YELP - Yelp: Momentum Is Picking Up Steam

2023-07-11 09:00:00 ET

Summary

- Yelp's stock is up 34% year to date, outperforming the S&P 500, due to stronger fundamentals and increased advertiser demand.

- Yelp is expanding into new categories such as Home Services and targeting multi-location national chains, which is driving growth.

- Despite a shift in sales strategy and pandemic-related layoffs, Yelp continues to grow its paid advertiser accounts and is expected to boost its adjusted EBITDA.

- Potential acquirer interest after recent activist noise may help Yelp to recover faster to a fair valuation.

Amid uncertainty over the direction of the markets for the balance of the year, I continue to advocate careful single-stock selection as the best way to position our portfolios. This often means diving into less-popular names that no longer get much mainstream buzz.

Yelp ( YELP ), in particular, has been a fortuitous call this year that I think will have further upside. The online-reviews site is up 34% year to date, roughly doubling the performance of the S&P 500. The stock's strength has been predicated on both stronger fundamentals, with the company raising its adjusted EBITDA outlook for the year on the back of healthy advertiser demand, as well as news of activist pressure pushing Yelp management to explore a sale.

Even standalone, Yelp is a profit powerhouse

A cardinal rule of my investment strategy is to never bank on an external factor (such as an acquisition) to purely drive the investment thesis for any stock. In the case of Yelp, I think this company is undervalued whether it gets purchased or stands alone. In spite of YTD strength, I'm continuing to hold onto Yelp in my portfolio and remain bullish on the stock.

Recent results (we'll dig into Yelp's Q1 success in the next section) showcase that Yelp is benefiting from a recovery in advertising demand. In addition, company-specific initiatives to bolster its dominance in the Services category are bearing fruit. And with ad clicks recovering after multiple quarters of decline, and Yelp poised to benefit from both headcount streamlining and talent shifting/real estate reductions to cheaper locales, I think there are plenty of drivers for Yelp to boost its adjusted EBITDA.

Here, in my view, is the updated long-term bull case for Yelp:

- Growing in new categories. Though we know Yelp largely for its traditional dominance in restaurant reviews, recent growth has stemmed from newer categories such as Home Services. As the pool of categories that people rely on Yelp for local reviews grows, so will Yelp's available pool of advertisers.

- Focus on multi-location customers. Yelp is also away from its traditional stronghold of focusing on local businesses and restaurants and going after large, multi-location national chains. These deep-pocketed advertisers benefit from reaching consumers on a platform known for its truthful and useful reviews, and Yelp benefits from having high-contribution recurring clients. Yelp is reshaping its sales teams to cut down on account executives focused on lower-dollar customers (the Local sales headcount is at 50% of pre-pandemic levels) and is instead hiring much higher-ROI salespeople focused on enterprise customers.

- Sales strategy shift has not impacted account growth. Yelp continues to grow its paid advertiser accounts at a healthy pace thanks to the success of its self-service channel, and average spend per account is also gliding upward.

- Focus on efficiency. Yelp was an early reactor to the pandemic and aggressively laid off/furloughed a large portion of its sales team. The company considered this move as part of a broader push (even before the pandemic) to cut down its Local (small business-focused) sales teams, hire more Enterprise-facing account executives, and shift staff away from its San Francisco headquarters and to geographically cheaper locales. Yelp's remote-work policy and decision to reduce its real estate footprint will also pad its bottom line.

- Consistent buybacks. Yelp has been consistent in its shareholder returns program, and has $232 million remaining on its current authorization. This is more than well supported by its balance sheet cash, which is unencumbered by debt.

