CA - Yum Brands Vs. Restaurant Brands International: Which Is The Better Buy?

2023-06-07 20:49:50 ET

Summary

- Restaurant Brands International and Yum Brands are both fast food operators with multiple brands across global markets.

- They have comparable sizes, revenues, EBITDA margins, and growth.

- Today, we'll aim to determine which of the two companies actually deserves a spot in your portfolio.

At first glance, Restaurant Brands International ( QSR ) and Yum Brands ( YUM ) look like very similar companies. They are both fast food operators, running multiple restaurant concepts across many global markets. They are also comparably sized, with similar revenues, free cash flows, EBITDA margins, and more.

Today, we will attempt to answer the following question: Which one of these fast-food giants deserves a spot in your portfolio, and which belongs in the dumpster out back?

Overview

When it comes to fast food, consumers have lots of choices and the market is quite competitive. QSR and YUM control the following brands:

| QSR |

| YUM |

| Burger King |

| KFC |

| Tim Hortons |

| Taco Bell |

| Popeyes |

| Pizza Hut |

| Fire House Subs |

| The Habit Burger Grill |

Both companies operate a franchise model, where almost 100% of the underlying restaurants are owned and operated by independent third-party franchisees.

Here's a breakdown of system-wide metrics for each company from their most recent reported quarter:

QSR |

| Restaurant Concept |

| Store Units |

| Store Units Growth YoY |

| System Revenues |

| Same Store Sales Growth YoY |

| Burger King |

| 18,911 |

| 2.5% |

| $6.24 B |

| 10.8% |

| Tim Hortons |

| 5,620 |

| 5.6% |

| $1.73 B |

| 13.8% |

| Popeyes |

| 4,178 |

| 10.8% |

| $1.56 B |

| 5.6% |

| Fire House Subs |

| 1,247 |

| 2.3% |

| $292 M |

| 6.1% |

| Consolidated |

| 29,956 |

| 4.2% |

| $9.8 B |

| 10.3% |

YUM |

| Restaurant Concept |

| Store Units |

| Store Units Growth YoY |

| System Revenues |

| Same Store Sales Growth YoY |

| KFC |

| 28,003 |

| 2% |

| $8.05 B |

| 9% |

| Taco Bell |

| 8,276 |

| 6% |

| $3.46 B |

| 8% |

| Pizza Hut |

| 19,046 |

| 3% |

| $3.36 B |

| 7% |

| The Habit BG |

| 358 |

| 8% |

| $158 M |

| 0% |

| Consolidated |

| 55,683 |

| 3% |

| $15 B |

| 8% |

In order to earn revenues from these franchisee ecosystems, QSR and YUM drive sales from royalty fees, supply chain inventory, property rents, and other services they provide to restaurant owners.

In return, franchisees can tap into the existing brand equity, marketing strategy, and the respective customer bases of each restaurant concept.

Operating Plans

As you can see from the numbers above, QSR and YUM have taken different approaches to running their businesses.

YUM, with more than 55,000 restaurants, seems to have taken the "shotgun" approach, opening as many restaurants as possible.

This strategy has worked well to increase system revenues, but broadly the risk here is that overall growth may mask issues at an individual store level. Brands may begin to suffer which could lead to underperforming assets, or specific markets may become saturated with locations and begin to cannibalize one another.

Thankfully, the company has seen solid same store sales growth of 8% YoY, which indicates that restaurants have some pricing power, and that each store, on average, continues to sell more than ever before.

QSR, on the other hand, has taken a more measured approach. The company boasts just shy of 30,000 restaurants, and less than $10 billion in quarterly system sales (vs. $15 billion for Yum). While the footprint is smaller, same store sales growth, especially with Burger King and Tim Hortons, has been much stronger.

It may come as a surprise, then, that each company has seen somewhat similar financial results recently.

