YEXT - Yext: Some Encouraging Metrics But No Growth Still A Big Red Flag

2023-10-01 03:42:47 ET

Summary

- Investors have abandoned tech stocks for safer investments, causing a decline in small and mid-cap tech stocks like Yext.

- Yext has improved its gross margin, generating better adjusted EBITDA and cash flow, and has added $50 million to its buyback program.

- However, Yext's growth has stalled, it has high churn rates, and the departure of its CEO and CFO raises concerns about the company's direction.

Investors have largely abandoned tech from their portfolios, preferring to stick to the safety of ultra-high risk-free cash yields. The sharp portfolio rotation has hurt small and mid-cap tech stocks the most, those whose values are based almost entirely on product and future earnings.

Against this backdrop, shares of Yext ( YEXT ) have given up all of their YTD gains (at one point having doubled from the start of the year over excitement on AI innovation). But unlike many other tech stocks, this sharp drop in share value has also been accompanied by a veritable decline in the business, as Yext's top line has cranked out barely any growth over the past few years.

Earlier this year, I wrote a note downgrading Yext to bearish on the basis of its terrible growth rates and its seeming lack of direction. Since then, a number of positive developments have swept in:

- Yext has substantially improved its gross margin profile, a result of the company simplifying its services organization and slimming down its cost structure

- As a result, the company has been able to generate substantially improved adjusted EBITDA and cash flow, removing a core concern for small-cap tech stocks in the current recession

- The company is taking advantage of its lower share prices by adding $50 million to its existing buyback authorization, which at current share prices would cover just over 6% of the company's outstanding market cap

It's worth noting as well that Yext has ~$200 million of cash and no debt on its books, so it can well afford this increased buyback program - especially with its positive adjusted EBITDA/OCF profile.

In light of the slightly improved outlook to Yext's bottom-line results, I'm upgrading my view on the company to neutral. That being said, I'm still very wary of the following red flags:

- Growth has stalled. Yext is barely managing to eke out growth anymore, and in the tech space, lack of growth creates a vicious cycle where customers start to lose faith and churn (software requires support, ongoing maintenance, and feature updates - none of which companies want to invest in if they think the vendor is in trouble of sinking).

- High churn rates. Yext's focus on smaller and mid-market customers has led to high churn rates (holding down growth). Yext's net revenue retention rates index far lower than peer software companies.

- Founder exit. Howard Lerman's resignation as CEO in 2022, as well as the concurrent exit of longtime CFO Steve Cakebread (a former Salesforce executive and well-known in the tech community), indicate in my opinion a lack of faith in the direction of the business.

The bottom line here: while I no longer necessarily think Yext is going to pink-sheet territory anytime soon thanks to its improved bottom-line profile, a software company that isn't growing, to me, is barely investable. Stay on the sidelines here until Yext can show a path to recovering its top-line trends.

