CA - Yangarra Resources: Leaving Past Worries Behind

Summary

- Roughly one-third of the debt balance will be paid off by year-end.

- Production is increasing with a slight decrease to original guidance.

- Cash flow guidance was raised due to higher-than-expected commodity prices.

- The share price to cash flow ratio is approximately 1.5.

- This small company is on its way to becoming large enough to attract institutional attention.

(Note: This is a Canadian company that reports in Canadian Dollars unless otherwise noted.)

Yangarra Resources ( YGRAF ) has one of the lowest market value-to-cash flow ratios of companies that I follow. Currently, a reasonable expectation is annual cash flow in the C$2 per share area while the stock trades at C$3 per share area. So, the ratio is about 1.5 not counting the usual stock price fluctuations that will make that number vary somewhat.

The reason for this low valuation has been the company's debt load, combined with the fact that this small company likely does not attract the attention of institutions that a larger entity would. But management is attacking both items by growing production and by paying down debt. In both cases, management is succeeding admirably. So, one day, the value of the common stock could be a lot higher than the current price.

Yangarra Resources Third Quarter 2022, Financial Results And Revised Guidance (Yangarra Resources Third Quarter 2022, Earnings Press Release)

{kind=link}

Of all the issues that the company faces with the market, the debt levels are the number one concern. Even though this company was a rare company that was profitable in fiscal year 2020, the debt ratio was too high for the market in that fiscal year. There is a demand that the next downturn feature debt ratios that are far more satisfactory.

To that end, the company will likely have repaid about 2/3 of the outstanding debt by the end of the fiscal year. Investors should realize that many companies sell their production about 30 days ahead of time. Therefore, when the company reports, management often has a solid view of a completed month as well as one that can be reasonably forecast. The only "stretching" involves the month of December. All things considered; it would take a major industry announcement to make that December forecast a material miss.

Generally speaking, the market appears to want a debt ratio of 1 or less using considerably lower commodity prices than what is currently available now. This management appears to be well on its way. Management has not only increased production, but the lower debt levels are attacking the previous debt ratio from two ways at one time.

The increasing production likely means that management will be able to find savings just by increasing the amount of production. 10,000 BOED that can be sustained is often a "magic number" for cost savings in the industry. There are more of those numbers as production increases. Costs were already low to begin with. Now those low costs may go lower.