Recent Results

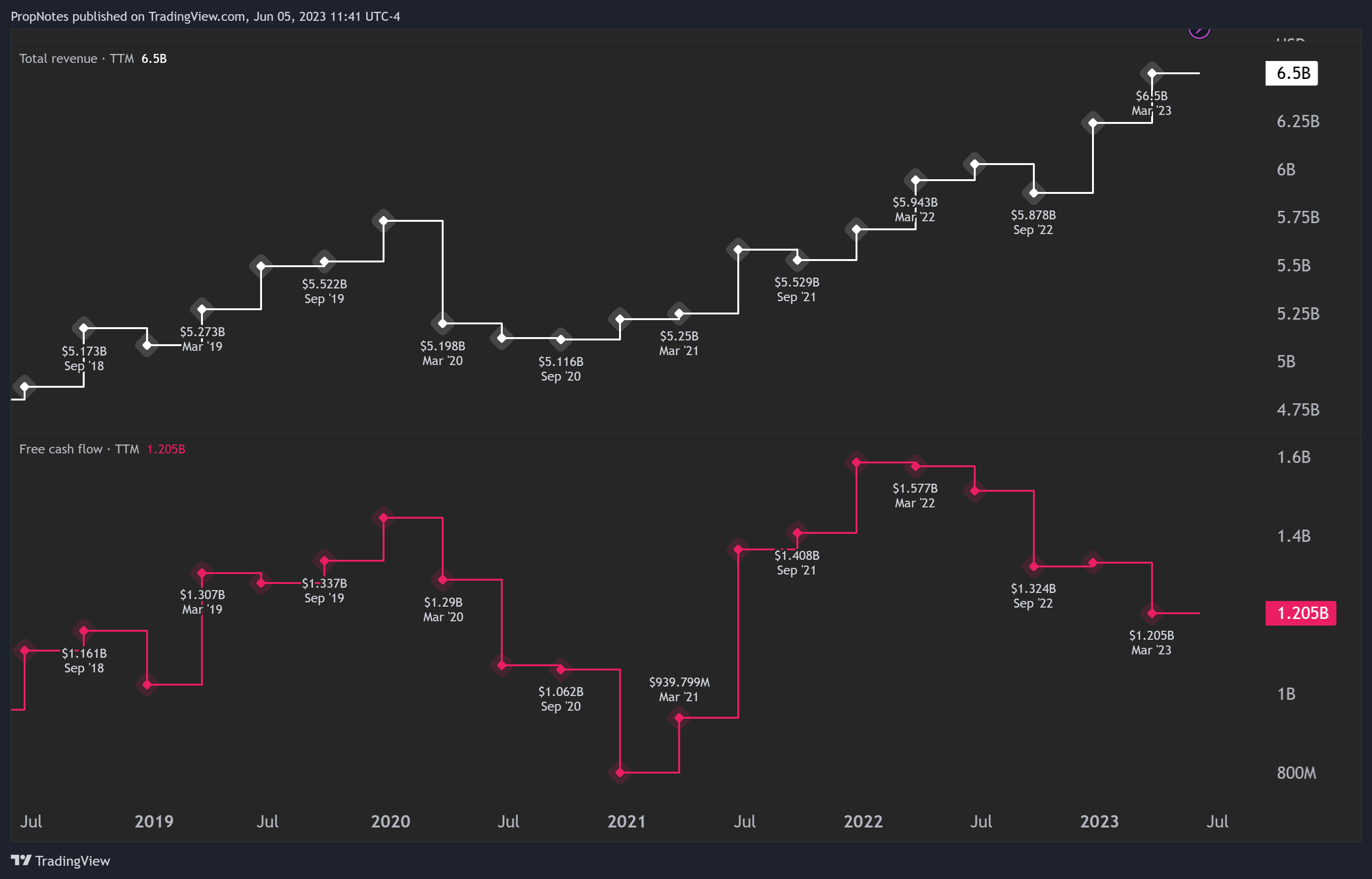

Over the last twelve months, QSR reported $6.5 billion in sales and $1.2 billion in free cash flow. Remember - this is different from "System Revenue"; each company earns revenue and cash flow from franchising as opposed to selling you food directly:

{kind=link}

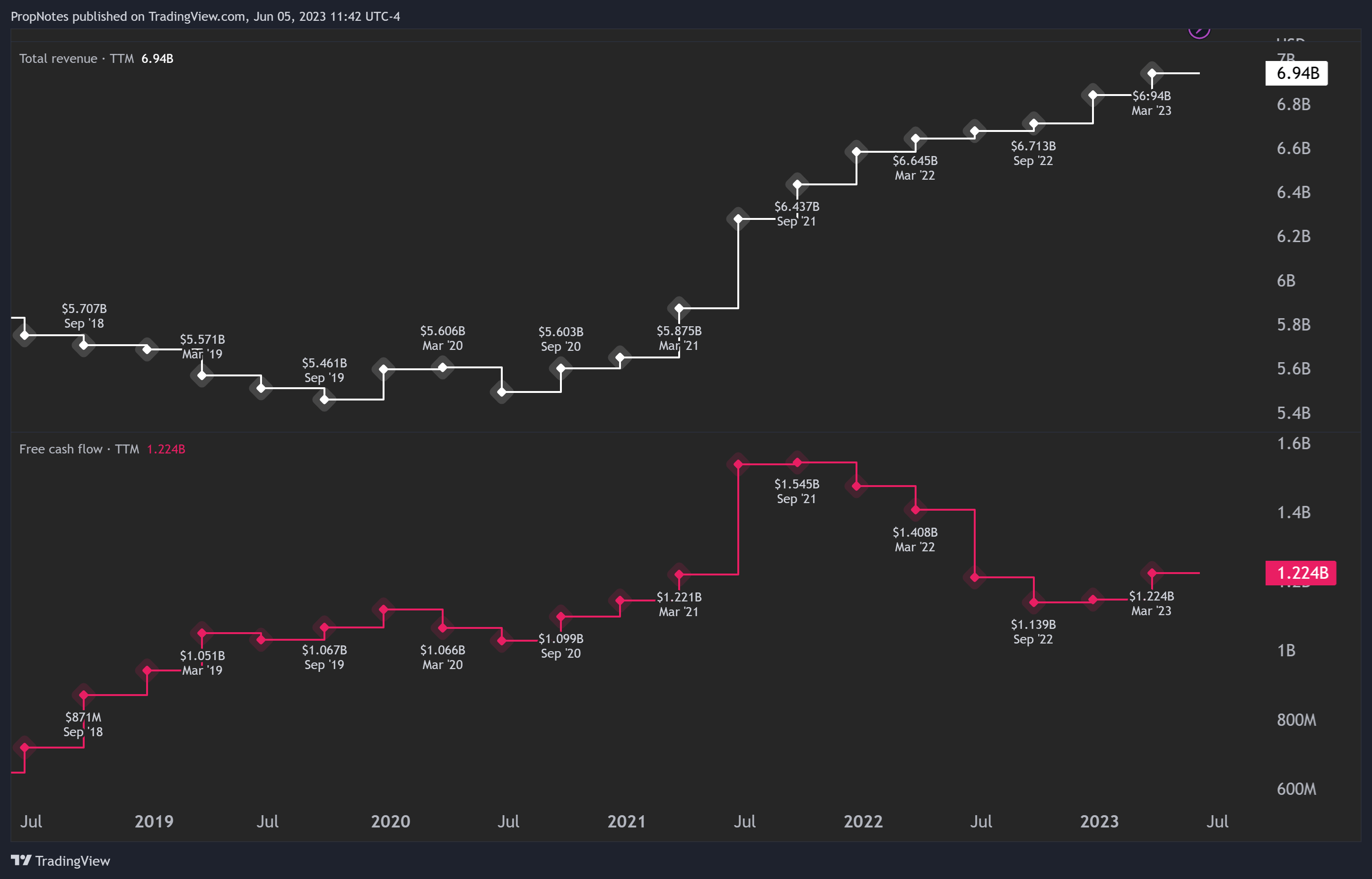

Compare QSR's numbers above to YUM, which reported $6.9 billion in sales and $1.2 billion in free cash flow:

{kind=link}

Despite the differences in store count and system revenue, each company produces roughly the same amount of revenue and free cash flow.

There are some distinctions to be made, however.

YUM brands has seen stronger net margins over the last few quarters, as QSR's have deteriorated somewhat:

{kind=link}

{kind=link}

This seems concerning and could be a sign that less margin is trickling down to shareholders of QSR which could dent long term returns.