Valuation remains mild

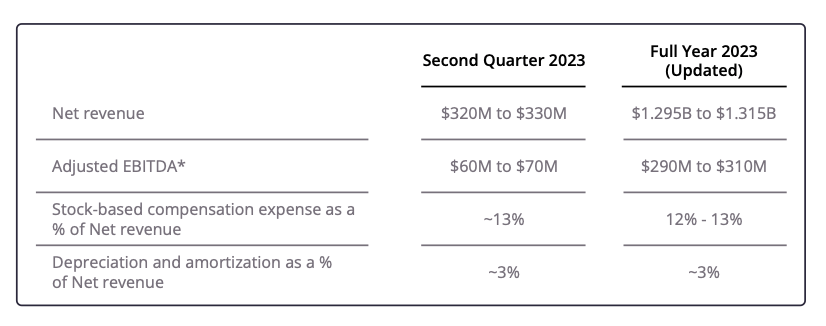

Key to note is the fact that Yelp recently boosted its full-year revenue outlook:

{kind=link}

The company is now expecting revenue of $1.295-$1.315 billion (+9-10% y/y), versus a prior outlook of $1.29-$1.31 billion; and adjusted EBITDA remains constant to the prior outlook of $290-$310 million (a 23% margin at the midpoint).

At current share prices near $37, Yelp trades at a market cap of $2.56 billion. After we net off the $400.6 million of cash on Yelp's most recent balance sheet, the company's resulting enterprise value is just $2.16 billion, putting the stock's valuation at 7.2x EV/FY23 adjusted EBITDA.

Considering adjusted EBITDA is still growing at a low-teens pace in line with revenue, my year-end price target on Yelp stands at $49, representing a 10x FY23 adjusted EBITDA multiple and 32% upside from current levels.

