a good environment - definitely something worthy of considering when it comes to deploying your hard-earned capital.

Where Is Oil Going?

However, despite how much industry health has improved, how well these companies have done, and how attractively their stocks are priced, at the end of the day when you're thinking about investing in energy companies you need to consider that everything, ultimately, is dependent on oil prices.

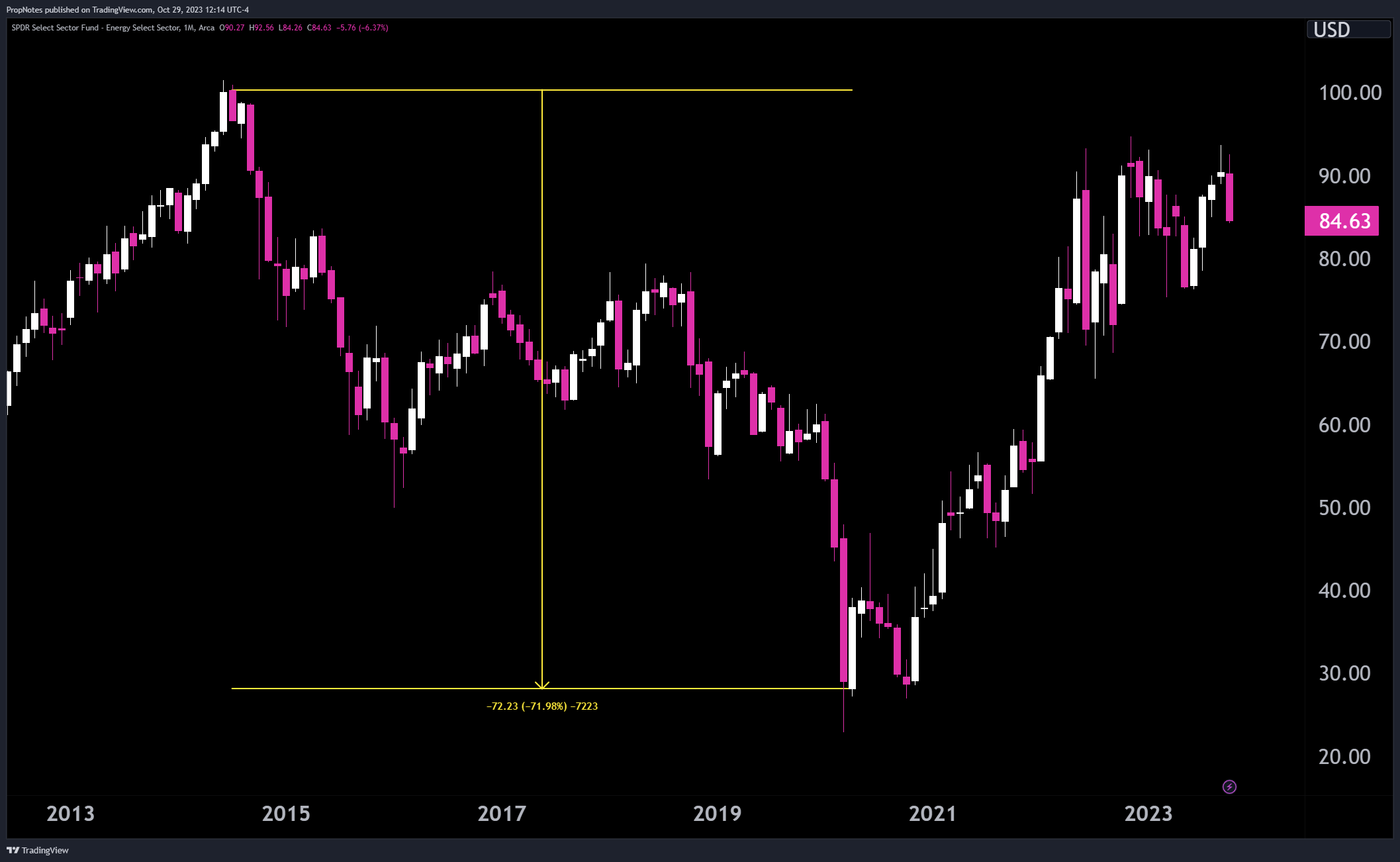

The companies we've mentioned have all done relatively well in previous bear markets as a result of their size and corresponding economies of scale, but investing at the wrong moment in the energy cycle can prove disastrous for long term returns.

In the previous bear market, XLE decreased more than 70% from highs to lows between 2014 and 2019:

{kind=link}

Thus, it's key to have a handle on this market over your investment time horizon.

In our view, oil is set to remain elevated and stable for the next year or so.

