ZBRA - Zebra Technologies: Good Company Amid Temporary Headwinds

2023-06-01 11:33:39 ET

Summary

- Zebra Technologies Corp. is a global leader in providing innovative solutions for the Automatic Identification and Data Capture [AIDC] industry.

- Despite all the difficulties, management isn't burying its head in the sand and continues to maintain the quality of the company's margins.

- If we return to historical valuation norms, Zebra Technologies stock has an upside potential of 9-18% by year-end, barring a recession.

- I rate ZBRA stock as a Buy this time.

The Company

According to the latest 10-Q filing, Zebra Technologies Corporation (ZBRA) is a global leader in providing innovative solutions for the Automatic Identification and Data Capture [AIDC] industry. Zebra's solutions span across various industries, including retail, e-commerce, transportation logistics, manufacturing, and healthcare. The company collaborates closely with customers and partners to optimize end-to-end workflows and solve complex business challenges.

The company has 2 product categories: Tangible Products [83.3% of consolidated sales] and Services and Software [the remaining 16.7%]. Zebra reports under 2 operating segments, based on served market areas:

- AIT segment [35% of sales] : barcode printing and asset tracking technologies, including printers, supplies, and services.

- EVM segment [65%] : automatic data capture solutions, offering mobile computing, data capture, RFID, scanning, machine vision, and workflow optimization solutions, along with services.

{kind=link}

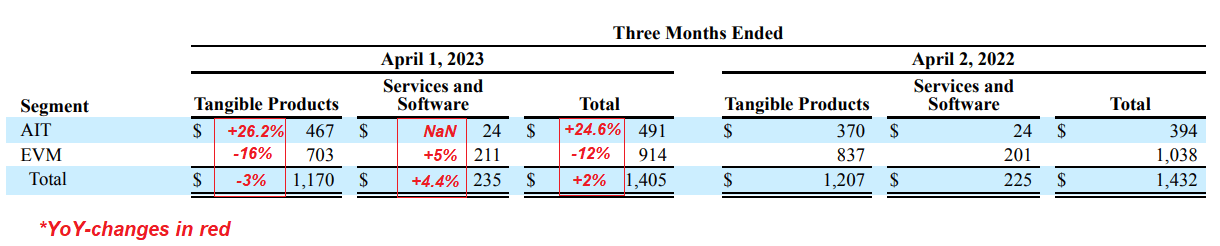

As we can see from the latest financial data, ZBRA is gaining momentum in barcode printing and asset tracking technologies and losing revenue in what remains its most important segment - automated data capture solutions. The multi-directional dynamics of the financial indicators suggest either attempts to reorient the business from one niche to another, or competitive weakness in the largest segment against the backdrop of strength in the smaller one. At this stage, it became interesting for me to look at the growth prospects of two addressable markets - the barcode printer market and the automatic data capture market. The first market - the one where Zebra is seeing growth - is expected to reach $11.06 billion by 2032 , growing at a CAGR of 7 - 9 %, according to various public sources. The second market - the one where Zebra is declining - is expected to reach $36.5 billion by 2027 , growing at a CAGR of 11- 14 %. As far as I can see, the data doesn't favor ZBRA - the company is losing in a more attractive market in terms of business expansion.

But upon further analysis, I discovered that the management's objective does not involve reducing operations in their largest segment. The decline in that segment is primarily due to reduced demand caused by fewer large order deployments in the EVM segment.

In 2022, the logistics industry experienced significant changes, especially in terms of peak lead times in the supply chain. In the meantime, however, the logistics situation has relatively stabilized in most enterprises. Consequently, the focus on process automation and optimization has taken a backseat. For Zebra's clients, the primary concern is to retain its own customers, who are likely to face the impact of high prices. Global inflation is coming down, but it is accompanied by a slowdown or decline in wages for certain population groups. This has led to lower demand for various goods and services, as prices are rising faster compared to wage growth. I've provided further details on the demand situation in my recent macro article .

