YEXT - Yext Valuation In Question As Growth Prospects Diminish (Rating Downgrade)

2023-10-12 12:04:08 ET

Summary

- Yext, Inc. is a technology platform facilitating accurate consumer queries responses across digital platforms.

- Uncertainty shrouds Yext's prospects as it trades at a high multiple of 21 times this year's EPS.

- Yext holds strengths such as being debt-free and its AI-enhanced digital experiences.

Investment Thesis

Yext, Inc. ( YEXT ) is a technology platform that aids businesses in organizing and managing their factual information, allowing them to offer accurate and prompt answers to consumer queries across various digital platforms, thereby enhancing their online presence and improving customer engagement.

Getting right to the point, this stock is currently priced at 21x this year's EPS, a multiple that might be too high for a business that could end up delivering no top line growth next year. This means that without top line growth, there's only so far Yext can cut back costs before its EPS also stops growing.

Yes, the business is debt-free, and that's clearly a bullish consideration, but I no longer believe that's enough to justify paying 21 times EPS. Therefore, I turn neutral on this stock.

Quick Recap,

In my previous analysis, I said :

Recall, that Yext is a debt-free business, with more than 20% of its market cap being made up of cash. The main bearish thesis here is that Yext is struggling to reaccelerate its revenue growth rates. Meaning that, unless Yext can start to deliver some strong top line growth, investors will continue to sidestep this stock.

For my part, I still remain hopeful that Yext has what it takes to reignite its operations and start delivering some top line growth.

With the benefit of hindsight, it's now easy to see that Yext has no growth left in the tank.

Nonetheless, that didn't stop me from making a terrible call on this stock. I had believed that investors' expectations were already low enough as we headed into the fiscal Q2 2024 earnings results, but as it turned out, investors' expectations were still high. Accordingly, I believe it's prudent for me to turn neutral on this stock until there's concrete evidence that it can regain some stable growth.

Yext's Near-Term Prospects

Yext, Inc. is a technology company that provides a platform for organizing a business's factual information, referred to as the Knowledge Graph. This platform enables businesses to structure and manage data about their brands, such as location details, professional information, FAQs, and more.

Yext's primary goal is to empower businesses to offer accurate and direct answers to consumer queries on their websites and across various digital platforms, including search engines, GPS systems, digital assistants, and social networks.

By centralizing and controlling this information, Yext helps businesses improve their online presence, enhance consumer engagement, and ensure that consumers receive accurate and relevant information about the business, ultimately driving customer conversion and retention.

In the near term, Yext's prospects remain promising as they continue to focus on product innovation and sales strategies. The company has gained traction with its digital experience platform featuring AI capabilities, attracting businesses looking to enhance their online presence.

Here's a quote from Yext's earnings call echoing that insight:

Executives are interested in finding AI-enabled solutions to enhance their digital experiences, yet many businesses lack the highly specialized technical expertise to realize its transformational power.

Moving on, Yext's summer release introduced AI enhancements for chat, content, and reviews, further appealing to a market interested in AI-driven solutions.

Moreover, Yext's commitment to optimizing the sales organization and its ability to generate cash flow while delivering value to shareholders highlights its strength in managing growth efficiently (more on its cash flows soon).

However, Yext does face notable challenges. The current macroeconomic environment presents obstacles with budget scrutiny, prolonged sales cycles, and increased decision-making complexity among larger enterprises. The delayed acceleration of buying trends from enterprise customers, cost-cutting efforts, and challenges in renewals create hurdles for ARR growth.

Additionally, the reseller channel, while showing potential, experienced a drop in ARR due to a customer churn from an M&A event. The company acknowledges the need to address these challenges and is cautious about the environment in the back half of the year, reflecting the continued uncertainties in the market.

In light of this framework, let's explore Yext's financials.