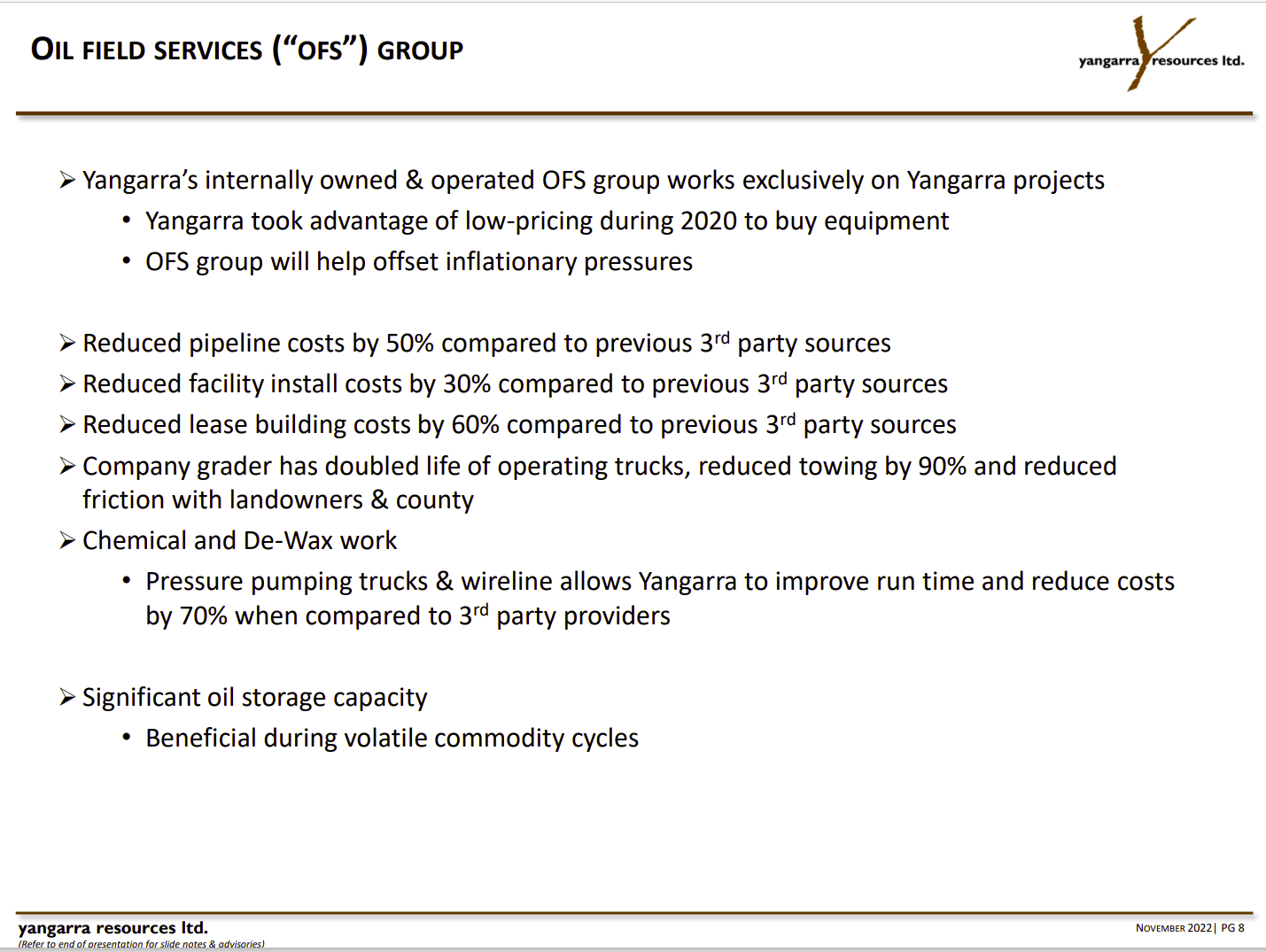

Yangarra Resources Operations Proposals That Reduced Costs (Yangarra Resources November 2022, Corporate Presentation)

{kind=link}

As a company grows , then there are more ways to reduce costs. Now, some of the things like the pipeline costs may have happened even when the company had lower production. But at least some of this is due to production growth to the point where the operations department can do things "in-house" rather than contract it out for the considerable savings shown above.

