YELP - Yelp Q3: Still No Respect

2023-11-07 15:09:54 ET

Summary

- Yelp Inc. reported strong growth in Q3 2023, with adjusted EBITDA soaring 30% YoY and revenues in the Home Services category growing at a 20% clip.

- The company has made significant improvements in profits, with adjusted EBITDA at 28% of revenues and a forecast for strong growth.

- Despite the stock trading at recent highs, Yelp is exceptionally cheap trading at 7.5x '24 EV/EBITDA targets.

Yelp Inc. ( YELP ) reported yet another quarter of strong growth and the stock just limped to recent highs. The consumer review site has a strong history of growth mostly ignored by the stock market. My investment thesis is ultra Bullish with the consumer review site trading at only $45.

Source: Finviz

Ignored Growth

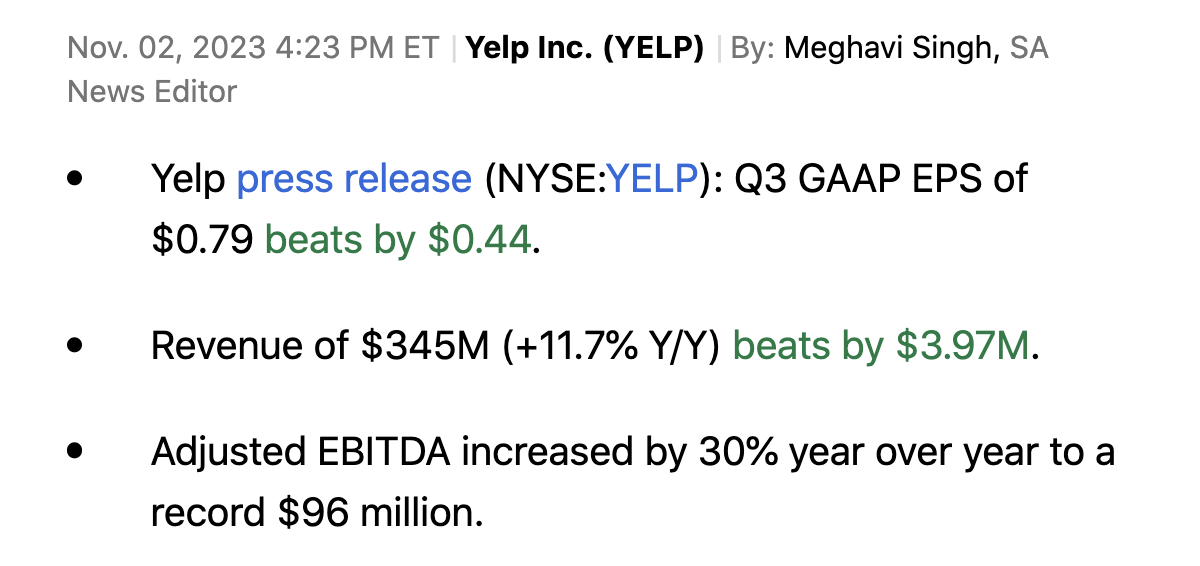

A lot of companies are happy to just grow sales these days, yet Yelp just reported nearly 12% growth in Q3 '23. The company again easily soared past consensus estimates as follows:

{kind=link}

Yelp continues a path of profitably growing, with adjusted EBITDA soaring 30% YoY to $96 million. The company has continued to improve ad formats leading to a 9% YoY boost in ad clicks with the CPC up only 4%.

The consumer review site has quietly gone from a restaurant review site to a Home Services business. Revenues in the last category are still growing at a 20% clip, with overall Services now accounting for $206 million of quarterly revenue in Q3'23.

Source: Yelp Q3'23 presentation

The company launched Yelp Guaranteed for customers setting up projects through the Request-a-Quote flow providing a $2,500 guarantee to work with verified contractors. The consumer review site has more traction with these large projects where consumers want a trusted partner versus random restaurant visits.

In addition, Yelp has become far more efficient with the sales department by focusing on self-serve and multi-location customers. These business either don't require the same sales work or provide the revenue base of a multi-location enterprise to warrant a sales department engaging with the customer.

In the process, Yelp has made massive improvements in profits with adjusted EBITDA at 28% of revenues now, up 400 basis points from Q2'22. Just as important, the company forecast strong adjusted EBITDA growth.

Still Cheap

Yelp Inc. stock has jumped to $45, but the market cap is only $3.1 billion. The enterprise value quickly dips to only $2.7 billion with a cash balance of $427 million.

Yelp guided to 2023 adjusted EBITDA of $319 to $324 million, up from previous guidance of $310 to $320 million. An investor should quickly see how the stock trades with an EV of below 10x the EBITDA targets for the year with only 2 months left. Remember, adjusted EBITDA just grew at a 30% clip in the last quarter and the annual target is for growth of nearly 20%.

A stock with these growth rates would normally trade with a valuation of at least 20x forward EV/EBITDA targets. The current analyst estimates forecast only $356 million for 2024, but Yelp is likely to soar past those numbers depending on the actual shift to cash compensation impact.

Even keeping this adjusted EBITDA target for 2024, Yelp is extremely cheap. The company likely grows EBITDA much close to 15% with revenue likely to reach double-digit growth rates again.

Yelp trades at only 7.5x EV/EBITDA targets of $356 million in 2024. Though, one of the bigger disappointments in the business is that target to shift stock-based compensation to cash compensation during 2024.

On the Q3 '23 earnings call , CFO David Schwarzbach made the following statement on SBC:

To reach our target, we are focusing our product development hiring efforts outside of the United States, particularly in the U.K. and Canada, as well as adjusting our overall mix of compensation throughout the organization. As a result, we plan to shift the substantial portion of our equity compensation to cash compensation in 2024. If we had made these compensation mix changes in 2023, SBC would have decreased by approximately $20 million, and cash expense would have increased by the same amount.

The shareholder hope was for a reduction in SBC by eliminating costs, not shifting the expense to cash. The adjustment in compensation expenses could slow the adjusted EBITDA growth rate during 2024, though the stock is still exceptionally cheap here.

Takeaway

The key investor takeaway is that investors should continue loading up on Yelp Inc. while it is trading at an exceptionally cheap valuation. Yelp has become far more productive in the last few years, and the additional ad formats and shifts towards services has allowed the business to report strong growth.

Investors should use any weakness to load up on Yelp.

For further details see:

Yelp Q3: Still No Respect