YELP - Yelp: Incredibly Strong Advertising Execution

2024-01-15 00:17:54 ET

Summary

- Yelp's stock has tumbled 6% since the start of the year, creating an opportunistic entry point for investors.

- Yelp has become a reliable hub of information on local businesses, making it a trustworthy platform for reviews.

- Yelp's most recent results showcased a strong acceleration in ad clicks, highlighting strong consumer engagement on the platform.

- The stock trades at just ~6x forward adjusted EBITDA, leaving plenty of room for upside.

2024 is going to be a stock pickers' market. So far in the first few trading weeks of the year, the major market indices have swung between gains and losses, but underneath the hood, many stocks especially in the tech sector have swung considerably (EV stocks have tanked, while software and internet names have largely hung on to their December rallies). The way to beat the markets this year is to be choosy on stocks that have very specific upside catalysts as well as an appealing valuation.

And that sometimes means choosing less-obvious, less-popular names like Yelp ( YELP ). The local reviews site is up 50% over the past year, but it has tumbled ~6% since the start of the year - creating what I believe to be quite an opportunistic entry (or doubling-down) point.

I last wrote a bullish note on Yelp in July, when the stock was trading in the high $30s. Since then, Yelp has released a string of strong quarterly results, boosted by a resurgence in advertising demand (though enterprise budgets have softened amid fears of a recession, consumer spending remains up - which is translating to healthy demand for Yelp's services and restaurant clients). And so even with the upward jump in Yelp's valuation (counterbalanced by rising forward expectations), I remain quite bullish on Yelp.

When we zoom out at the long term, one thing to consider is that in this more distributed economy - where we lean toward online marketplaces to put us in contact with virtual strangers to deliver almost every service (from short-distance rides to home repairs), the concept of trust - and thus, trustworthy reviews - has become paramount.

In its Q3 shareholder letter, Yelp cited a study by the FTC that found that Yelp's ratings distribution appeared more balanced and fair than competitors like Facebook ( META ) and Google ( GOOG ):

Yelp ratings distribution (Yelp Q3 shareholder letter)

In other words, Yelp has become a reliable hub of information on local businesses - which has become the company's moat.

For investors who are newer to Yelp, here is my full long-term bull case on the stock:

- New categories like Home Services and driving growth for Yelp. Though we know Yelp largely for its traditional dominance in restaurant reviews, recent growth has stemmed from newer categories such as Home Services. As the pool of categories that people rely on Yelp for local reviews grows, so will Yelp's available pool of advertisers.

- Focus on multi-location customers. Yelp is also away from its traditional stronghold of focusing on local businesses and restaurants and going after large, multi-location national chains. These deep-pocketed advertisers benefit from reaching consumers on a platform known for its truthful and useful reviews, and Yelp benefits from having high-contribution recurring clients. Yelp is reshaping its sales teams to cut down on account executives focused on lower-dollar customers (the Local sales headcount is at 50% of pre-pandemic levels) and is instead hiring much higher-ROI salespeople focused on enterprise customers.

- Sales segmentation (between self-service and multi-location customers) has not impacted account growth. Yelp continues to grow its paid advertiser accounts at a healthy pace thanks to the success of its self-service channel, and the average spend per account is also gliding upward.

- Rising margins and profit-minded management. Yelp was an early reactor to the pandemic and aggressively laid off/furloughed a large portion of its sales team. The company considered this move as part of a broader push (even before the pandemic) to cut down its Local (small business-focused) sales teams, hire more Enterprise-facing account executives, and shift staff away from its San Francisco headquarters and to geographically cheaper locales. Yelp's remote-work policy and decision to reduce its real estate footprint will also pad its bottom line.

Stay long here - there's plenty of upside to go.