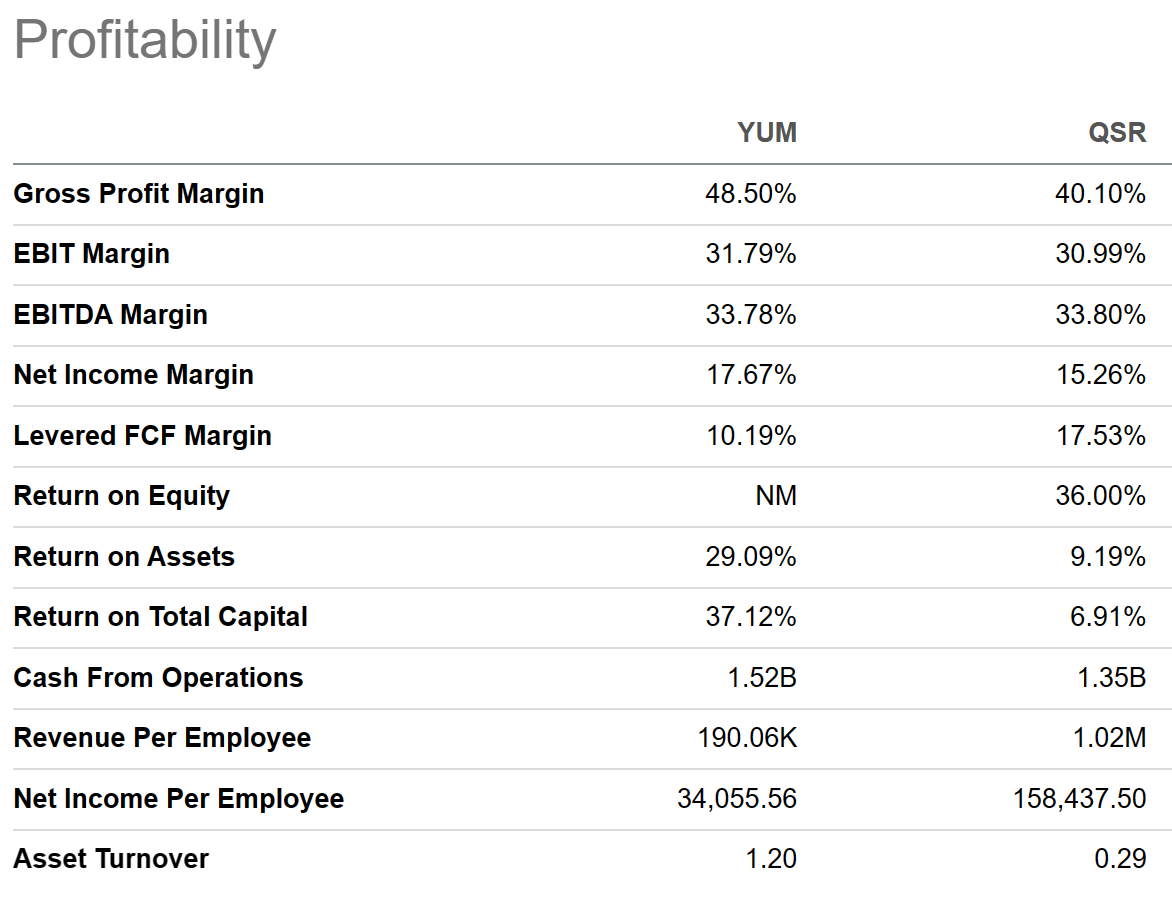

However, other profitability metrics tell a different story:

{kind=link}

QSR actually has better levered FCF margins, which to some is a better way of measuring the amount of cash available to return to shareholders as a percentage of revenue.

Taken together, we think YUM has had slightly better overall results, which is a good starting point to keep in mind as we continue to think about which company deserves a spot in your portfolio and may outperform in the medium to long term.

Routes To Increased Profitability

In order to get a better sense of which stock may make a better investment over the next few years, it's important, next, to look at the available levers that each company has available to improve demand for shares.

1.) Open more stores

The first option available to both companies is to open more stores. More stores means more revenue, and more revenue means more royalties, property fees, etc. Given that QSR has considerably less store units, while having higher same-store sales growth, it appears that pulling this lever has more upside for QSR than YUM. This is likely why they are growing units at 120 basis points faster per year than YUM is.

2.) Marketing / R&D

Marketing and R&D (new menu items) are the main ways that restaurant concepts can bring in more customers on a same store sales basis, which is what drives QSR and YUM free cash flow, assuming flat unit growth. We'd give the slight edge here to YUM brands. Taco Bell has significantly revamped its menu and now boasts one of the healthiest quick-service menus around, and YUM spends more on advertising as a whole.

3.) Control Costs

Both companies have negligible room to cut costs, as both QSR and YUM sport operating margins around 30%. This is in line with the industry, which indicates that there's not a lot of headway either company can make in the short term to reduce expenses.

