YEXT - Yext: Profits Without Growth

2023-12-11 03:44:25 ET

Summary

- Yext should benefit from the digital transformation of business and the AI revolution.

- The company's growth has slowed due to a tough macro environment and budgetary pressures from customers.

- Management is optimistic growth will return and has increased sales productivity and profitability, but they will have to overcome the loss of a large customer from Q1 onwards.

Yext, Inc. ( YEXT ) takes care of customer's proliferating digital presence by producing consistent messaging through a host of different digital platforms and a host of additional products, like Answers that help customers with the search on company websites using natural language, rather than links (like large language models).

{kind=link}

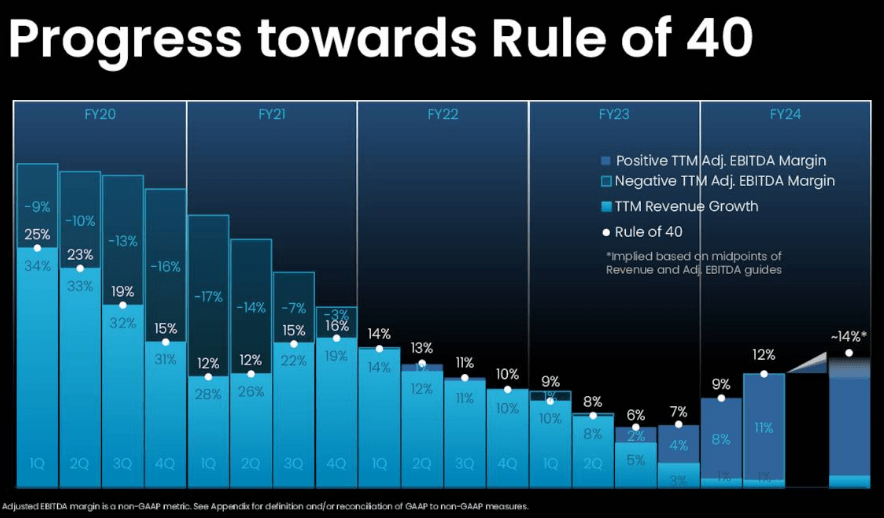

The company moved from a loss-making but relatively fast-growing company to produce a profit but with growth almost coming to a halt, the following figure from the earnings deck sums that up:

{kind=link}

In principle, the company remains well-placed to benefit from the secular tailwinds:

- The digital transformation of business

- The AI/LLM revolution

ARR growth

The growth slowdown comes from the fact that the macro environment turned out to be a little tougher than they expected at the start of the year with many customers feeling budgetary pressures.

This produces a situation that while the pipeline is still promising, once they negotiate deals the size of the deal tends to be affected in the latter stages of negotiation once finance gets involved ( Q3CC ):

what you get is, you get this picture of really robust pipeline that actually on a dollar basis closes at a lower percentage than we have seen historically.

The same budgetary issues play during renewal negotiations.

The rough environment for SMBs, which come in disproportionally through resellers that started 6 quarters ago is stabilizing and management is getting a little more optimistic here.

Most of the reseller ARR 7% decline in Q2 was caused by the merger of two resellers, without that there would have been a small sequential ARR increase.

Management sees opportunities with their resellers as they are focused on SMBs but don't always follow through with deals that are closed so management sees an opportunity to increase ARR here.

There were some new logo wins and some 'boomerang' customers coming back

However, there is a loss of a large customer on December 31, 2023, which will have an $11M hit to ARR from Q1/24 onwards .

Competition

ARR growth slowed down on macro uncertainties which not only reduced growth directly, but more customers scrutinizing expenses led to more choosing for a lower cost alternative.

Management claims they have some success with 'boomerang' customers (like Guaranty Bank & Trust in Q2), that is, customers that went away (presumably to the competition) but are coming back ( Q2CC ):

we saw some of these listings and reviews customers go elsewhere over the last two, three, four years. We've talked about this a lot. They were promised certain things by competitors and in a lot of cases, they moved for lower-cost solutions. And I think what they found was that the ones that are coming back clearly didn't get the value that they were expecting elsewhere, and so we're seeing them return.

Apparently, the competition leaves much to be desired (Q2CC):

What you see over the last few years is some of our competition doing some unnatural things from a deal structure standpoint and the old adage is you get what you pay for. And so listings quality, the support models, the ability to resolve issues at scale are really all areas where competition has fallen down really. And when you're talking about mission-critical data being out there in the Internet, you're talking about your public presence and sort of driving top of the funnel, you really can't go with a second-rate solution.