Q3 download

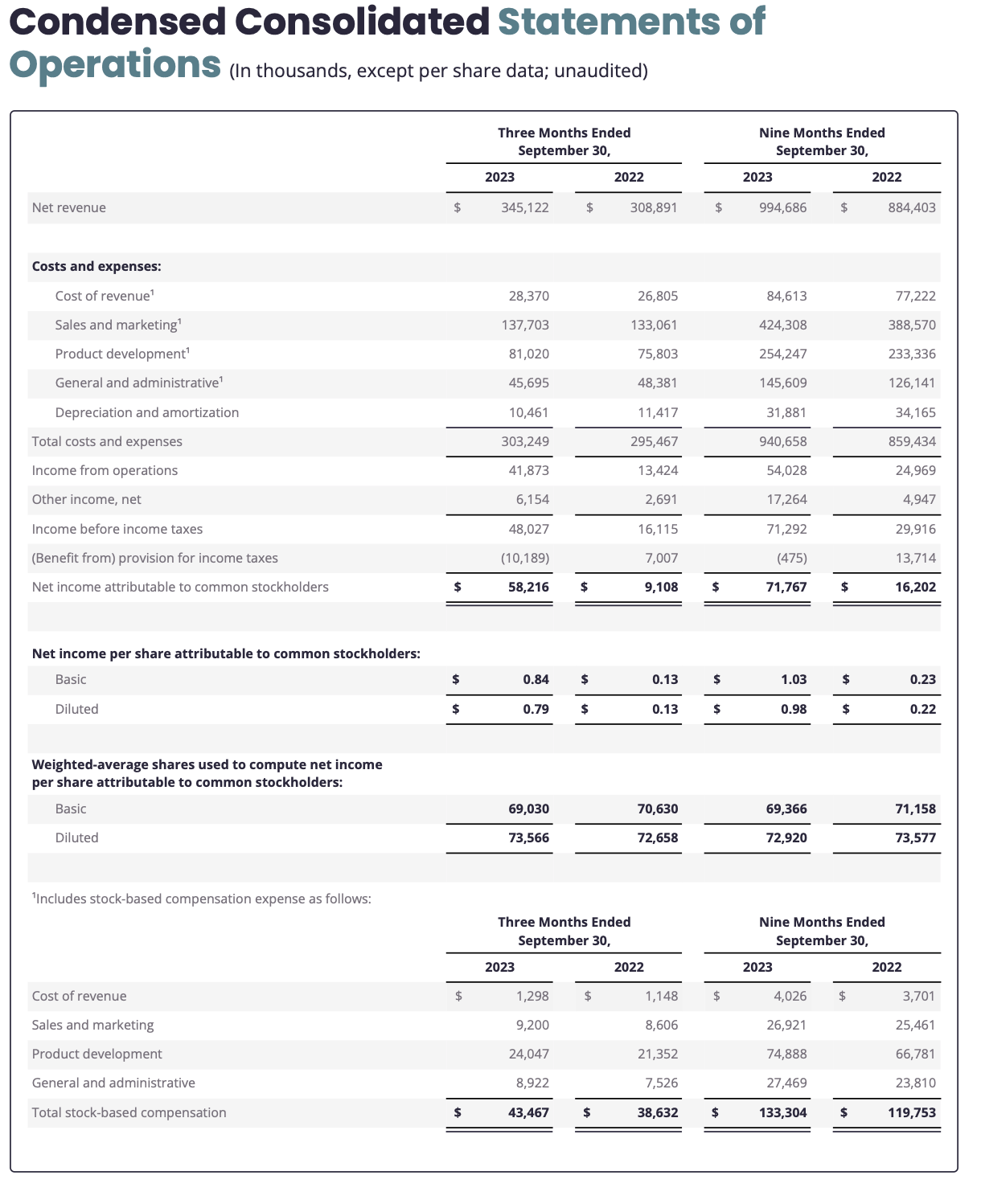

Yelp's latest quarterly results demonstrate a lot of the momentum recovery that will be key for the stock to sustain in 2024. Take a look at the Q3 earnings summary below:

Yelp Q3 results (Yelp Q3 shareholder letter)

{kind=link}

Revenue grew 12% y/y to $345.1 million, ahead of Wall Street's $341.0 million (+10% y/y) expectations.

Top line strength, meanwhile, was driven by a sharp jump in ad clicks, demonstrating strong consumer engagement on the Yelp platform. Q3 saw a 9% y/y growth in ad clicks, versus flat behavior in Q1 and Q2. Home Services continues to be a major category leader for Yelp, especially as the company doubles down on its "Request a Quote" feature. Revenue from Home Services ads grew 20% y/y, underneath a Services category total growth of 14% y/y.

Yelp ad clicks (Yelp Q3 shareholder letter)

Meanwhile, robust advertiser demand also has cost per click continuing to rise, up 4% y/y in Q3. Note that the primary reason that CPC growth decelerated from Q2 was due to lapping a sharper advertising recovery in Q3 of last year.

Yelp CPC rates (Yelp Q3 shareholder letter)

Here's helpful anecdotal commentary from CEO Jeremy Stoppelman's remarks on the Q3 earnings call , detailing the advertising strength the company has seen as well as the opportunity ahead:

With record advertising demand in the quarter, our efforts to deliver more value to advertisers has clearly resonated. The product improvements we've made to enhance our ad formats and ad system drove more high-quality clicks to our customers in the third quarter. In fact, ad clicks returned to year-over-year growth, increasing by 9% from the prior-year period, a marked improvement from flat year-over-year growth in the second quarter.