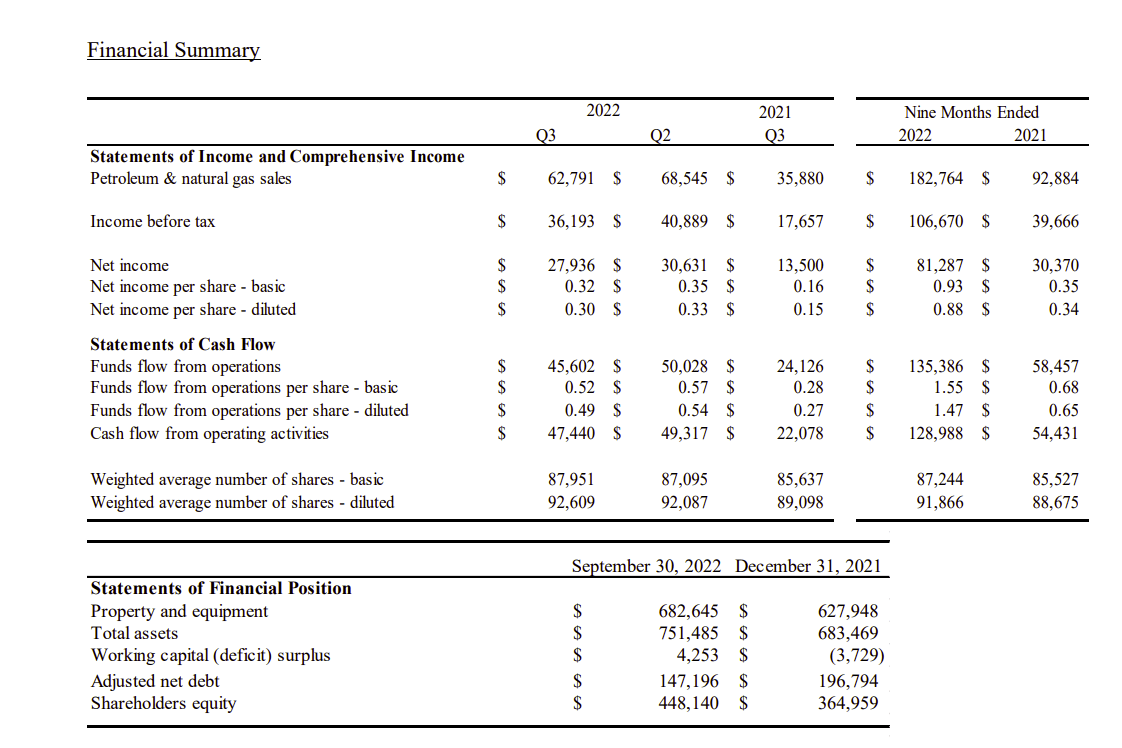

Notice from the first slide that income before income tax is still above 50% of revenue. That is unusually profitable for companies in the oil and gas industry in just about any part of the business cycle. That helps to explain how the company can repay debt while growing production.

The growing production is likely to lead to more proposals like the ones shown above that will keep the very wide income margins before tax.