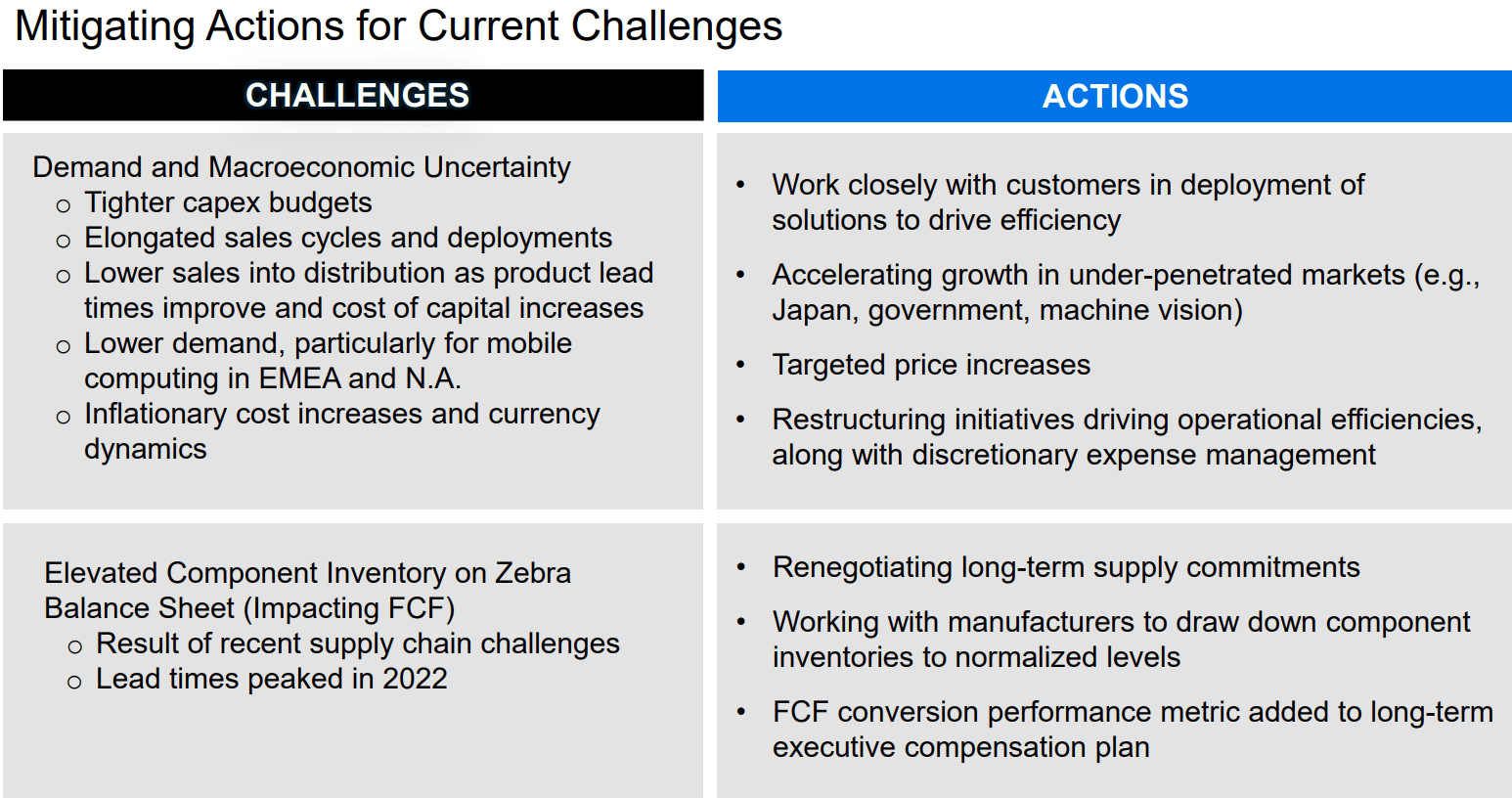

The good thing about Zebra Technologies is that the company is aware of all the challenges and doesn't bury its head in the sand, but speaks out about them openly [ Q1 FY23 presentation ]:

{kind=link}

Management's awareness of the issues created by the supply chain strengthening [its weakness drove demand from 2020 to 2022] is a key factor, in my opinion. This made ZBRA possible to switch from aggressively expanding the business to "energy saving mode" on time. By "energy", I primarily mean margin and profitability.

