YELP - Yelp: Appears Expensive With A Small Moat

2023-05-03 17:00:40 ET

Summary

- On initial examination, Yelp appears to be a conservatively financed business generating large amounts of consistent free cash flow.

- The company faces heavy competition, but is etching out a niche for itself by partnering with local service based businesses.

- When stock-based compensation is taken into account, shareholder returns are muted and the current market capitalization of $2 billion appears far too expensive.

- Total users of mobile and desktop website have been trending down to flat over the last few years.

Executive Thesis

Value investors might be interested in Yelp ( YELP ) as it is conservatively financed, generates large amounts of free cash flow and consistently buys back stock. Indeed, in FY 2022, the company generated $160 million in free cash flow, and is currently selling at a market capitalization of $2 billion. Despite all this cash they appear to be generating, share price performance has generally been abysmal and a closer look is warranted to understand why. It appears that high stock-based compensation has consistently taken away from any shareholder returns, alarmingly with 2022 FCF being adjusted to $4.24 million when this is taken into account.

The Business

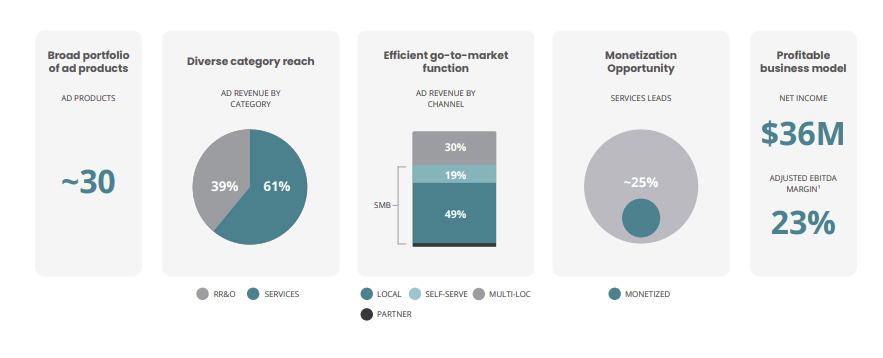

Yelp operates a website and mobile application with the goal of connecting consumers to great local businesses. When I first think of Yelp, I think of checking reviews for restaurants, but the company has reviews and information on all sorts of consumer serving businesses. Yelp has more recently been focusing on partnering with small local businesses such as plumbing, to advertise and connect nearby consumers to the services. Interestingly, this appears to be the larger portion of their revenue, as shown below:

{kind=link}

Only 39% of ad revenue comes from "RR&O" or restaurant, retail and other with the rest coming from local service-based businesses. Moving forward, the company would like to increase monetization from these businesses, reporting currently only 25% of leads are generating revenue. This is an interesting niche for Yelp, and it also offers features such as "request a quote" to generate leads.

Despite these avenues for growth, total unique users of Yelp appear to be trending down to flat. Unique mobile and desktop users over the last 5 years can be demonstrated below:

Company Data

This downtrend can likely be attributed to the low moat nature of the business, but credit needs to be given as 2020 was an abnormal year. Yes, the company is already well established with local businesses and with a review database, but it's pretty easy for new players to enter the field. It also has to fight for ad market share with behemoths such as Google ( GOOG ) (GOOGL). Often when I am looking for any nearby local business, I'll pull up Google Search on my desktop or phone browser, and easily find what I need.

High Stock Compensation

Yelp is a good case study as to why it is so important to look at stock-based compensation. In its best year over the last 5, the company has earned $46 million in free cash flow when adjusting for stock-based compensation. With this adjustment, free cash flow in 2022 was only $4 million, with stock-based compensation almost equivalent to free cash flow. To me, these numbers are unacceptable but perhaps if the company used cash instead of stock for compensation, YELP would not be trading at such a premium. Using stock for such a large proportion of expenses and having no long-term debt also indicates the company was not taking advantage of low interest rates when they were available. These data can be visualized below:

Yelp Adjusted FCF (Data from Morningstar)

Valuation

I wanted to take an optimistic approach to my valuation, as I believe this is the most convincing way to demonstrate the shares are trading at a premium. On the plus side, the company is pretty conservatively capitalized, with no long-term debt on the balance sheet. Because of this, I decided to use a 10% discount rate, as this is likely the minimal return equity investors would expect. I assumed the company would be able to return to growth following a tough few years and grow free cash flow at a 15% CAGR net of high stock-based compensation. The company would then have a terminal growth rate of 2% until its eventual decline, as the company has minimal moat and likely will not continue to grow as fast as global GDP. These assumptions are demonstrated as follows:

{kind=link}

Even with these optimistic assumptions, our models put the fair value of YELP at around $1.2 billion, suggesting approximately 40% downside from the $2 billion market cap at time of writing.

Inverting the Thesis

Recent Years Have Been Difficult

Extrapolating valuation from pandemic and post-pandemic years may be misleading as the restrictions likely had a large impact on use of the platform for recommendations when traveling, eating out or partaking in other paid experiences. As the economy recovers, Yelp may have much better returns than I anticipated. That being said, if we look at pre-pandemic years, there has also been a history of shareholder value slipping from 2014-2019.

There May be a Stronger Moat

I personally do not give the company much credit for having a strong moat, as there appears to be endless competition in their industry from smaller players and from big tech. Though there is competition, the company's website appears to have plenty of engagement, with a reported near 100 million unique visitors this year when aggregating mobile and computer users. The high number of users combined with plenty of already established reviews on the platform could indicate loyalty to the service.

Strong Balance Sheet

The company may deserve to trade at a premium, as it has a strong balance sheet with no long-term debt other than leases, stockholder's equity of $700 million, and $300 million of current assets net of total liabilities. Though this strong balance sheet has come at the expense of shareholders with high stock-based compensation, this may allow the company to be more flexible than its more highly leveraged peers.

Conclusion

I do not consider Yelp to be a particularly attractive investment at current prices, given the recent low free cash flow generation relative to market capitalization, high stock-based compensation and heavy competition. Our models also indicate approximately 40% downside from current prices, with an estimated value for the company of $1.2 billion using optimistic assumptions. This may be slightly offset by the strong balance sheet, with $700 million in stockholder's equity at the end of FY 2022 and no long-term debt. I do expect Yelp to continue chugging along profitably, as it does have somewhat of a moat with its large reviews database and established good reputation and partnerships with local businesses. That being said $2 billion appears far too expensive for investors to be sure they're receiving an adequate margin of safety.

For further details see:

Yelp: Appears Expensive With A Small Moat