Q2 download

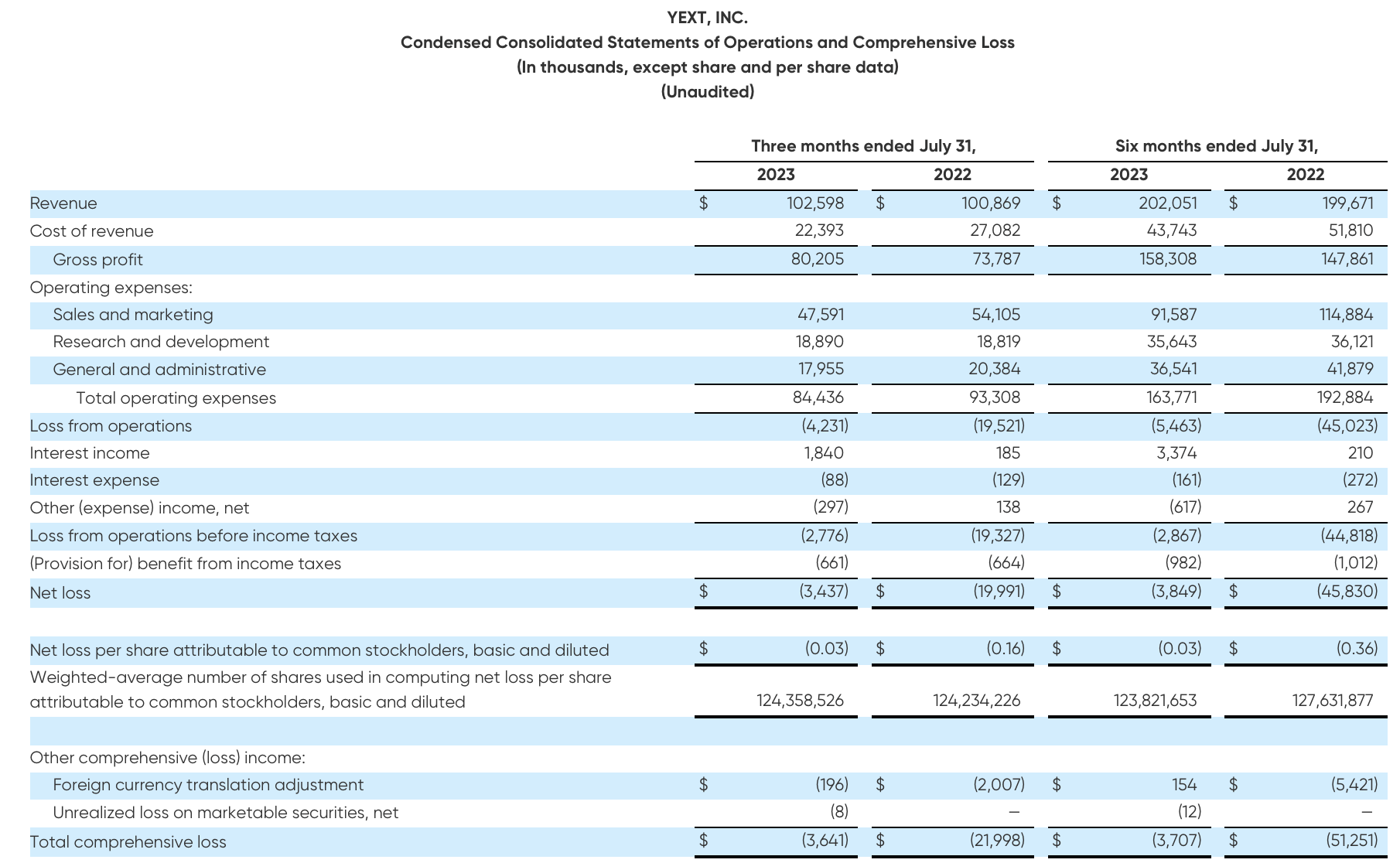

Let's now go through Yext's latest quarterly results in greater detail. The Q2 earnings summary is shown below:

{kind=link}

Yext's revenue grew only 2% y/y to $102.6 million in Q2, though this came in slightly ahead of Wall Street's $102.0 million (+1% y/y) expectations for the quarter. Growth largely held pace with Q1's 1% y/y growth rate

Management notes that while its sales team's execution is improving, buying trends still remain challenged in the enterprise space - which is similar commentary to what other software companies are reporting. Per CEO Michael Walrath's remarks on the Q2 earnings call:

In Q2, total ARR grew 3% year-over-year and direct ARR was up 5%. Sales productivity and execution are continuing to show improvement and I'm pleased with the progress we're making in our end-to-end demand generation efforts. Our go-to-market transformation remains a work in progress where we are executing well and beginning to see increases in total and qualified pipeline production.

Our midmarket team who calls on smaller enterprise customers continues to execute well consistent with the progress we saw from this group in Q1. We continue to believe this momentum will eventually carry over to larger enterprises so it is likely to take longer in the current macro environment. Customer buying trends, budget scrutiny and prolonged closed processes with multiple decision makers are still the norm and the larger the enterprise, the more of these factors repeat the sales cycle.

Interest in our digital experiences solution is building. We see measurable increases in total pipeline year-over-year. However, we have not yet seen buying trends from larger enterprise customers re-accelerating. Our assumption is that enterprise deal cycles, budget pressures and close rates will remain challenged through the rest of the year."