{kind=link}

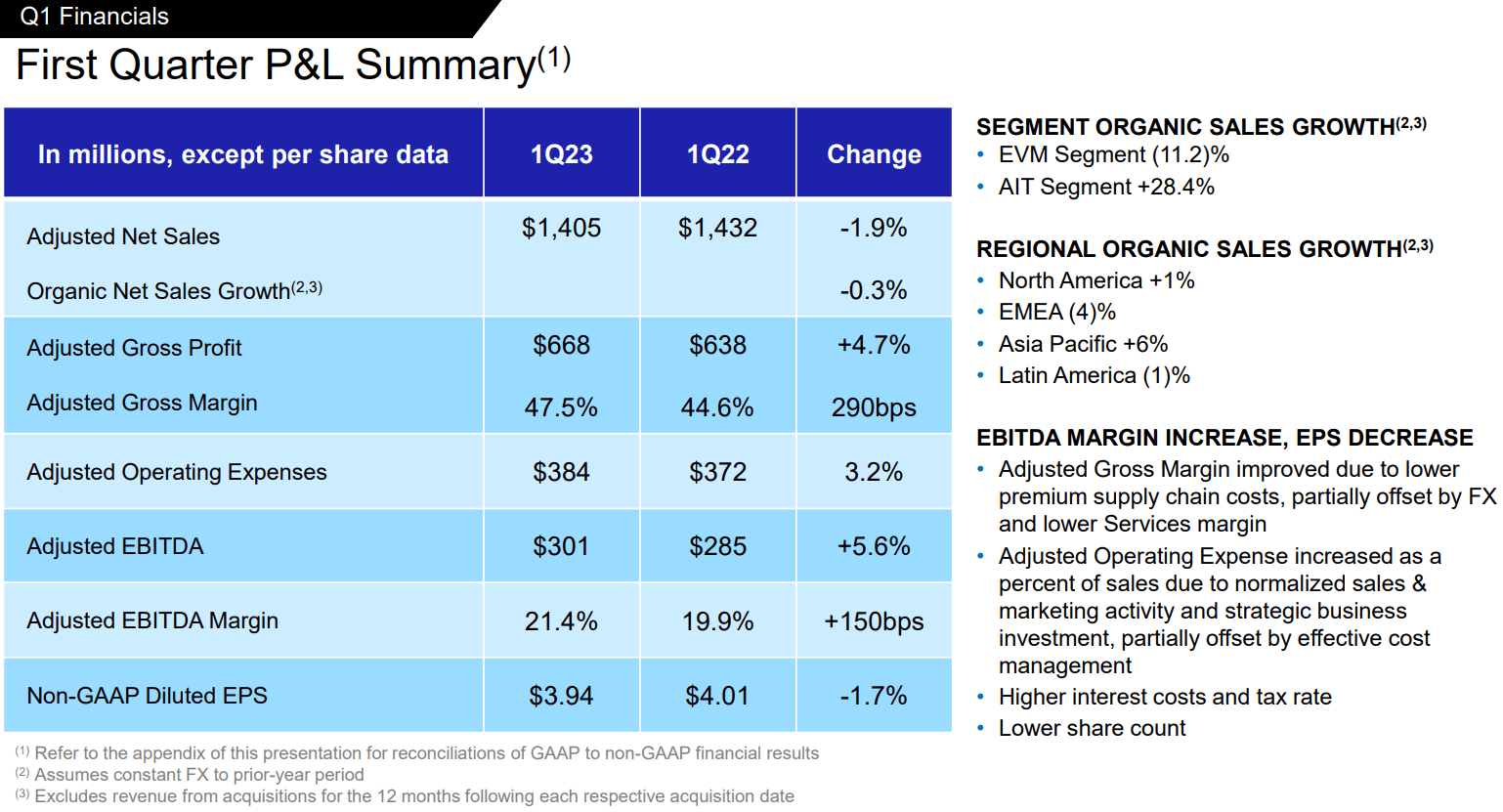

In the first quarter, Zebra Technologies experienced a 1.9% decrease in net sales, including currency impacts, with a 0.3% decline on an organic basis. But ZBRA's adjusted gross margin improved by 290 basis points to 47.5%, primarily due to lower premium supply chain costs, partially offset by foreign exchange impacts and lower service margins. Adjusted OPEX increased by 130 basis points as a percentage of sales, driven by normalized sales and marketing activity and strategic investments. Adjusted EBITDA margin increased by 150 basis points to 21.4%, supported by gross margin expansion. Non-GAAP diluted earnings per share decreased by 1.7% year-over-year, primarily due to increased interest expense and higher tax rates.