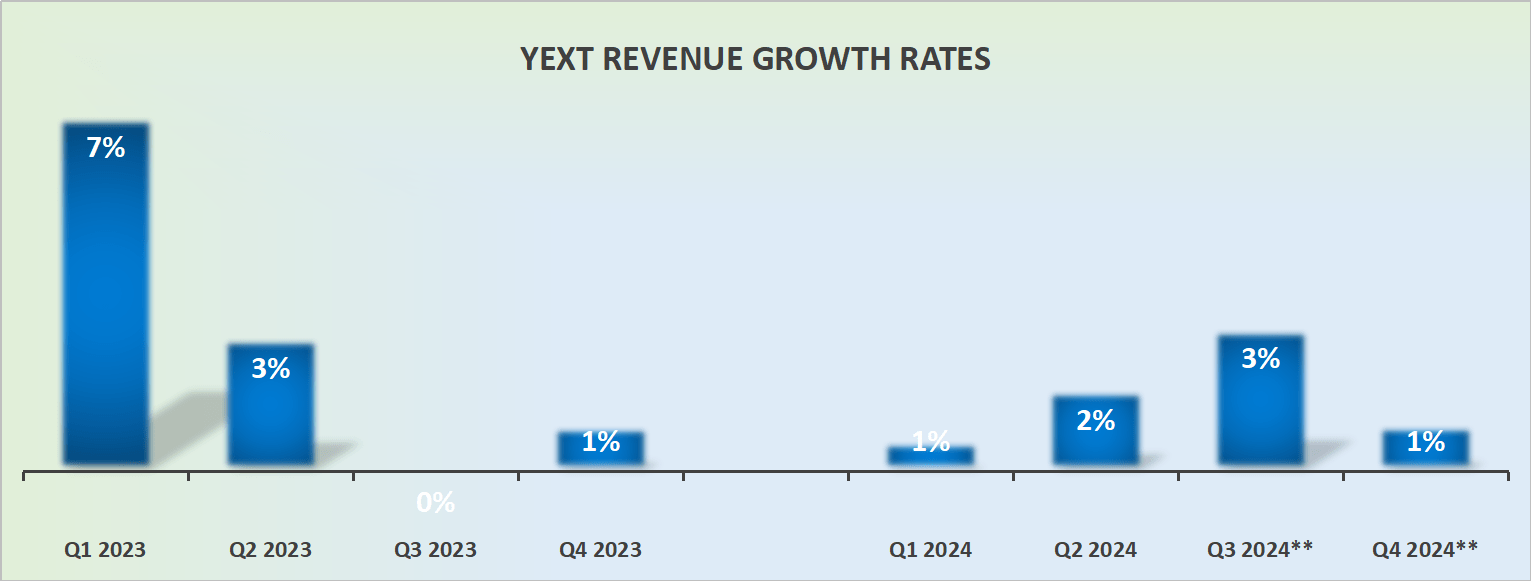

Revenue Growth Rates Fully Moderate

{kind=link}

Previously, I believed that Yext would be able to revise its fiscal H2 2024 results upward. After all, in fiscal Q1 2024 , Yext had delivered 1% growth against a much higher hurdle of 7% growth in the previous year.

It didn't make sense for fiscal Q3 2024 to be guided for only 3% y/y growth, given the comparables from the previous year set a low bar.

And yet, here we are. However, we analyze this business, it's clear that its revenue growth rates are expected to moderate. Furthermore, there's a real danger that in fiscal 2025, this technology company may end up delivering no growth or worse, negative growth rates.

Keeping this perspective in view, let's discuss its valuation.

YEXT Stock Valuation - A Complex Picture

This is where the plot thickens. It's not just that Yext's price-to-sales multiple dropped from 4x forward sales to 2x forward sales in about two months. But also, looking back a few years ago, this stock was priced at close to 6x forward sales.

That being said, the issue here has been a misalignment of investors' expectations. Investors believed that Yext still had some growth potential left. And without that growth, investors are likely to shift their focus from revenue growth rates to underlying free cash flows and the multiples they are willing to pay.

Particularly considering the real danger that next year, Yext may be delivering negative y/y revenue growth rates.

To put it more concretely, is it truly worthwhile to pay 20 times this year's EPS for a business that may end up delivering negative revenue growth rates next year? What about the year after? Is there a scenario where this technology becomes even more obsolete?

The Bottom Line

As I consider Yext's current situation and prospects, I find myself in a state of uncertainty. Yext is a technology platform aimed at aiding businesses in managing their information and enhancing their digital presence.

However, the stock is currently priced at 21x this year's EPS, a valuation that raises concerns, especially as the company faces challenges in reigniting its revenue growth.

While Yext, Inc. has strengths, such as being debt free and introducing AI capabilities to improve digital experiences, I can't help but question whether its growth potential is running dry.

The evolving market dynamics, budget scrutiny, and competitive hurdles add to my uncertainty about the company's future. The misalignment of investor expectations and the possibility of negative growth rates in the coming years make Yext's valuation a perplexing puzzle.

For further details see:

Yext Valuation In Question As Growth Prospects Diminish (Rating Downgrade)