YEXT - Yext: Hopes For A Rebound Are Fading

2024-01-13 13:13:04 ET

Summary

- Yext's lack of growth and customer defections are causing concern for investors.

- The company's valuation is low, but its prospects for M&A or turnaround are uncertain.

- Yext's Q3 earnings showed minimal revenue growth and a decline in key metrics like ARR and net retention rate.

Global markets are hanging on closely to the December Santa Claus rally. Bearish attempts to drag market indices lower this year so far have stalled. Amid this optimism for the direction of the markets in 2024, however, I continue to hold fast to the belief that 2024 will be a stock-pickers’ market. Including and especially in the tech sector, investors have to be diligent to identify companies with specific growth drivers and catalysts that can help to justify higher valuations this year.

In other words, I’m also favoring high quality stocks - and am not keen to invest in value names that later turn out to be value traps. Against this backdrop, I’m downgrading my viewpoint on Yext ( YEXT ), already down -15% over the past year (dramatically underperforming fellow software stocks over the same timeframe).

I last wrote a neutral opinion on Yext in October , at the time citing that its ultra-low valuation would offset its lack of clear growth execution. My thinking has changed now: as investors continue to chase stock-specific growth drivers, Yext’s lack of growth is going to stand out even more in 2024.

Yext has long been an AI and automation-driven company. Its original product, Yext Listings, sought to automate the process of local retail and restaurant businesses updating their opening hours across the web. Its subsequent products, Yext Answers and Yext Knowledge Graph, intended to leverage predictive AI to intelligently answer user queries on websites and get them to relevant pages more quickly.

Many software companies have seen a surge in bookings (or at least, pipeline interest) from GenAI use cases at the tail end of 2023, despite the overhang of tighter IT budgets. In spite of this big wave, Yext’s top line trajectory has barely moved from flattish y/y growth - indicating that the company is not a beneficiary at all of the AI trend, or that the industry doesn’t put much stock in Yext’s ability to execute and capture this market with its technology. Add that to the departure of Yext’s founder (Howard Lerman) and much of the company’s original executive team, and what we have left is a company that is struggling to hang on to relevance.

There are also signs of customer defections. Though revenue growth is barely positive, ARR is on a downtrend - as Yext is losing both direct-channel customers as well as customers gained from third-party resellers. And the company also continues to show <100% net revenue retention rates, indicating continued churn - while most of the software industry tends to report net retention rates above 100% (examples of Yext peers that report better retention rates include Zuora ( ZUO ), Okta ( OKTA ), Asana ( ASAN ), and many others).

For all these reasons, Yext is quite cheap. At current share prices just above $5, Yext trades at a market cap of $686.1 million. After we net off the $182.2 million of cash on Yext's most recent balance sheet, the company's resulting enterprise value is $503.9 million.

For next fiscal year FY25, meanwhile, Wall Street analysts are expecting Yext to generate $404.9 million in revenue, which represents flat y/y growth. This would put Yext's valuation multiple at just 1.2x EV/FY25 revenue.

I used to have a glimmer of hope that Yext might be an attractive M&A target, especially given its cheap valuation. But given customer defections, lack of growth, and seeming inability to benefit from recent AI tailwinds, I'm not sure this exit path is still reasonable for Yext to hope for.

All in all, I think Yext is dead money - it's best to ditch this stock and invest elsewhere.