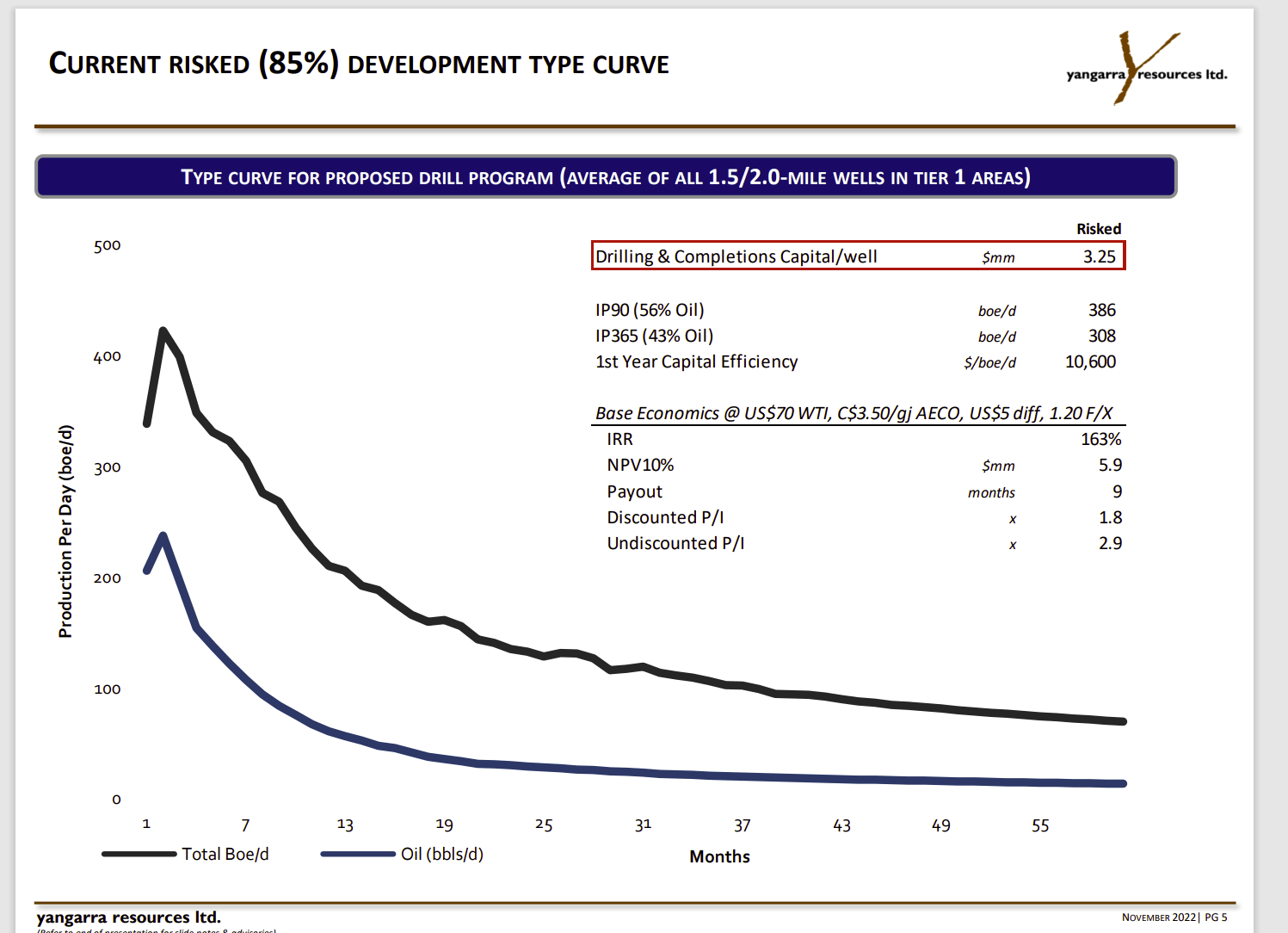

Yangarra Resources Well Profitability Under Very Conservative Assumptions (Yangarra Resources Third Quarter 2022, Corporate Presentation)

{kind=link}

This presentation shows more than adequate well profitability under some very conservative pricing assumptions. This still seems to be the primary driver of company profitability during fiscal year 2020 when a lot of firms lost a lot of money.

The payout of these wells is still very short and, of course, shorter in the currently far more robust commodity price environment. The one thing that has changed materially with the natural gas price of these wells is the increasing value of the later production. These wells have an increasing percentage of natural gas production that made later production not as attractive as earlier production. Now that later (and gassier) production is far more profitable than was the case before the current pricing recovery.

The Future

This Canadian company (reporting in Canadian Dollars) has managed to be profitable since production growth began a few years back. Even though the pandemic interrupted the production growth, the company remained profitable during that very challenging fiscal year for the industry.

Likewise, this is one of the very few companies that is able to dig its way out of a perceived high debt load while growing production. Management appears to be ready to continue to grow production for the foreseeable future while bringing that debt under control.

Shareholder returns are on the future agenda. But the primary objective is likely to be to make the company an attractive acquisition candidate for another company or at some point to be an industry consolidator. The very profitable production already available is a good start, and management has plenty of inventory to expand production as well as other levels to possibly produce as technology advances. In short, this company does not have to acquire any more land in order to grow for years to come.

Any time a company like this one produces from a previously noncommercial interval; it takes time to get adequate records for an accurate idea of production throughout the life of the well. This company is finally getting those records. As management does, this management has taken the unusual step of advising shareholders of every change every time they get more information.

That has worried some shareholders. On the other hand, the wells are still clearly profitable. That is because the initial production when compared to the well costs assures a fast enough payback for the company to assure a reasonable well profit by hedging should that be a necessary strategy. Obviously, these wells will produce for several years after that payback to make these wells extremely profitable under a wide variety of industry pricing scenarios.

This management has built and sold companies before. That takes some of the small company risks out of this investment because the management is unusually experienced (as are some of the directors on the board).

Even though this company is small, and the stock can be volatile as a result, the management strategy appears to be conservative enough to appeal to a wide variety of investors. The low price-to-earnings ratio also provides a measure of safety because it protects against a sustained downside move. As the debt ratio continues to decline, that also increases the safety of this stock.

The stock is probably best as a basket of similar picks. That kind of diversification can provide added safety when dealing with smaller companies and their volatility.

For further details see:

Yangarra Resources: Leaving Past Worries Behind