The main question I had for Q1 EPS was whether increased taxes and interest are the new norms. The total interest expense was primarily due to a $7 million loss on interest rate swaps and higher interest expense resulting from increased debt levels and interest rates, according to 10-Q. The effective tax rate for the respective period was 18.9% [vs. 18.0% in Q1 FY22], with the increase attributed to a higher U.K. statutory tax rate offset by changes in the global earnings distribution. So the answer to my question is probably yes - higher taxes and interest on payments will likely be the new normal for Zebra.

As per the company's CEO Bill Burns [ 1Q Earnings Call ], Zebra is focused on driving profitable growth , increasing market share, and improving free cash flow through customer collaboration. With the inevitable return of customers to automation needs, Zebra's focus on enterprise asset intelligence should grow at about the same rate as the addressable market over the long term. Exactly how that may affect the company's share depends on its valuation - and we'll turn to that now.

Valuation & Expectations

Seeking Alpha's Quant Ranking System gives Zebra Technologies stock a "C" in "Valuation" grade , showing that ZBRA is potentially fairly valued at its current levels. The stock itself is trading at ~15x of the Non-GAAP TTM price-to-earnings ratio and at ~16.6x of the next-year ratio.

As for EV/EBITDA, a more informative multiple in my humble opinion that seems to be calculated by various platforms on an unadjusted basis, ZBRA is currently trading around the lower end of 2017-2020 levels, which is a good sign for those looking for undervaluation.

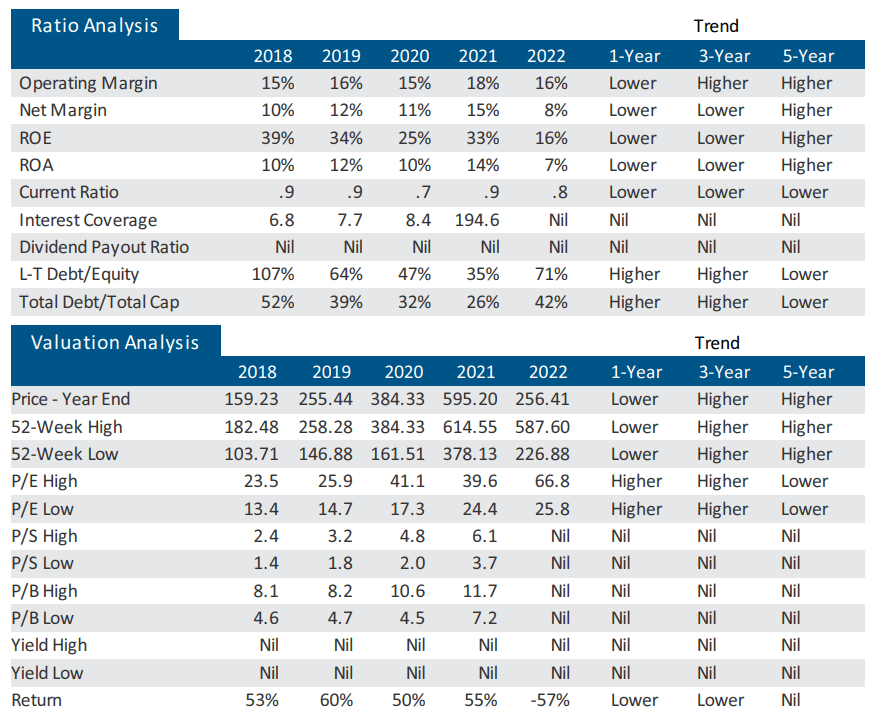

Let's go back a few years to understand the requirements for such a business valuation. I suggest that we first focus on margins.

{kind=link}

Zebra was already a relatively mature company back then [for reference, the firm went public in 1991], so before the period of abnormal demand growth in 2021-2022, the EBIT margins were consistently around 15-16% [2018-2020]. Right now we're at 16.6% and I expect ZBRA to be at 17-18% in a few years.