There were several more 'boomerang' customer wins in Q3 (Q3CC):

One client in particular, was an immediate win back from Q2 when they signed with a competitor and almost immediately ran into issues as the competitor failed to deliver on their deadlines.

they did have a few customers coming back from the competition, like Guaranty Bank & Trust in Q2.

New product version

The company finished its platform improvement with the autumn release with 80 new features so they continue to improve and add functionality.

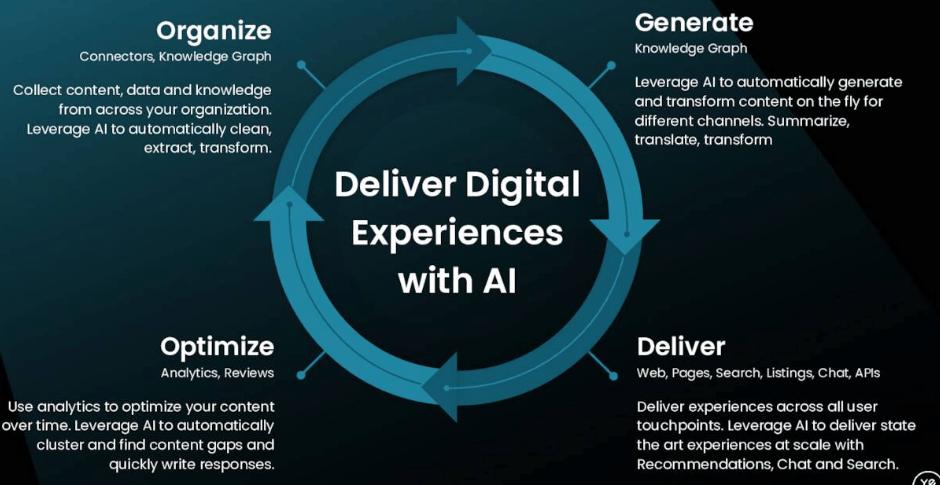

AI

{kind=link}

While the company introduced a new AI functionality able to produce AI-generated responses to reviews, management underscores that larger companies especially facing hurdles employing AI in customer-facing applications as a result of regulatory and legal constraints. Therefore, management stresses (Q2CC):

our digital experience solutions are not purely AI solutions. They're really robust digital experience capabilities, including now content, headless CMS and a number of others that brings tremendous value without the AI plug-in pieces

Management believes that the real AI ramp is 4-8 quarters away as the teething problems are sorted out and the risks decline for large organizations but actually sees faster AI adoption at SMBs.

One might worry whether the large language models could become a competitive threat for Yext, but they had some reassuring things to say on this at the Q3CC:

I think there is a lot more reticence, especially from larger enterprises and regulated industries about kind of setting the AI free in talking to the customer directly. And so we have, we believe, huge advantages over the long run because of the nature of our content system and our knowledge graph storing authoritative information, which makes the - allowing the generative AI to generate the customer experience... we are starting to see generative AI application interest translate into purchases

That seems a reasonable take albeit we still have some residual worries about LLMs getting better and might be able to produce similar results without Yext knowledge graph.

Cost cutting/efficiency gains

We already pointed out above that while revenue and ARR growth are almost stagnating, margins have improved to such an extent as to produce non-GAAP black figures.

- Management revamped their go-to-market approach, increasing sales productivity, leading to a 9% y/y decline in S&M in Q2 and a 7% decline in Q3, falling to 42% of revenue, down from 48% in Q2/22.

- This involves things like focusing on value-based selling, rep performance, and qualified pipeline generation.

- Net income was $8.1M versus a loss of $3.9M in Q2/22.

- Sales productivity is proving as demonstrated by leading indicators like bookings per sales rep and the pipeline is improving.

A little more depressing is that it's likely diminishing returns have been reached with the cost-cutting and revamping of sales strategies, as management itself argued that they are looking for a balance with growth strategies and are aware that there is a potential trade-off here.

Finances

Some notable Q3 figures:

- $500K+ forex headwind, without which they would have made guidance.

- ARR was $396.8 million at the end of Q3, up 2% y/y.

- Net retention 97% (95% for customers coming through resellers)

- FY23 gross margin +350bp to 78.9%.

- OpEx was $69.9M or 69% of revenue compared to $72.1M or 73% on S&M realignment.

- S&M was down 7% while R&D was up 13% in Q3 (y/y).

- Adjusted EBITDA was $13.5M versus $7.1M in Q3/22.

- Net income was $11.3M compared to net income of $2.5M in Q3/22

- Operational cash use was $1.6M versus $10.8M in Q3/22.