Yext remains in a net churn position, which is rare among enterprise SaaS companies. The good news, however, is that churn is improving slightly. Dollar-based net retention rates ticked up slightly to 97% this quarter (indicating 3% net churn), versus ~96% over the past two quarters in 94% in Q3 of last year:

{kind=link}

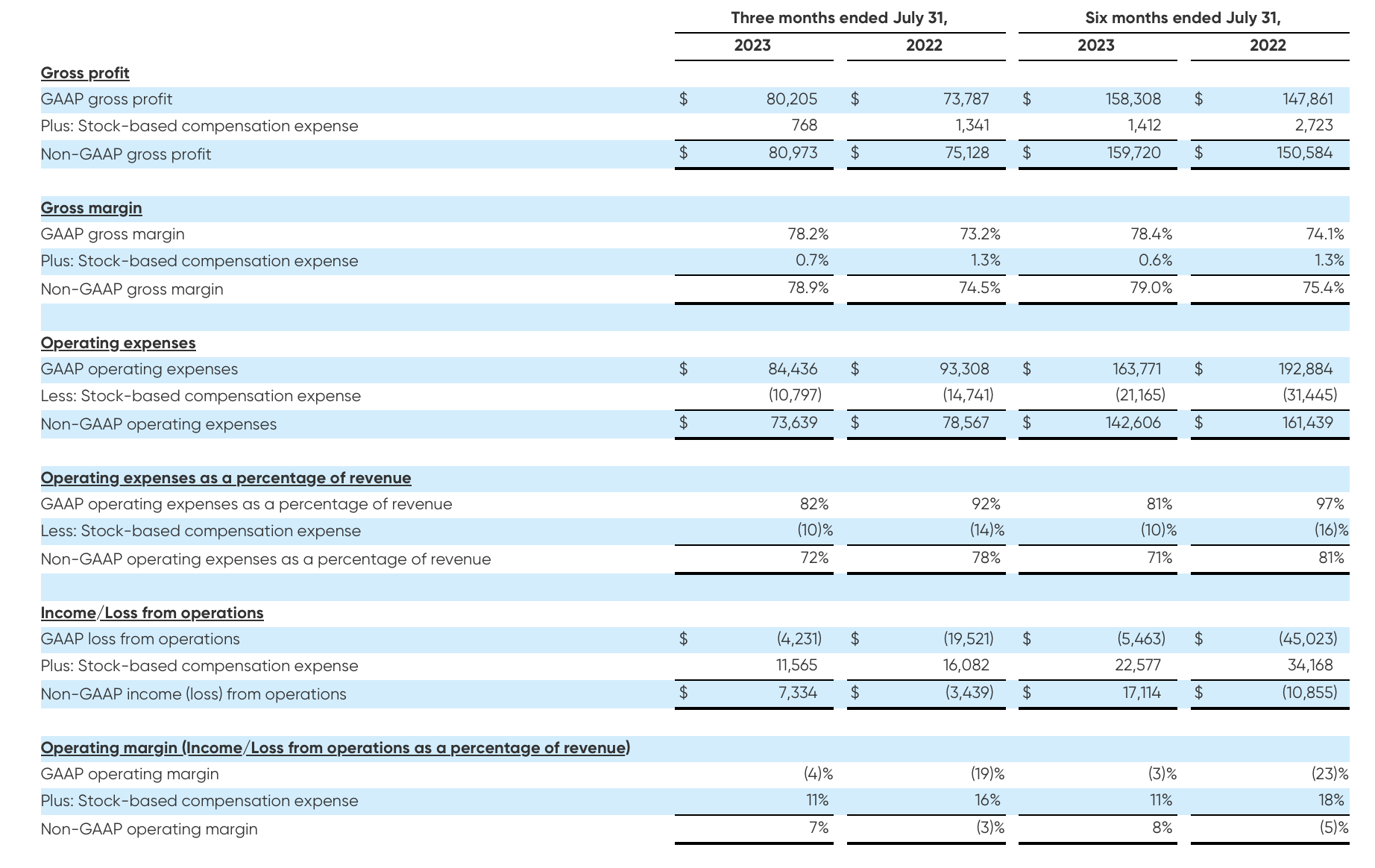

Margins, meanwhile, are where Yext excelled in Q2. The company's pro forma gross margins lifted 530bps y/y to 78.9%, a result of the company improving costs in its services organization.