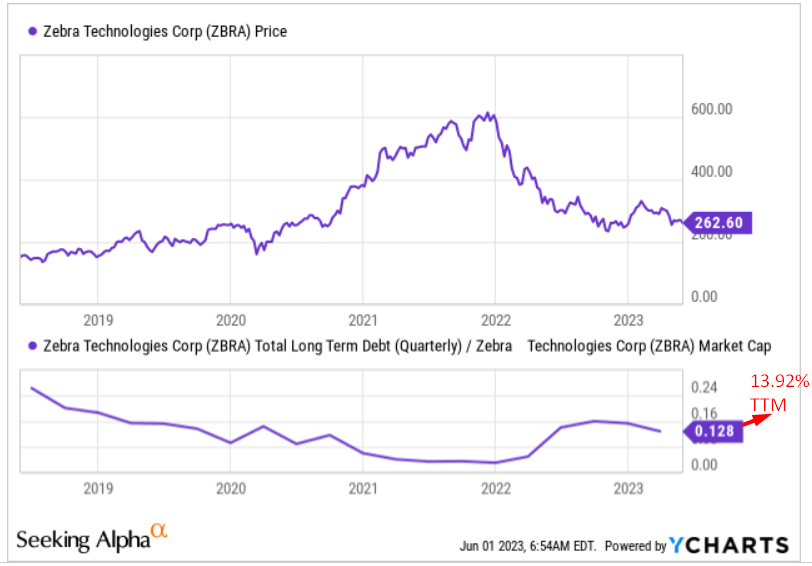

The amount of debt on the balance sheet has increased uncritically over the last 5 years - according to first-quarter data, it's actually lower relative to market capitalization than in 2019.

{kind=link}

Yes, the fact that ZBRA has to pay higher interest rates is somewhat frustrating. However, the increase in debt is modest - the company has the resources to manage these payments without jeopardizing profitable growth.

