YELP - Yelp: Growth In Short To Medium Term Potentially Modest

Summary

- While Yelp has continued to see growth in advertising revenue, such growth has started to plateau.

- Earnings growth has also started to moderate.

- Yelp could see modest growth in the short to medium term due to rising costs and a potential slowdown in advertising demand across the restaurant business.

Investment Thesis: Yelp could see modest growth in the short to medium-term due to rising costs and a potential slowdown in advertising demand across the restaurant business.

In a previous article back in January, I made the argument that Yelp ( YELP ) could be poised to see a rebound in growth on the basis of continued revenue growth as well as strong performance across the Restaurants and Home Services business.

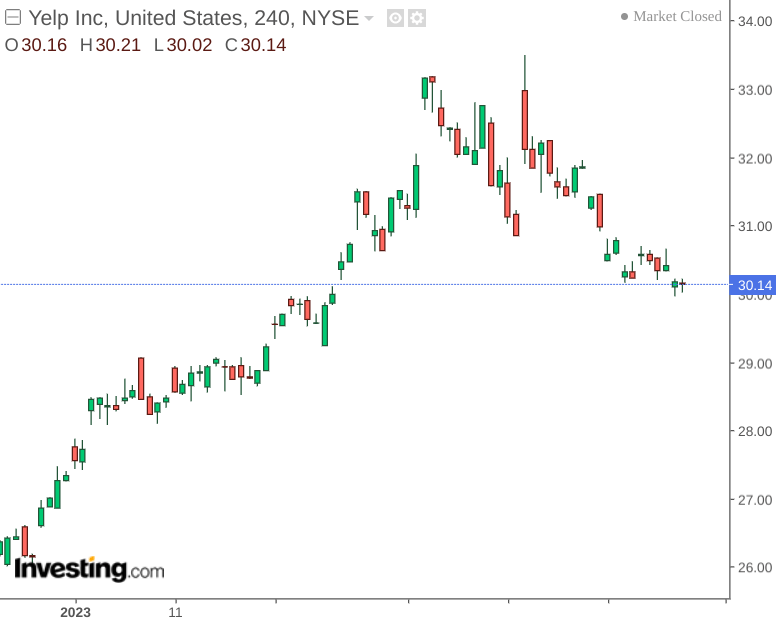

Since my last article, the stock is up by just over 5%:

{kind=link}

The purpose of this article is to assess whether Yelp could continue to see further upside from here, particularly taking recent quarterly performance into consideration.

Performance

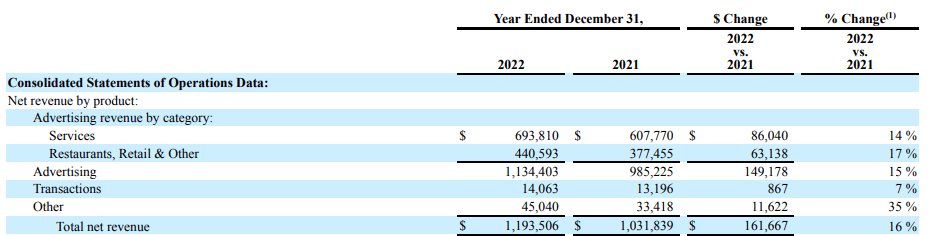

When looking at net revenue by product across the company's full-year results - we can see that all except Transactions saw double-digit growth on a yearly basis.

{kind=link}

Moreover, total net revenue for the year as a whole was up by 16%, which is in line with the growth of 17% that we saw for the nine months ended September 2022 .

Additionally, when looking at advertising revenue for 2022 as a whole - we can see that Q4 2022 revenue is substantially higher than that of last year, but growth seems to be plateauing - with negligible growth from Q3 to Q4 of 2022.

Figures sourced from Yelp historical quarterly reports. Heatmap generated by author using Python's seaborn.

It is notable that on a three months ended basis, Services saw growth of just over 13% while that of Restaurants, Retail & Other saw growth of just over 11%.

{kind=link}

I had previously made the point that with Yelp having significant exposure to the restaurant industry - growth in advertising revenue had been vibrant in spite of inflationary pressures. With that being said, there is a possibility that growth across this sector could start to plateau as inflationary pressures continue to place upward pressure on prices and the post-COVID recovery starts to plateau.

Specifically, Fitch Ratings is forecasting that while restaurants will see higher profits as a result of higher prices - sales volumes will weaken.

While this may be good news for the restaurant industry - it may cause headwinds for advertising demand if profitability becomes less dependent on volume and consumers increasingly reduce levels of discretionary spending.

In this regard, I take the view that investors will be looking for evidence that advertising revenue as a whole can continue to see growth in the next quarter. Should we see a plateau in growth, or indeed a decline in growth from the Restaurants, Retail & Other segment, then we could see growth in the stock plateau in the short to medium-term.

From a balance sheet standpoint, Yelp seems to be performing well. When looking at the company's quick ratio (calculated as cash plus marketable securities plus accounts receivable all over current liabilities), we can see that while this ratio has seen a fall over the past year - it still remains well above 1. This indicates that Yelp has more than sufficient liquid assets to cover its current liabilities.

| December 2021 |

| December 2022 |

| Cash and cash equivalents |

| 479783 |

| 306379 |

| Marketable securities |

| 0 |

| 94244 |

| Accounts receivable |

| 107358 |

| 131902 |

| Current liabilities |

| 164013 |

| 182824 |

| Quick ratio |

| 3.58 |

| 2.91 |

Source: Figures sourced from Yelp Inc. 2022 Annual Report on Form 10-K. Figures provided in thousands of U.S. dollars, except the quick ratio. Quick ratio calculated by author.

Risks and Looking Forward

Going forward, the main risk that I see to Yelp at this point in time is a plateau in advertising revenue - particularly if we see further weakening of sales growth across the restaurant industry.

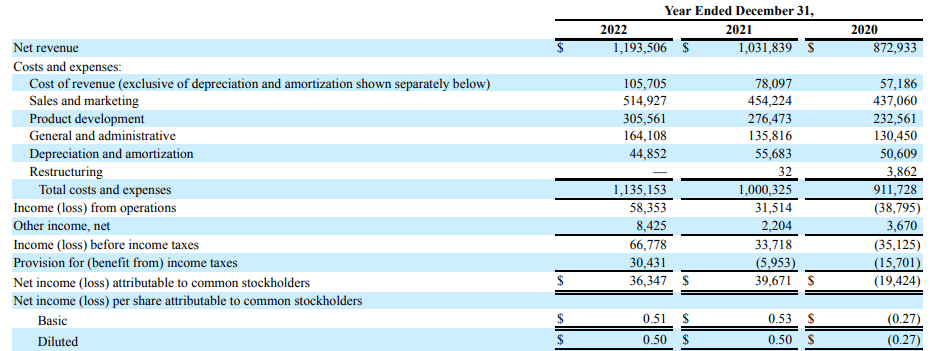

We can see that while growth in net revenue has continued - growth in net income (diluted) has stalled over the past year:

{kind=link}

In this regard, continued inflationary pressures could mean further upward pressure on cost of revenue.

Conclusion

I ultimately take the view that while Yelp has the capacity to grow advertising revenue further over the longer term, rising costs and a potential slowdown in advertising demand by the restaurant industry could hinder growth in the short to medium term.

For further details see:

Yelp: Growth In Short To Medium Term Potentially Modest