CA - Yangarra Resources: Mr. Winter Throws A Curve Ball

2023-06-19 07:00:00 ET

Summary

- Mr. Winter caused more idle time than Yangarra Resources' management envisioned.

- The money raised will go to additional drilling. But that drilling will not affect average production as was originally anticipated.

- The debt ratio is very low.

- This company reported a profit in 2020. Yet the market still assigns the stock a price-earnings ratio of about 2.

- The debt will still decline despite the winter weather issues.

(Note: This is a Canadian company that reports in Canadian dollars unless otherwise indicated.)

Yangarra Resources (YGRAF) management raised money to accelerate production growth and end up with a lower debt balance by yearend. However, the winter had other ideas about that plan. Conditions became rough enough that management actually slowed work until field conditions improved.

The problem with that is field conditions improved close to the time of Spring Breakup. But Spring Breakup results in a period of slow field activities until the conditions are dry enough for heavy machinery to move around again. Wildfires are another industry hazard in the area that will usually abate as summer arrives (but not this year of course).

So, all that great planning went out the window. Even if management can still drill all the wells for that planned production increase, the production will get started too late to have the originally intended effect on the average production projection. That has resulted in a new production guidance range that includes potentially lower production levels than planned.

Now that original cash raise will likely head to the bank to reduce the debt amount. But the production that would have done a better job is not a consideration for the current year.

Fortunately, the company remains very profitable with a cash flow that can handle the debt balance. Furthermore, there are reports out that some key raw materials like steel prices are finally on their way down. Should that trend hold until after the Spring Breakup, then there is a chance that management will have cost reductions to aid them in their original plan to increase production faster. It may not be what was originally planned. But in this industry that is just the way things go.

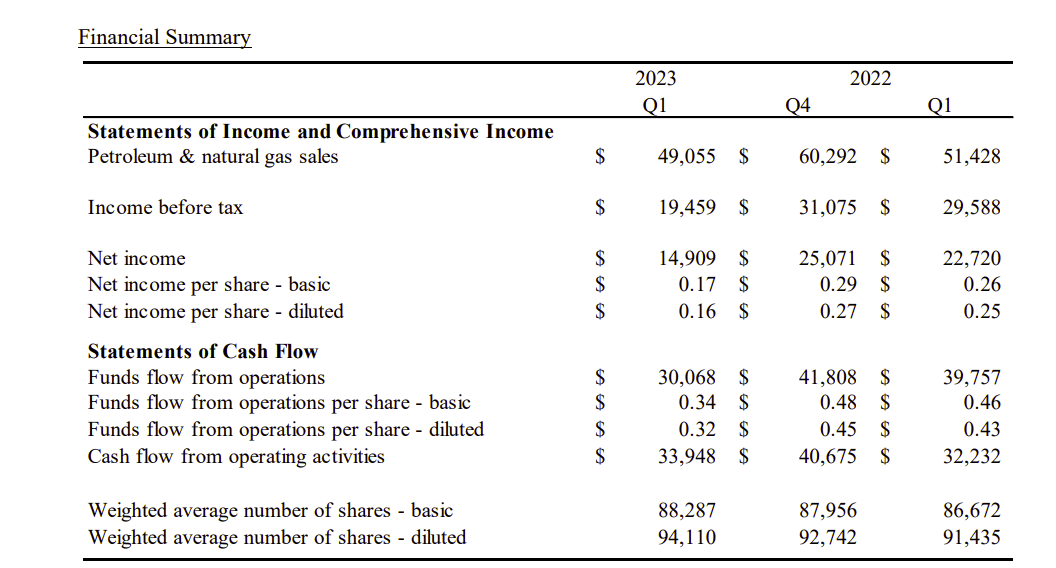

Yangarra Resources Summary Of First Quarter Operating Results (Yangarra Resources First Quarter 2023, Earnings Press Release)

{kind=link}

The market is so worried about lower commodity prices that the stock price declined to maintain that price-earnings ratio of about 2 or less even annualizing the results of the first quarter. Sooner or later, Mr. Market is going to realize that the rather patience-trying results of fiscal years 2015-2020 throughout the industry are not going to repeat. At that point a lot of these stocks will return to normal valuations instead of the currently ridiculous outlook of the market right now.

This is a financially strong company with a debt ratio of less than one that is unusually profitable. That income is an extremely high percentage of sales (as has always been the case). The company has a lot of inventory to continue that rather profitable history well into the future.

Competitive moats are something that appears to be a permanent advantage. In this case, that competitive moat is an interval that the company found long before a lot of competitors and then grabbed a lot of acreage with that same characteristic for a very long future outlook that is among the best in the industry.