- Cash and cash equivalents were $182M, down from $201M at the end of Q2/23. An $11.9M share buyback in Q3 explains most of the cash decline.

- Stock-based compensation declined to 12% of revenue.

The big takeaway is that adjusted EBITDA is expected to be over $51M for the full year, a pretty impressive increase of over 200% in FY22. The company really is getting more profitable and over 100% of adjusted EBITDA now flows into operational cash flow.

Cash flow has improved a lot too. Net cash used in operating activities was $1.6M versus $10.8M in Q3/22 (Q3 isn't yet in the figures):

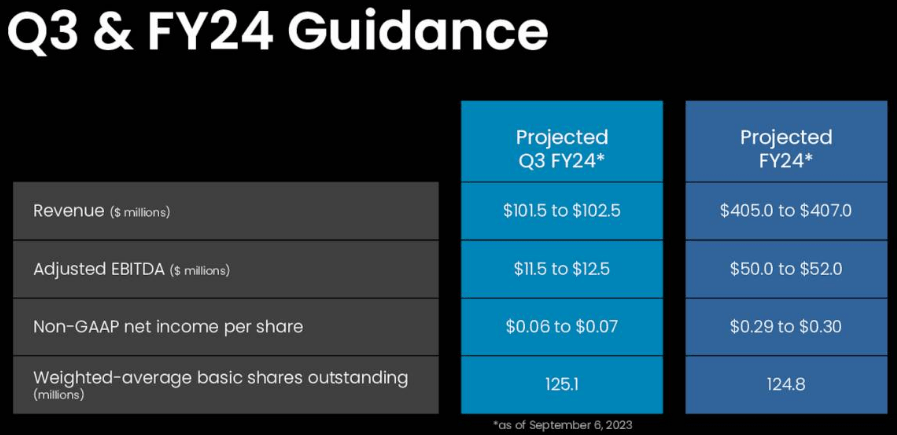

Guidance

The guidance they provided at the Q2CC:

{kind=link}

There were slight tweaks to the outlook after Q3:

- Revenue $403.2M to $403.7M

- Adjusted EBITDA $51.7M to $52.7M

- Non-GAAP net income per share is projected to be in the range of $0.31 to $0.32, on 124.1M weighted-average basic shares outstanding.

Management is somewhat optimistic that growth can return (Q3CC):

We don't expect those headwinds to continue in a meaningful way next year. And so as we see our execution improve on things like sales productivity, pipeline and efficiency, we feel confident that those things will allow us to grow next year with some of these, let's call it, chosen headwinds this year... we see real improvement in underlying trends around pipeline, sales productivity and profitability, and we remain confident that we'll see a return to high single-digit ARR growth next year.

In any case, they are somewhat adaptable in their focus depending on the environment and can focus on efficiency like they have done this year if the environment turns out to be tougher than expected.

But there is that $11M ARR hit from the big customer leaving on Jan 1.

Valuation

On November 21, 2023, this had declined to 124M on buybacks.

Add to that the 2.4M stock options and 10.45M RSUs outstanding and you get a fully diluted share count of 136.85M. At $6 produces a market cap of $821.1M and an EV of $639M.

With FY23 revenue guided at $403.5M this delivers a reasonable 1.58x EV/S for a company that's not growing, even a little on the cheap given the 78% gross margin and the possibility of at least some modicum of growth returning.

The earnings multiple (a P/E of 22x) is still fairly robust. It seems to us that the low-hanging fruit for cost-cutting has largely been picked so the company mostly needs a growth revival to produce some operating leverage.

Conclusion

The company has some attractive features:

- A sophisticated AI-based platform for which there is considerable need with the proliferation of digital attack space to cover. It's constantly improving its platform as well and looks to be the market leader.

- Sales productivity seems to have increased.

- Despite decelerating growth, margins have improved considerably and the company has swung to profit and generates considerable amounts of cash.

However, we find the evaporation of ARR growth quite concerning, a net retention rate under 100% also suggests quite a bit of attrition.

If revenue growth returns to high-single digits as management seems to be predicting for next year, the shares are attractive, as cost-cutting has significantly increased the operating leverage in the model.

Not only would that boost the bottom line disproportionally, but it would also increase cash flow with which to buy back shares.

A return to higher growth looks well within the realm of possibility, although the chances for it near term seem bleak with the loss of an $11M ARR customer per Q1 next year.

The upshot : Despite the considerable fall in the share price post Q3 earnings we see more attractive opportunities elsewhere.

For further details see:

Yext: Profits Without Growth