Q3 download

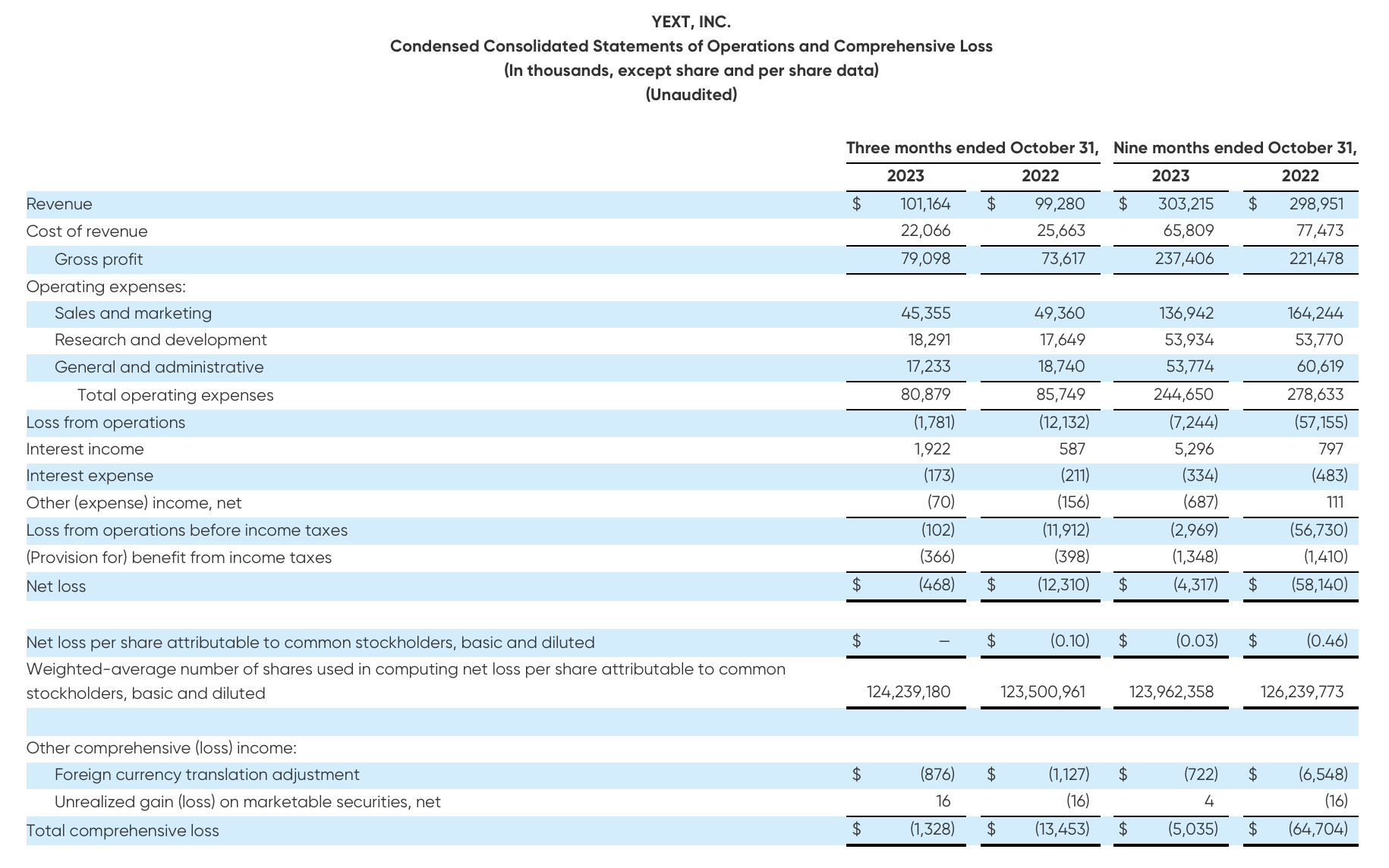

Yext's recent Q3 earnings print showcases a lot of the core issues that are plaguing the stock today. Take a look at the Q3 earnings summary below:

Yext Q3 results (Yext Q3 earnings release)

{kind=link}

Yext's revenue grew just 2% y/y to $101.2 million, missing Wall Street's expectations of $102.2 million (+3% y/y) and holding pace with the previous quarter's 2% y/y growth rate.

As previously mentioned, however, top-line growth did not preclude decay in other key metrics. Yext's ARR in the quarter shed roughly $1 million sequentially to $396.8 million. For a subscription software company whose bread and butter business model involves investing heavily in upfront sales to secure customers for long-term subscription contracts, the slide in ARR - also the fourth sequential quarter of ARR decay - is a major blow.

Yext ARR (Yext Q3 earnings release)

{kind=link}

Similarly, dollar-based net retention rate in the quarter was 96%, one point worse than in Q2 - driven by more churn among direct-channel customers, though third-party reseller customers also showed <100% retention rates.

Yext retention trends (Yext Q3 earnings release)

{kind=link}

The company is hopeful that it can return to ARR growth next year, but so far, it is expecting the situation to worsen in Q4 before getting better. Per CEO Mike Walrath's remarks on the Q3 earnings call :

As we continue to improve our operations, we were hopeful this year would be a year of reacceleration for Yext, but we aren’t seeing this in our revenue or ARR growth rates yet. As we discussed on our Q2 call, the selling environment remains quite challenging with some deals slipping or downsizing during the later stages of deal cycles. This caused softness in Q3 bookings as well as budget pressures on renewals. On top of this, we expect a singular large churn in Q4 attributable to a particular customer. We believe this is due to unusual factors that are unique to this customer. Darryl will discuss churn in more detail, but this particular account, a happy customer, seems to be facing budgetary pressures of the magnitude we are not seeing with other accounts.

The net result is that fiscal year ‘24 revenues and ARR will not see the reacceleration we anticipated when we began the fiscal year. We think this is temporary because we see real improvement in underlying trends around pipeline, sales productivity and profitability, and we remain confident that we’ll see a return to high single-digit ARR growth next year."

In other words - it's not a great time to invest in Yext.

Key takeaways

With flailing customer momentum, macro-related budget headwinds, and Yext constantly being outshadowed by flashier and more relevant AI-driven software names, I fear that Yext's time in the penalty box will have no definite end.

The only "upside risks" I see, as previously mentioned, is the possibility of M&A. With such a low valuation, Yext could be viewed as a technology grab - though with the exit of its product-driven founder, plus customer churn, I think this is unlikely. Better than expected execution is also possible - if the deals that Yext cited were delayed have remained in the pipeline and will close in FY24, we could see the reaccelerating in ARR that the company is hoping for.

Still, I see far more risk than reward/upside potential in this stock. Steer clear here.

For further details see:

Yext: Hopes For A Rebound Are Fading