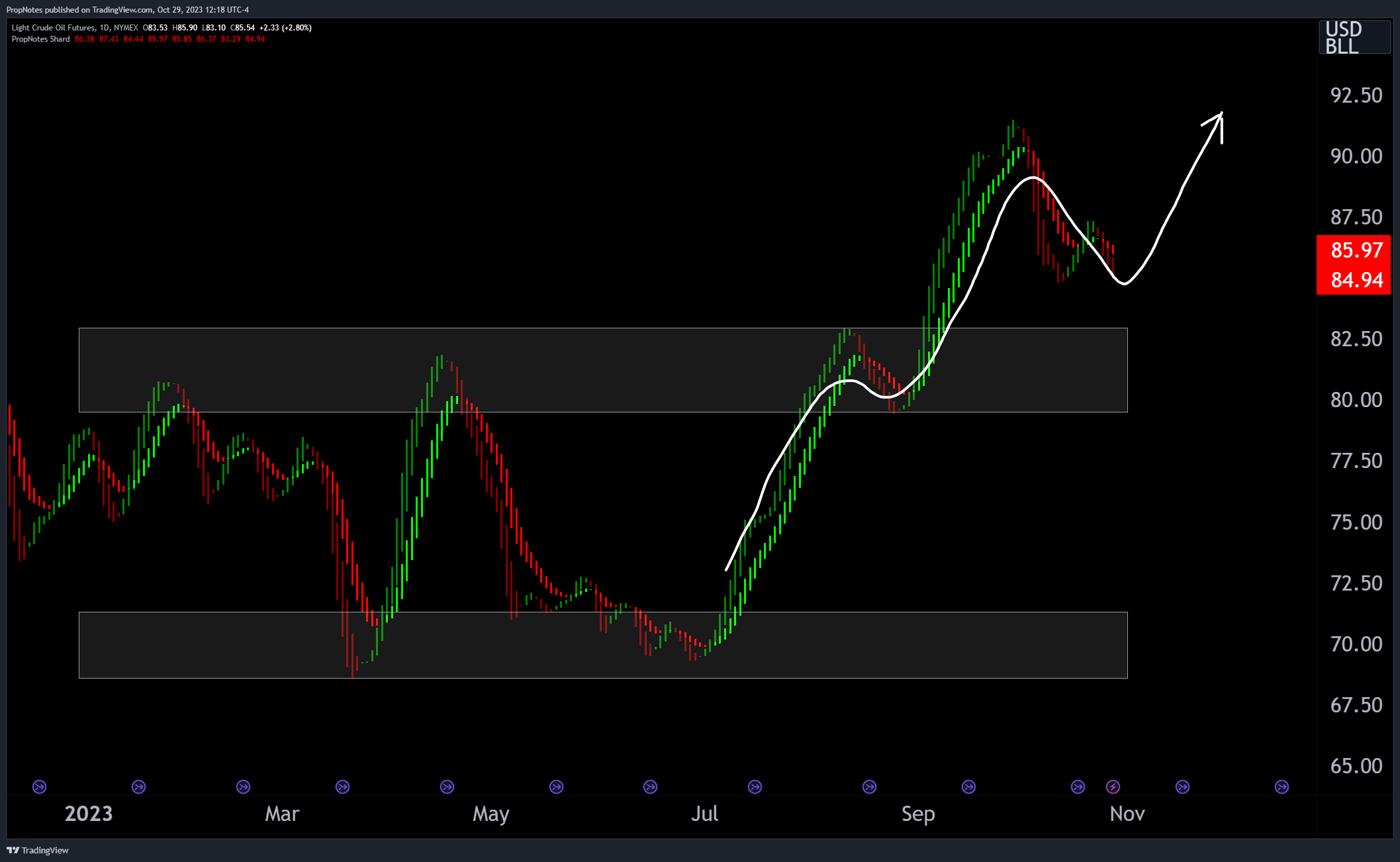

From a technical perspective, oil continues to be strong, breaking above resistance around $80 to new yearly highs:

{kind=link}

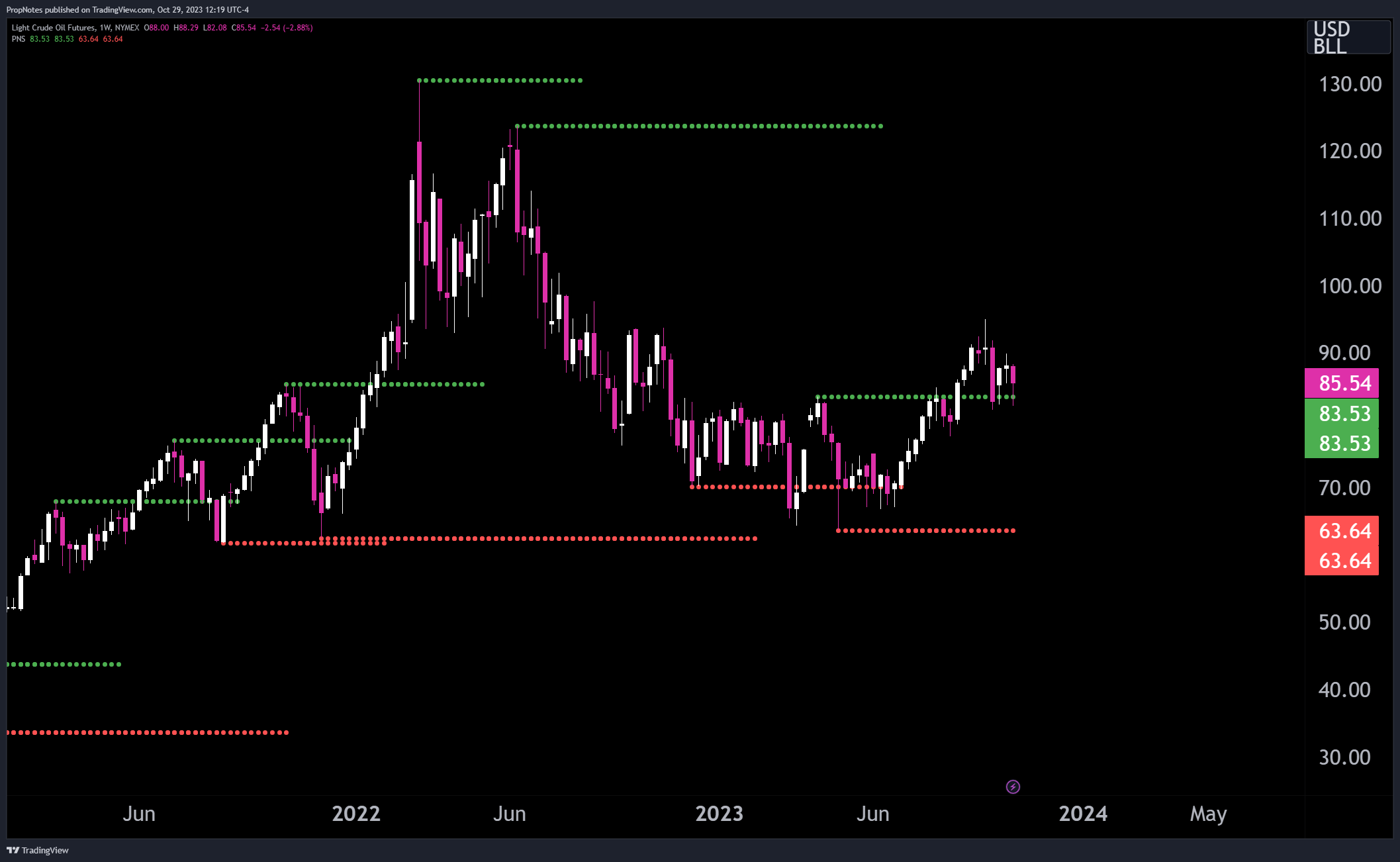

Zooming out, the commodity is trapped in a broader range between $60-$100, but could be headed higher given the recent breakout:

{kind=link}

After making a series of higher highs and higher lows, the commodity has traded sideways for a little over a year, although the recent price action has given us some hope that further increases could be on the way as a result of momentum market participants and bullish hedgers. We're less certain that a big move could occur, but prices remaining historically high seems technically reasonable for some time.

From a more fundamental perspective, the outlook for oil seems to be stable / bullish as well.

Most analysts expect prices to remain elevated in the near term, given the limited supply growth over the last decade. Overall investment in new oil production has declined in recent times, due to a number of factors including the COVID-19 pandemic, the transition to clean energy, and pressure from investors to reduce greenhouse gas emissions. As a result, global oil supply is expected to grow slowly.

This supply/demand imbalance could persist as a green transition slowly chuggs along, leading to favorable price dynamics in the interim.

Backing this up, the U.S. Energy Information Administration forecasts that the Brent crude oil spot price will average $95 per barrel in 2024, up from $84.09 per barrel in 2023.

Risks

Despite our outlook, oil prices also remain the top risk for an investment into XLE. If prices decline, then it's only logical than XLE would experience significant underperformance or losses as the underlying companies discussed experience deteriorated results.

Here are a couple things to look out for.

First, the oil sector is cyclical, meaning that it goes through periods of booms and busts. This is because demand for oil is closely tied to economic growth. When the economy is growing, demand for oil tends to increase, which can lead to higher oil prices and profits for oil companies. The same happens in reverse, which is why the recent forecasts of economic malaise over the next year or so could be of concern.

Secondly, oil companies are exposed to financial risks, such as debt and currency risk. Many of the components discussed above have debt loads, which could drag on earnings if rates stay this high or hike more given refinancing costs. Additionally, as global oil companies, many of XLE's components operate in countries with local currencies, which can affect USD results.

Finally, investors in XLE are also exposed to specific company risk. This is the risk that a particular oil company, like XOM or CVX, may underperform the sector as a whole. Given the size of the XOM and CVX exposure, it's a risk to consider.

Bringing It All Together

All in all, we like the idea of investing into XLE at this point in time. The recent transactions inspire confidence in renewed value recognition in the industry, and many of the top companies are well priced and have been performing well over the last few years.

There's even a convenient ETF, XLE, which provides good diversification with a microscopic expense ratio.

However, oil prices remain a serious, concentrated risk. While we're relatively bullish on them over the interim from both a technical and fundamental standpoint, any declines or demand shocks could cripple the market and send XLE and its components into a tailspin.

That said, right now, it's a risk we're willing to take.

We rate XLE a "Buy".

For further details see:

XLE: Good Value Amid Industry Consolidation