{kind=link}

The company also managed to slim down total opex to 72% of revenue, a six-point improvement versus the year-ago Q2. As a result, pro forma operating margins swung to a positive 7% this quarter, up from -3% last year.

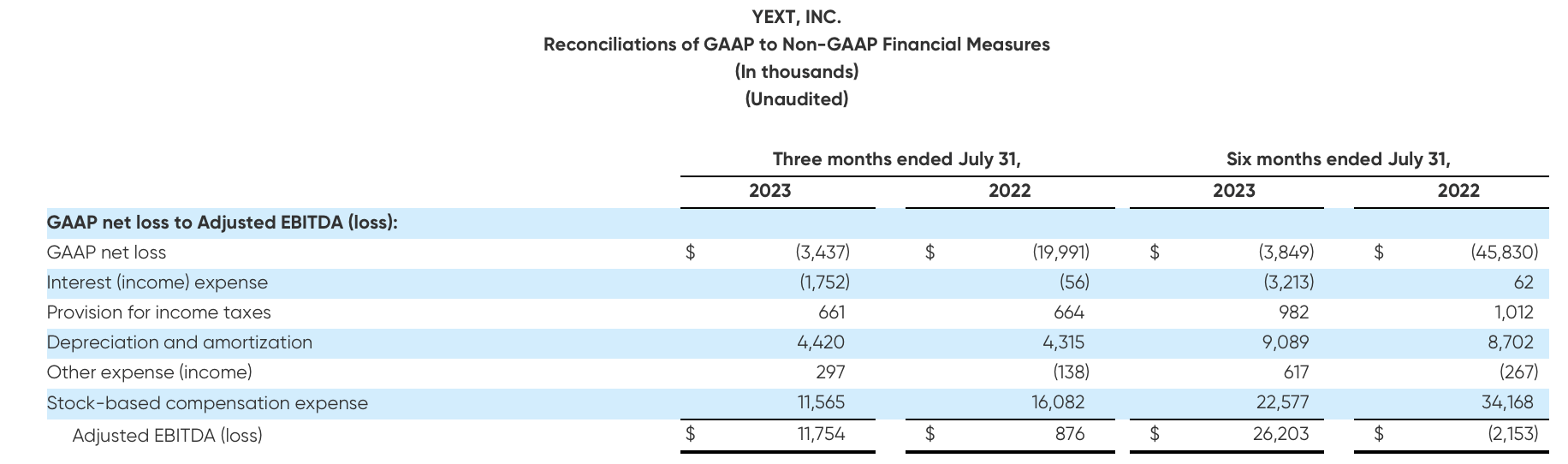

Adjusted EBITDA also improved dramatically to $11.8 million, or a 12% margin, versus just a 1% margin in the year-ago quarter.

{kind=link}

Yext also generated $19.7 million of operating cash flow in the first two quarters of FY23, versus cash burn of -$7.3 million in the prior-year period: a reflection of the company's higher gross margins and opex cost reductions that give us more comfort in Yext navigating through the current macro environment.

Valuation and key takeaways

At current share prices just over $6, Yext trades at a market cap of $788.0 million. After we net off the $200.5 million of cash on Yext's most recent balance sheet, the company's resulting enterprise value is $587.5 million.

Meanwhile, for next fiscal year FY24, Wall Street analysts are expecting Yext to execute a slightly improved return to growth, with revenue up 5% y/y to $425.6 million (data from Yahoo Finance ). Against this outlook, Yext trades at just 1.4x EV/FY24 revenue. And if we assume Yext's current ~12% adjusted EBITDA margin profile on FY24 revenue, adjusted EBITDA would be $51.1 million and its multiple would be 11.5x EV/FY24 adjusted EBITDA.

Needless to say, Yext is cheap: but with such tepid growth rates, it's difficult to tell whether Yext is capable of rebounding or if it will die a "death by a thousand cuts" as it decays toward irrelevance. All in all, I'm not comfortable making a bet on this stock yet: I'd recommend remaining on the sidelines here.

For further details see:

Yext: Some Encouraging Metrics, But No Growth Still A Big Red Flag