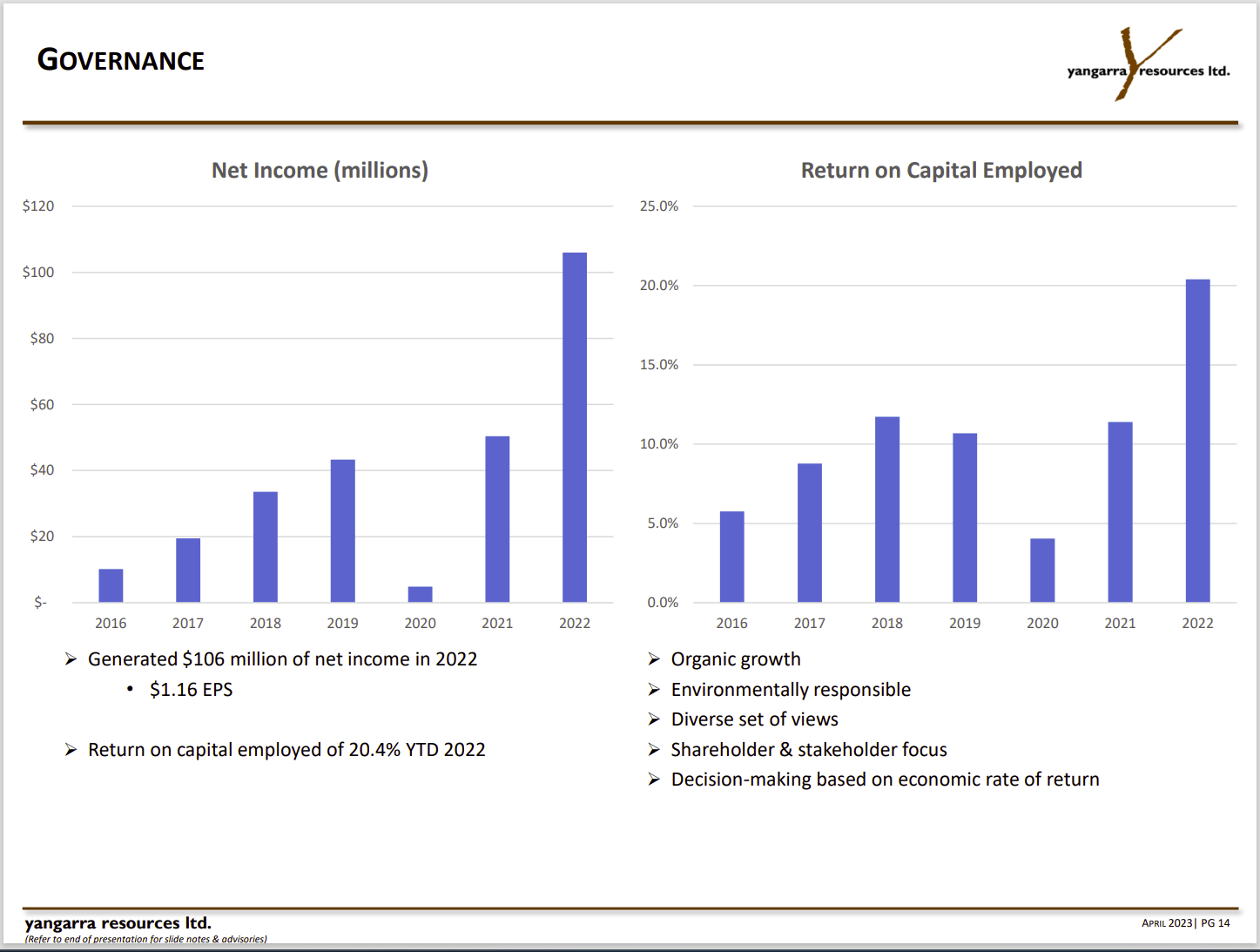

Yangarra Resources Profitability And ROC History (Yangarra Resources April 2023, Investor Presentation)

{kind=link}

Yangarra is a company that reported a profit in fiscal year 2020 which much of the industry reported losses and impairment charges. A company that can do that is going to have a very easy time in the current environment. This also lends credence to the idea that the current profit margin is not due to aggressive accounting.

The other thing is that the return on capital employed shown above is something you rarely see in this industry. That current 20% combined with a profitable ROC in 2020 is rare even for the larger and more established industry leaders.

As noted above, Yangarra is very unlikely to join the current industry trend to grow by acquisition. The reason is that the well profitability of this particular area is hard to match in an acquisition.

Now industry activity in this zone and this area is beginning to increase as yet another major low-cost interval comes online in a big way to compete with more established plays like the Permian in the United States. Anyone who thinks we are running out of prime low-cost acreage to drill is just not paying attention because small players like this one keep identifying new profit opportunities and then the more established crowd moves in (with greater press coverage).

As long as this kind of discovery followed by more industry activity keeps "popping up" every few years, then there are no worries about "Tier 1" acreage long term. It may happen in different countries or even offshore like the Guyana discoveries. But it would appear that technology keeps advancing to move more acreage and more intervals into the low-cost column that attracts this industry.

When management has published well payback calculations, it has been in months even during periods of weak industry pricing. A current calculation is not available right now. But that will likely change for the better as industry technology advances in the future. That is a condition that is responsible for management being able to guide to debt reduction while growing production.

In the future, management is likely to continue to grow production at double digit rates while repaying long-term debt. Any time management decides to raise money (as they did in the current fiscal year), that extra money simply accelerates the pace. But this company has demonstrated sufficient progress so that they do not have to raise money to have a decent balance sheet with growing production.

Conclusion

A company like this is actually a fairly safe investment because management is very experienced at building and selling companies. The finances are strong. Meanwhile that profit in fiscal year 2020 adds a level of investment safety that one seldom sees in larger more established companies. Then there is that low price-earnings ratio that is very unlikely to go lower. In fact, the stock price could triple from current levels and that price-earnings ratio would still be crazy-low. That just shows how out-of-favor the current oil and gas industry is.

Sometimes, very good things come in small packages. A company that is able to report a profit in fiscal year 2020 (however small) is very unlikely to lose money in the future under a wide variety of industry conditions. This company can grow production profitably in what many competitors would consider hostile conditions that cause them to idle their equipment. The future of this company is unusually good and unusually safe for a small upstream producer.

For further details see:

Yangarra Resources: Mr. Winter Throws A Curve Ball