YELP - Yelp: Resilient Performance Should Continue

2023-09-29 00:09:59 ET

Summary

- Yelp serves as a valuable guide for consumers seeking reviews and information about local businesses, primarily in the United States.

- Yelp Inc. has demonstrated consistent resilience, and this trend is expected to continue, driven by its appealing value proposition to advertisers, resulting in revenue growth and margin expansion.

- While the expanding use of AI presents a challenge, Yelp's recent strong performance and innovative product offerings position it for growth.

Overview

My recommendation for Yelp Inc. ( YELP ) is a buy rating, as I expect the business to continue demonstrating resilient performance over the near term, supported by its value proposition towards advertisers. The incremental revenue should drive margin expansion, a trend that Yelp has demonstrated over the past few years. Together, these should drive multiple expansions.

Business

Yelp serves as an invaluable guide for those seeking a treasure trove of reviews and intricate details about the diverse array of businesses nestled in their local communities. Yelp primarily focuses on the United States, where 99% of its revenue originates from. In essence, Yelp is the compass that leads consumers through a vibrant tapestry of local businesses. With a rich tapestry of trusted information, captivating photos, and insightful reviews, they offer a comprehensive local ecosystem where individuals can effortlessly unearth, connect, and engage with businesses of all shapes and sizes. Be it soliciting a quote, securing a spot on a waitlist, reserving a table, booking an appointment, or making a purchase – Yelp simplifies the entire process, offering a seamless experience for the modern-day explorer of local gems.

Recent results & updates

Yelp delivered a solid set of results for 2Q23 that has turned my view of the business positive in the near term. On the results, Yelp revenue came in at $337 million, beating the top-end of its guidance ($320 to $330 million), and adj. EBITDA came in at $84 million, implying a margin of 24.9%. Importantly, the company is seeing healthy increases in advertising spending across all of its verticals, which is particularly encouraging given the current state of the market. Q2 revenue beat guidance, and total revenue guidance for FY23 was increased, thanks to positive spend per advertiser trends and a general uptick in advertising spending by small and medium-sized businesses.

At the rate that the business is performing, I am inclined to believe that it might continue at this pace, given the momentum. As I mentioned above, Yelp remains relatively resilient in the current volatile and uncertain ad environment, which is an indication that the ROI marketers are seeing continues to make sense . This means one of two things:

- Advertising on Yelp has such a high ROI that budgets continue to be allocated to it relative to other ad channels.

- Advertising on Yelp is much cheaper than other marketing channels but yields a similar ROI.

In either case, it's good news for Yelp because it bodes well for the company's ability to increase its market share. According to the Goldman Sachs Communacopia and Technology Conference , advertisers continue to place a high priority on spending on lower-funnel, click-based and performance ad offerings like those provided by Yelp. Yelp's diverse and affluent user base is a big draw for advertisers, and the site's high-intent users are another plus. Furthermore, I believe that advertisers are responding positively to Yelp's newer product offerings, such as (1) Yelp Audience and attribution solutions; (2) the redesigned home feed and increased personalization, which should continue to yield rising utility and engagement benefits over time.

Hence, I am turning bullish based on the recent performance. Looking beyond the current environment, I am positive about Yelp’s ability to continue to grow revenues and capture an increasing share of existing advertiser budgets, given its value proposition. Scale in revenue should also drive continued margin expansion, following the same trend over the past few years.

Author's valuation model

Valuation and risk

Author's valuation model

According to my model, Yelp is valued at $49, representing an 18% increase. This target price is based on my growth forecast of low teens over the next two years. The rationale for this growth rate is that I believe growth momentum will continue through the next year, as Yelp was able to show resilient performance even in today’s bad market environment. Suppose the macro environment recovers in FY24, Yelp should be able to grow at least at the same rate.

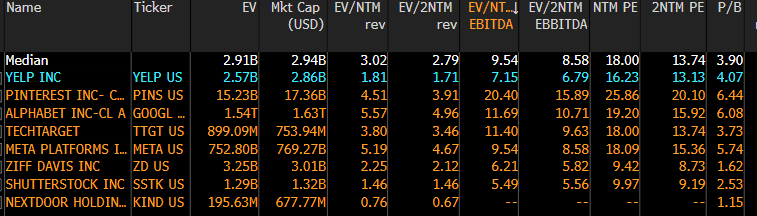

Yelp is now trading at 7x forward EBITDA, which I believe will gradually improve to 8x as it continues to show resilient performance. While Yelp is expected to grow at similar rates to peers (average of 10x), I note that its margin is less than peers (20+% EBITDA margin vs. peers at high 20s to low 30s%); hence, I attached a valuation discount.

{kind=link}

As for risk, I believe that the expanding applications of AI pose a threat to Yelp. While I do have optimism for the company as a whole, I do not feel super confident yet in YELP's ability to succeed in the increasingly complex and AI-driven advertising market. As more and more major companies put money into things like AI chatbots, conversational search experiences, and generative AI tools, I believe the danger level will rise. Google (GOOG) (GOOGL) and Bing (MSFT) have a strong foundation on which to build increasingly sophisticated tools for use in all stages of the advertising stack and marketing funnel (from measurement to targeting to conversion). My fear is that the larger platforms will be able to scale more quickly by investing in their larger data sets, distribution networks, and balance sheets to compete with YELP over the long term. For reference, Yelp has a total revenue of $1.3 billion over the LTM. This is less than 1% of Google’s ad revenue.

Summary

My recommendation for Yelp is a buy. Yelp has displayed remarkable resilience, and I anticipate this trend will persist in the near term, bolstered by its compelling value proposition to advertisers. With a strong track record of revenue growth and margin expansion, Yelp is poised for further multiple expansions. Yelp's ability to maintain its performance in a volatile advertising environment is a testament to its high ROI and affordability. The company's diverse user base and innovative product offerings position it for continued growth. However, the expanding influence of AI in advertising poses a potential threat. Despite this, I am optimistic about Yelp's growth prospects and value proposition. My valuation model indicates a target price of $49, representing an 18% increase, based on conservative growth forecasts.

For further details see:

Yelp: Resilient Performance Should Continue