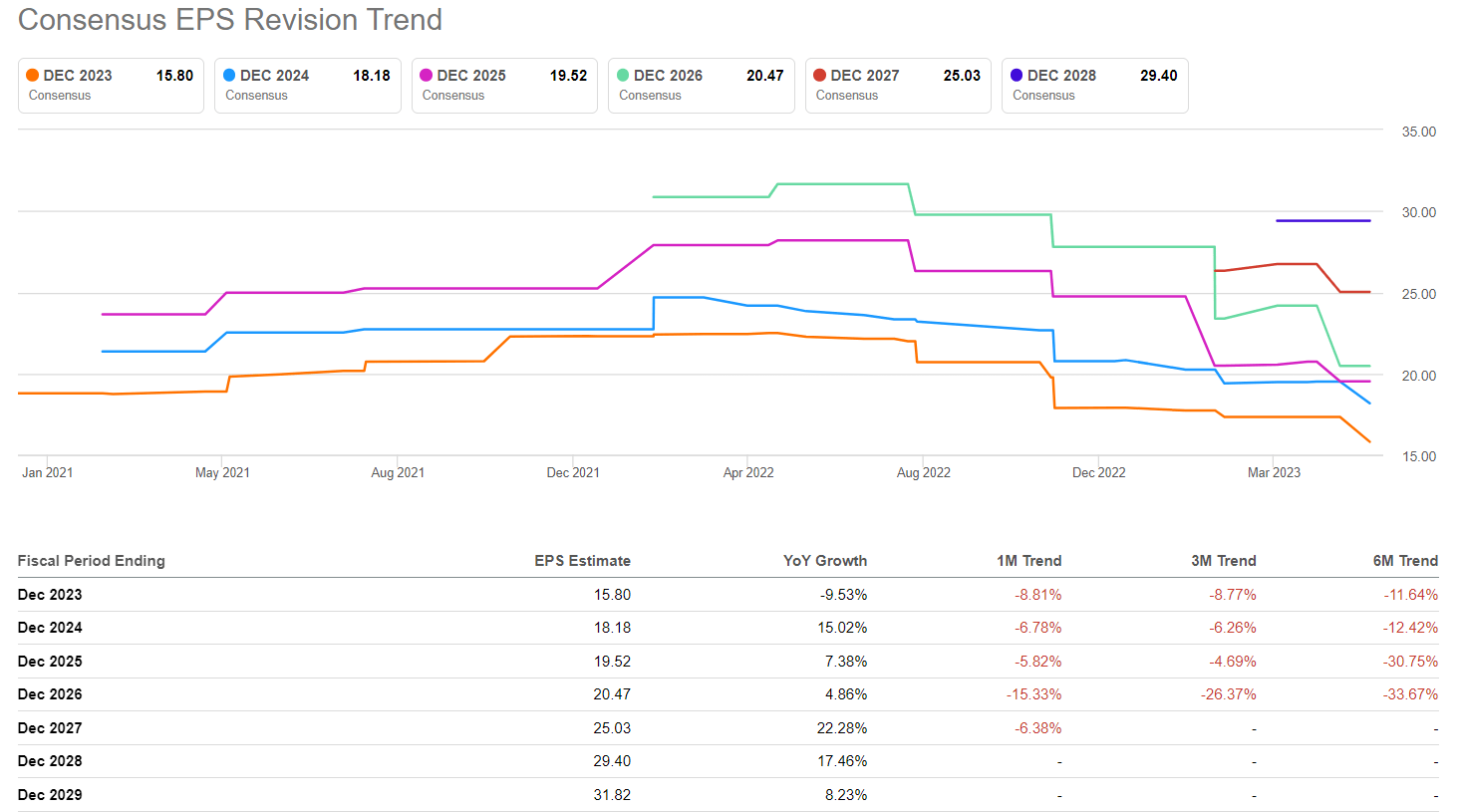

Analysts expect Zebra to post a 4.74% decline in revenue and a 9.53% drop in EPS this fiscal year. After that, however, there should be a recovery period in growth: Revenue will grow 5-10% year over year [per annum], and earnings per share will grow 5-22% over the same period. And this despite the fact that none of the analysts has raised his/her forecast in the last 3 months - quite the opposite:

{kind=link}

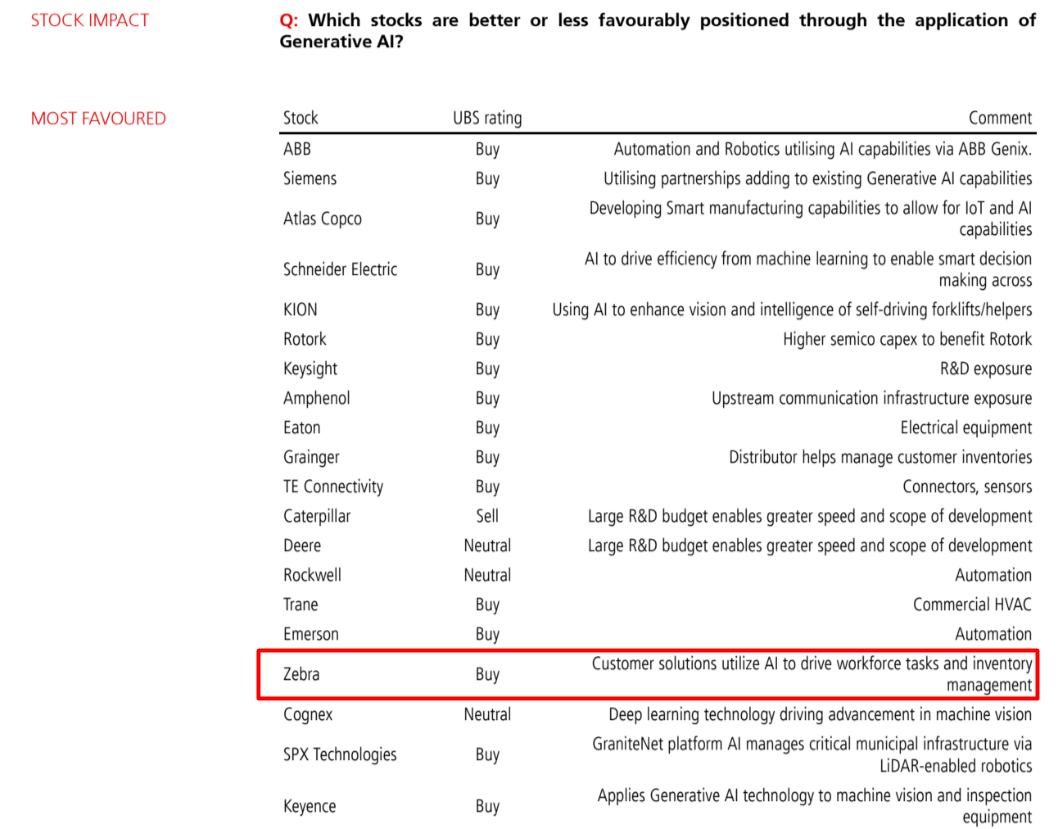

And just recently, a new study from UBS [proprietary source, 11/26/2023] was published that identifies Zebra Technologies as one of the best-positioned companies to deploy and benefit from Generative AI:

{kind=link}

So I expect Wall Street to start revising its EPS forecasts soon - but this time in a positive direction for ZBRA. And here, it seems to me, it'll be important not to look at the growth of the company's business - this can keep falling if the macro state of the economy continues to deteriorate. It'll be enough for ZBRA to continue to strengthen margins.