Q1 download

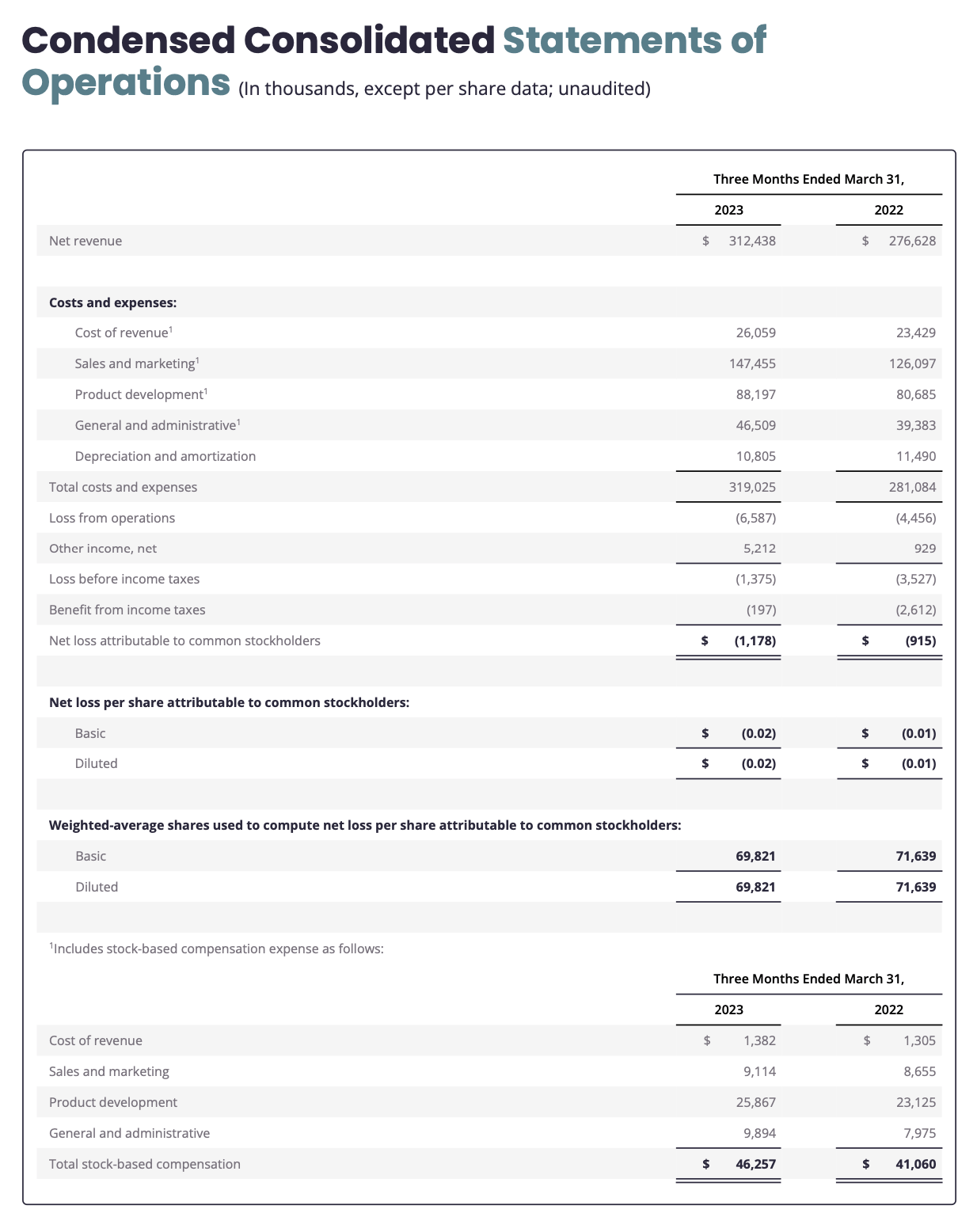

Yelp showcased strength on a number of fronts in its most recently reported quarter. Take a look at the Q1 earnings summary below:

{kind=link}

Revenue grew 13% y/y to $312.4 million, beating Wall Street's expectations of $305.7 million (+11% y/y) by a two-point margin. It's worth noting that Yelp's revenue kept pace with 13% growth in Q4, despite most other companies in the software/internet sectors reporting substantial sequential deceleration owing to macro decay.

In fact, it's also worth noting that Yelp's ad clicks returned to positive 1% y/y growth in Q1, after shouldering three straight quarters of declines:

Yelp ad clicks (Yelp Q1 shareholder letter)

And while Yelp's core restaurant and retail categories showed solid 10% y/y growth in advertising revenue, Yelp is building up new proficiency in the Home Services space, which saw 25% y/y growth in ad revenue in Q1. This is driven by strong customer response to Yelp's "request a quote" feature.

Yelp Home Services category revenue (Yelp Q1 shareholder letter)

Speaking to advertiser demand on the Q&A portion of the Q1 earnings call, CEO Jeremy Stoppelman noted as follows:

So, we’re feeling really great about advertiser demand. Clearly, they’re seeing that our leads are high quality, are down funnel that the consumers that they’re interacting with are motivated. But that said, we’re also working on the product side to continually improve our offering, both on the ad matching side, which is underlying request a quote, but then also on request a quote itself streamlining things. You may have seen our product announcements in there with password-less login. So, that reduces friction.

There is also a really big initiative that we’ve started rolling out called Yelp Guaranteed, where we stand behind service providers, advertisers, and help them close that business with consumers by offering Yelp Guaranteed. You can imagine, this could particularly help a newer business and maybe hasn’t had the chance to build up the reputation in the same way as someone more established. So, we do have a lot of investments in that area to continue to grow the overall number of requests to close. Obviously, macro plays a role here. And I think if you look across the peer group of companies, there’s soft trends out there. But even despite the overall consumer demand, I think we’re making really good progress on the product side. And we’re certainly seeing the demand from businesses remain quite strong and gaining share there."