At the same time, year-over-year growth in average CPC moderated compared to the second quarter, at 4%. We also made progress against our initiative to drive sales through our most efficient channels. Self-serve revenue increased by 25% year-over-year, while multi-location revenue increased by 10% year-over-year. At a combined 51% of advertising revenue, we continue to see significant opportunities to grow each channel in the years ahead."

But in spite of double-digit top-line growth, Yelp is noting that it will end 2023 with a flat y/y headcount - a testament to the company's profit-oriented mindset.

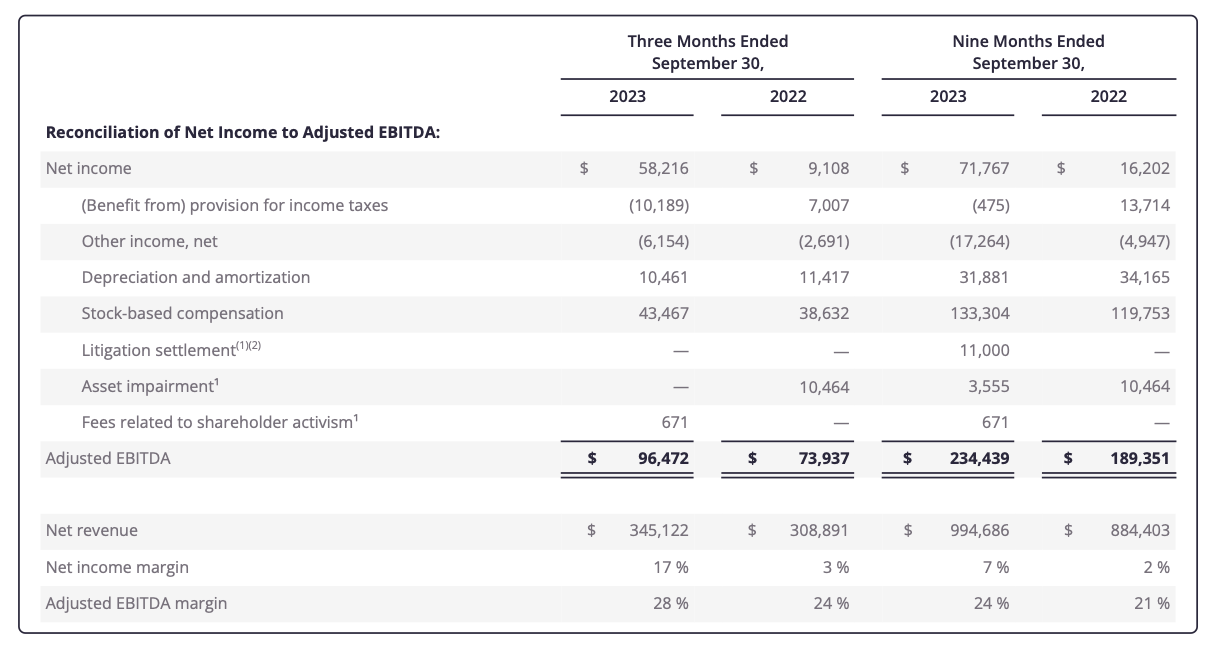

Strong cost management has helped the company boost adjusted EBITDA, up 31% y/y to $96.5 million in the third quarter, also representing four points of margin expansion y/y to 28%.

Yelp adjusted EBITDA (Yelp Q3 shareholder letter)

{kind=link}

Note as well that GAAP net margins jumped 13 points to 17% while diluted GAAP EPS also increased 6x y/y, showcasing that Yelp's profits aren't all on an adjusted basis either.

Valuation and key takeaways

At current share prices near $44, Yelp trades at a market cap of $3.00 billion. After we net off the $426.6 million of cash on Yelp's most recent balance sheet, its resulting enterprise value is $2.57 billion.

For the current fiscal year FY24, Wall Street analysts are expecting Yelp to generate $1.46 billion in revenue, representing 9% y/y growth. Assuming the company holds onto its current 28% adjusted EBITDA margin, adjusted EBITDA next year would be $409 million (+27% y/y versus this year's $319-$324 million adjusted EBITDA guidance range) , putting Yelp's valuation at just 6.3x EV/FY24 expected adjusted EBITDA.

To me, that leaves quite a bit of room for multiples expansion this year, which is one of the core reasons I like Yext on top of its strong recent execution.

For further details see:

Yelp: Incredibly Strong Advertising Execution