Assuming the current TTM EBITDA margin of 20% rises to just under 20.5% [+50 b.p.] by year-end, I calculate that Zebra should be able to generate EBITDA of $1,132 million on consensus revenue of $5.52 billion. At an EV/EBITDA of 15-16x, ZBRA stock should trade at an enterprise value of $17-18.1, or a market cap of $14.8-15.9 billion [EV net of net debt]. That means the undervaluation is 9-18%, making ZBRA an undervalued company.

However, this is only true assuming growth is truly in line with consensus. Historically, the company likes to beat forecasts - in the last 2 years, it has beaten forecasts in earnings per share 87.5% of the time.

The Bottom Line

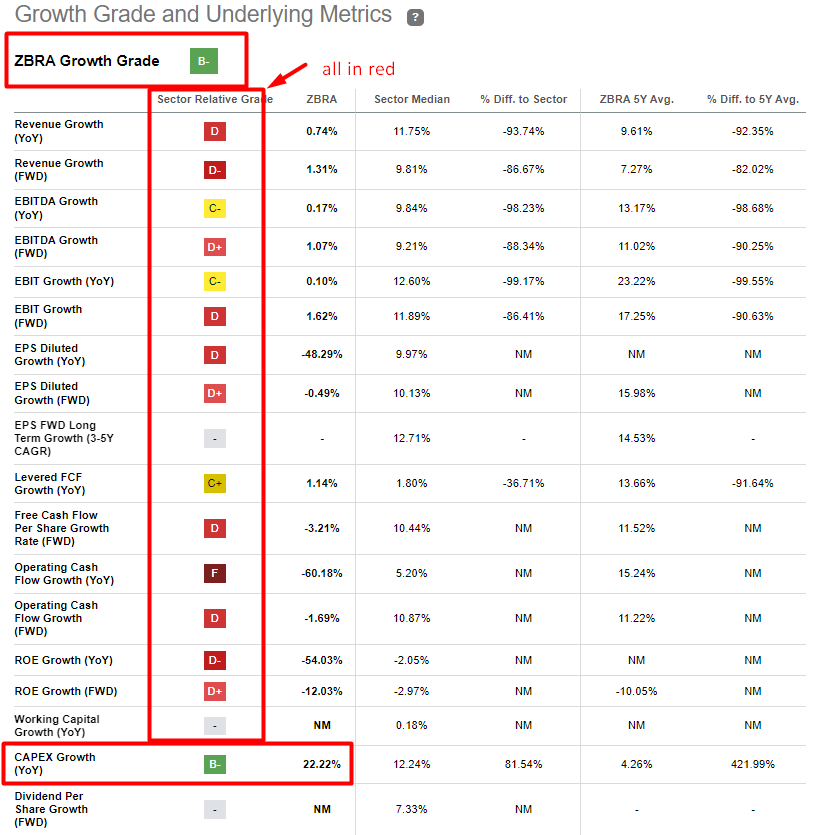

The biggest risk I see for buyers today is the shelving of supply chain automation by Zebra's customers due to slowing end-consumers demand. The fall of lead times has already occurred and is clouding Zebra's growth picture - the stock is rated "B" by Seeking Alpha's Quant System because its CAPEX growth is higher than the industry's median. To be honest, that's not exactly the height that bulls want to see.

{kind=link}

However, I believe that in the long run, the automation needs will take its toll and Zebra's consumers will come back with a new request. The company's financial stability and its focus on quality financial development should help it weather the storm in relative safety and gather strength before the next bullish cycle. The preconditions in the form of the fundamental problem of lack of AI integration in the supply chain are on the surface - it just takes a little time.

If we return to historical valuation norms, Zebra Technologies stock has an upside potential of 9-18% by year-end, barring a recession. If the recession happens, ZBRA stock, like everything else, will fly much lower. In that case, you'll get an opportunity to buy even cheaper.

Thanks for reading!

For further details see:

Zebra Technologies: Good Company Amid Temporary Headwinds