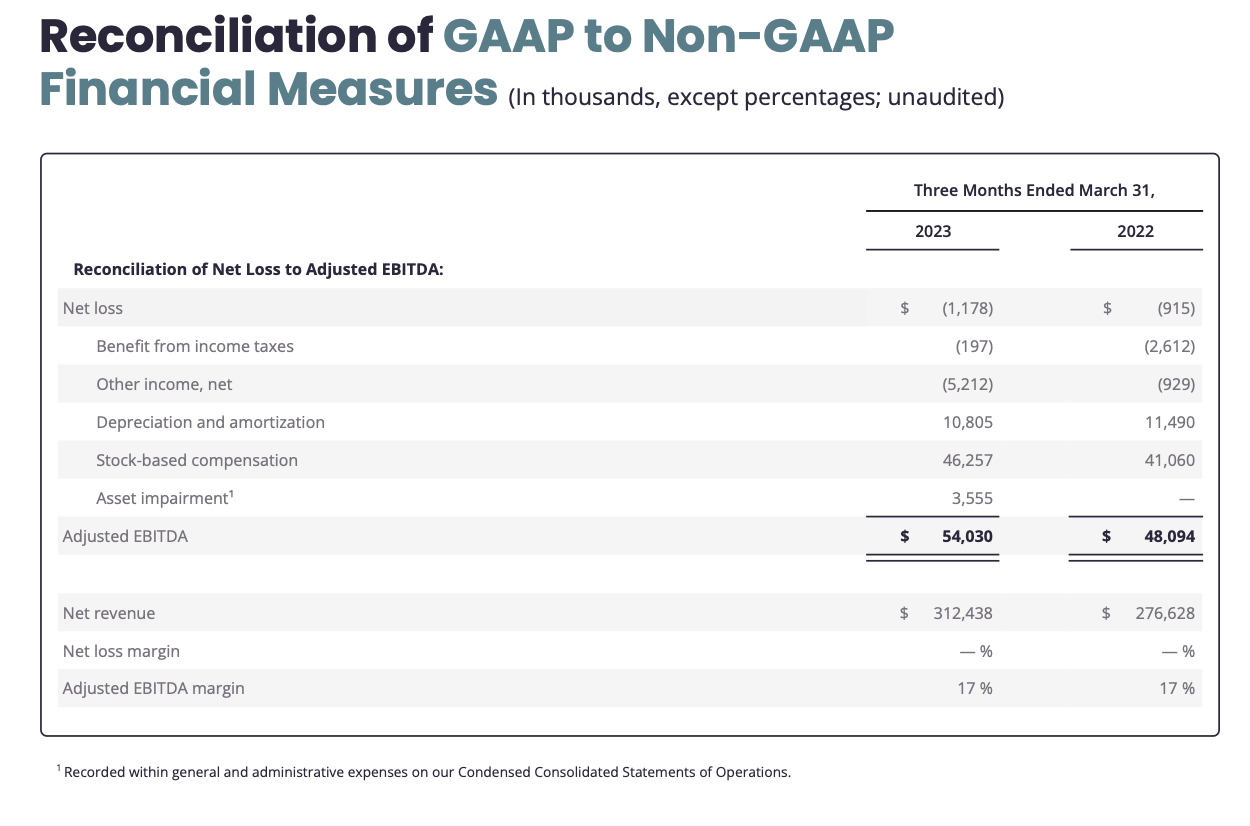

Strong top-line trends have also flowed to the bottom line, where adjusted EBITDA grew 13% y/y in line with revenue to $54.0 million, representing a 17% adjusted EBITDA margin.

{kind=link}

The company expects adjusted EBITDA to continue seeing operating leverage throughout the balance of the year as workforce reductions and real estate eliminations kick in.

Key takeaways

Irrespective of whether acquirer interest continues to build in Yelp, I find that the stock is substantially undervalued at ~7x current-year adjusted EBITDA, despite double-digit growth in both the top and bottom line. With recovering advertiser demand and Yelp successfully broadening its reach into new categories beyond restaurants and retail, I think now is a great time to invest in Yelp.

For further details see:

Yelp: Momentum Is Picking Up Steam