4.) Capital Returns

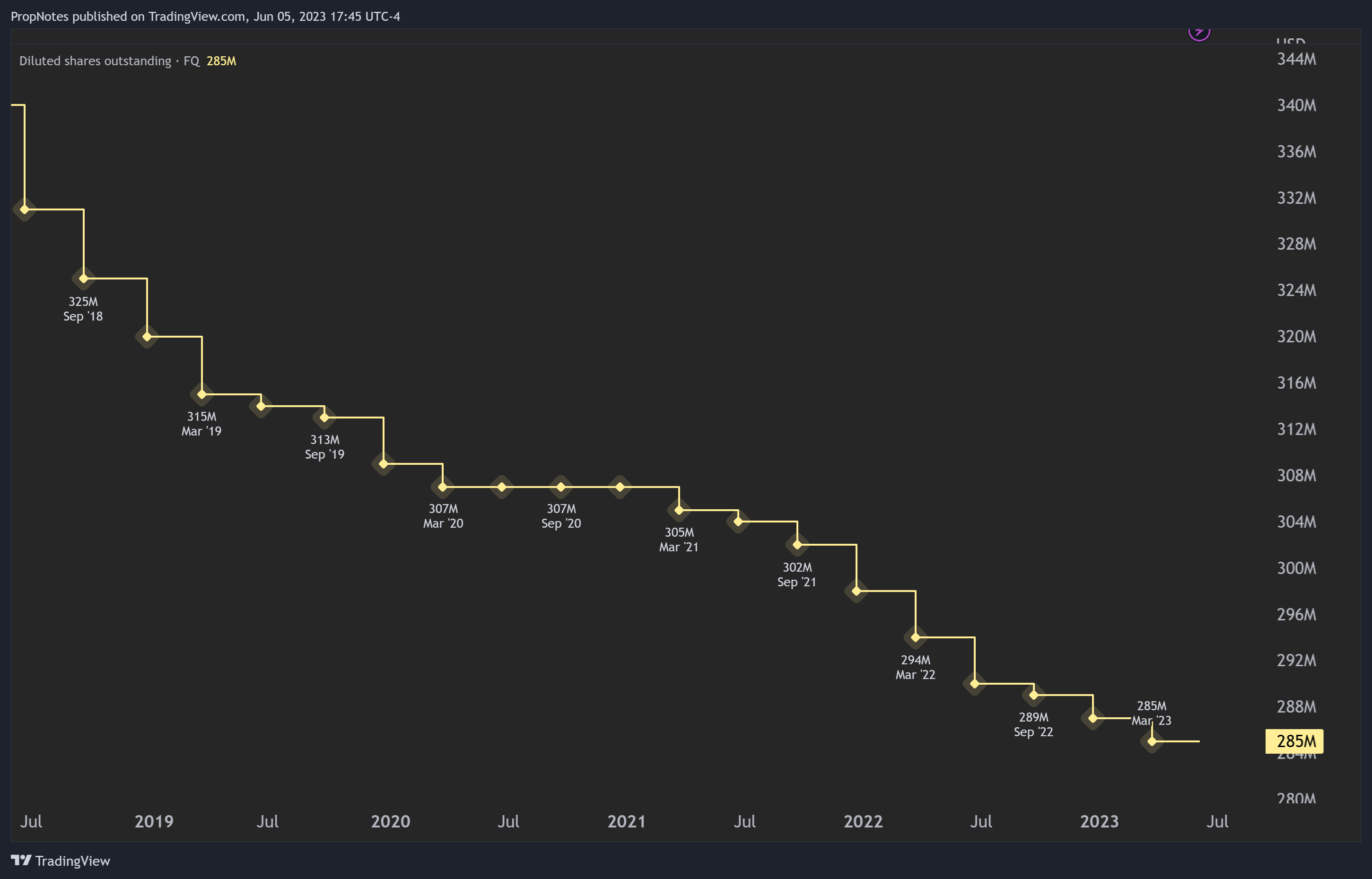

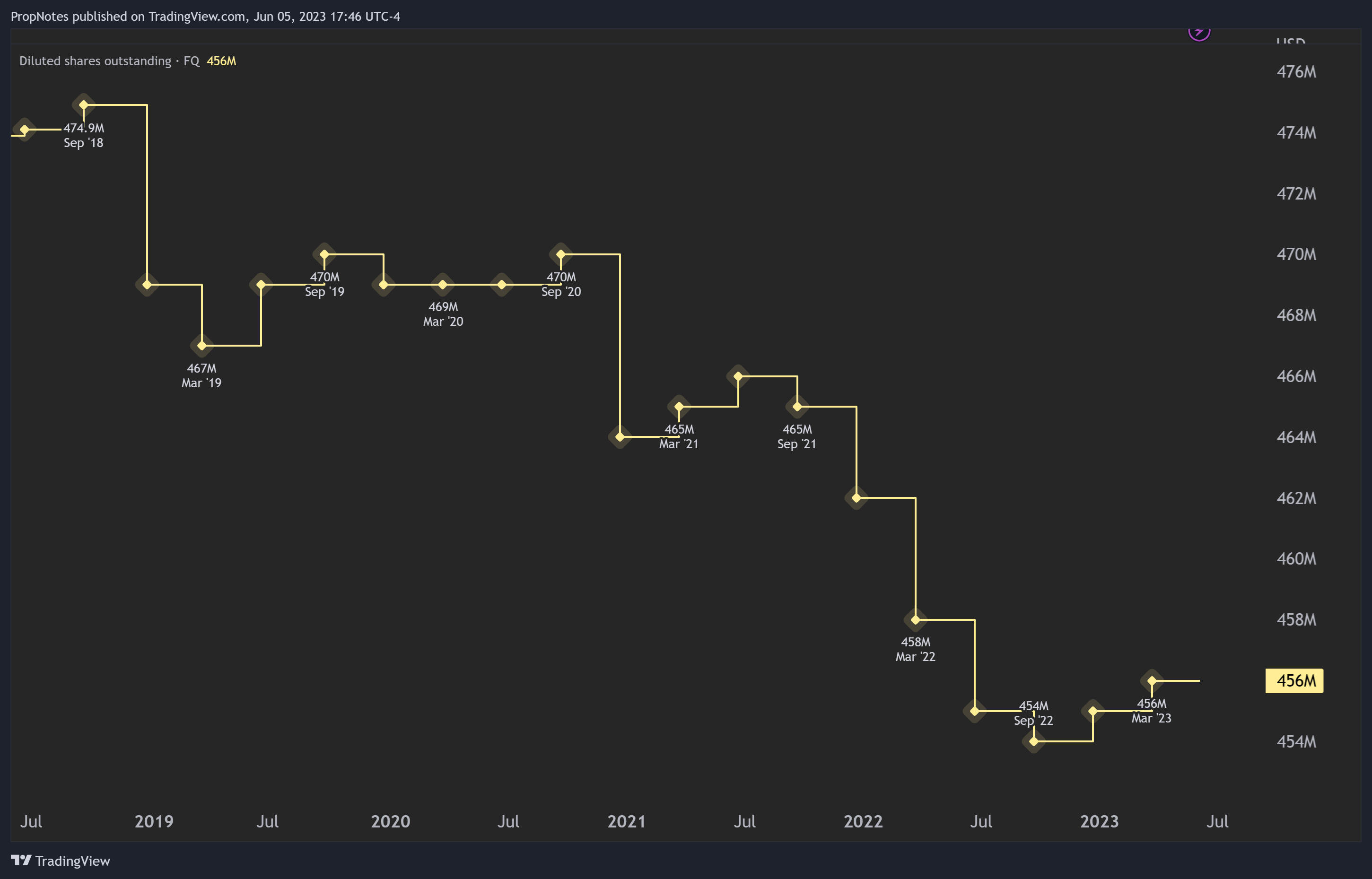

Both companies have been returning capital to shareholders by retiring outstanding stock from the market. Here's YUM's outstanding diluted share count over the last few years:

{kind=link}

And here is QSR's:

{kind=link}

Both companies have been reducing share count, although YUM has been more diligent, reducing outstanding shares by 15% vs. QSR's 4% over the last 5 years.

We'd give the slight advantage to YUM for their track record.

However, this must be balanced vs. a QSR dividend which ~100 basis points higher than YUM's, at 2.88% vs. 1.8%.

Valuation

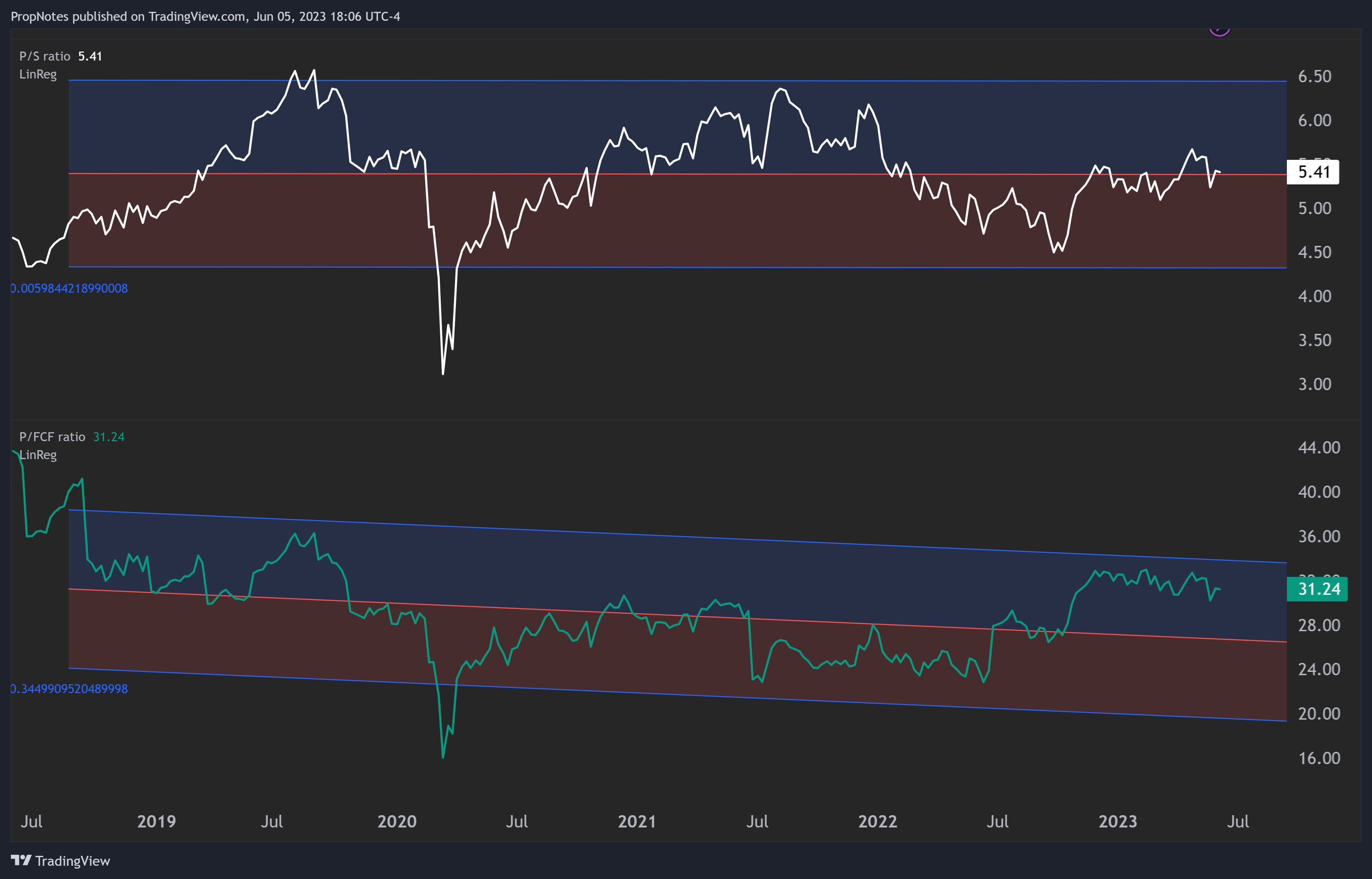

YUM and QSR's multiples are also similar; to the point of being a nonfactor. Currently, YUM trades at 5.4x sales and 31x FCF:

{kind=link}

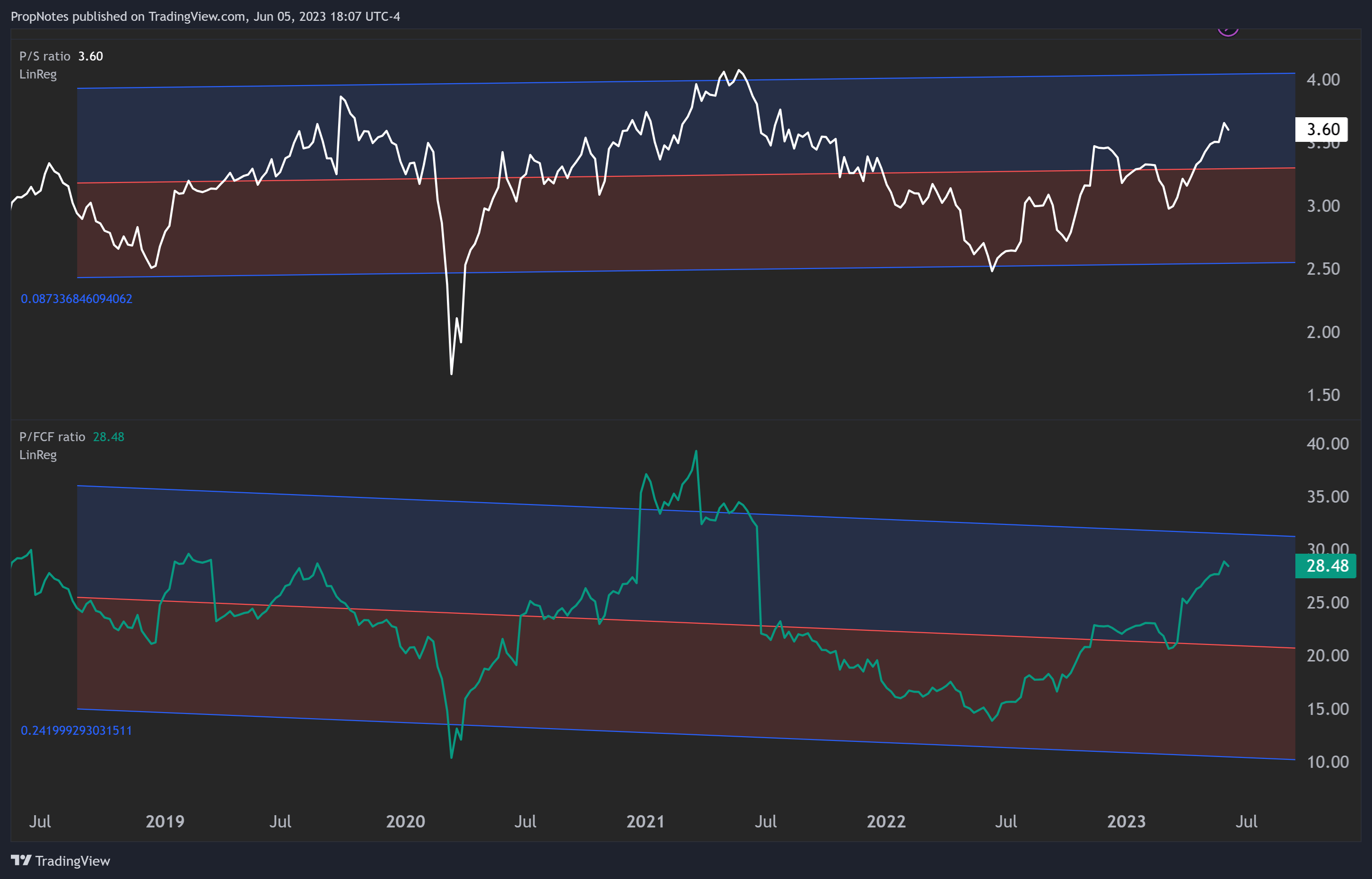

QSR is trading a little bit cheaper, but is also comparably priced vs. it's historical valuation at 3.6x sales and 28x FCF:

{kind=link}

Net-net, there's not much to see here.

Management

So far, it looks like a bit of a wash between YUM and QSR when it comes to financial performance, growth prospects, capital return policies, and valuation.

That is, until you get to management.

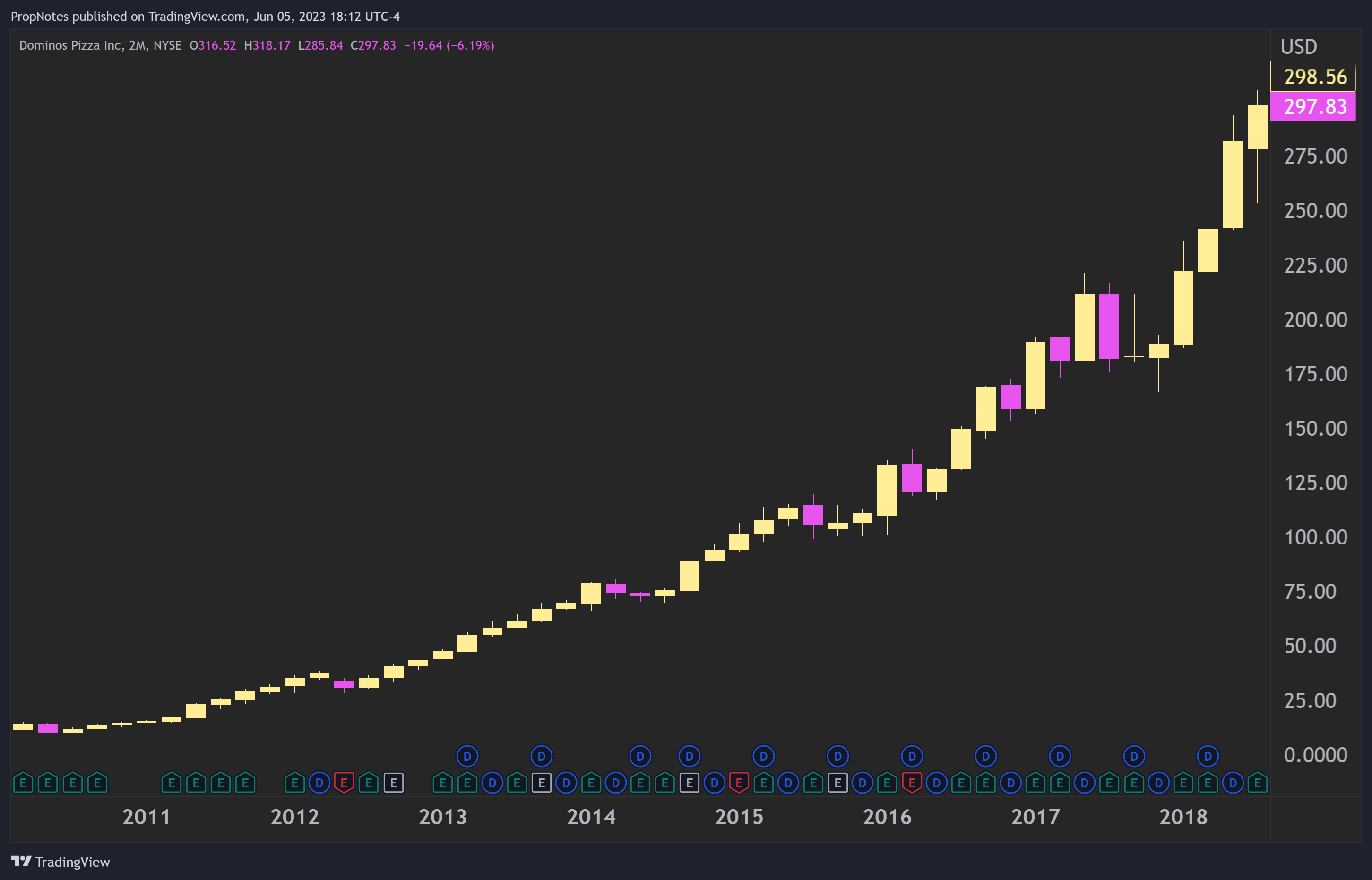

Recently, QSR brought in Patrick Doyle, the previous CEO of Dominos that oversaw the massive turnaround in the company. As you may well know, the stock saw unbelievable outperformance during his tenure:

{kind=link}

If you want to read more about how this may impact the company, Bill Gunderson recently wrote a great article about it. Suffice it to say that we feel the same as Bill, in that the potential for significant upside exists, particularly with the historically lackluster Burger King brand.

If anyone can unlock value, Patrick Doyle seems like the man. While he is acting in an executive chairman role and likely won't be involved in the day-to-day operations of the company, he's a massive value add.

Taken together with the higher upside that exists in further growing store unit count, and we believe that overall, QSR is positioned for solidly higher total returns over the next few years vs. YUM.

Risks

There are some risks to this thesis, the key one being that YUM still holds nearly a quarter of YUM China ( YUMC ) on its books, and should those shares experience material upside, then it's likely that the company could outperform QSR.

Additional risks also present in that YUM has significantly more emerging markets exposure vs. QSR, and should the U.S. deteriorate vs. EM, then YUM seems more well positioned.

Summary

Overall, a combination of exciting new management and better ROI from new store growth makes us think that QSR stands a solid chance of outperforming YUM over the next few years. While there are some risks to this thesis, we think QSR deserves a spot in your portfolio, and YUM, by extension, may be worth passing on.

For further details see:

Yum Brands Vs. Restaurant Brands International: Which Is The Better Buy?