ZIM - ZIM Integrated: Why The Red Sea Shipping Crisis Could Allow It To Shower Shareholders With Free Cash Flow

2024-01-17 07:11:58 ET

Summary

- ZIM Integrated Shipping Services is a deep-value opportunity trading at 0.56x book value headed into a rapidly rising earnings environment.

- Based on interviews with experts, I believe that the Red Sea shipping crisis will be long-lasting and result in heightened container freight rates globally.

- Freight rates have been rapidly risin, but even if they stabilize from here, I estimate that ZIM will earn 2.2x its market cap in free cash flow over 12 months.

- I have a target price of $48 per share for the Company based on its current book value and estimated free cash flow, representing 258% upside from current prices.

Thesis

In this note, I consider the business of ZIM Integrated Shipping Services ( ZIM ) and explain why I believe it will shower shareholders with free cash flow throughout 2024. I explain why container vessels will continue to avoid the Red Sea for the foreseeable future despite the recent military buildup. As container ships go the long way around the Cape of Good Hope, freight rates will settle at heightened levels like they have throughout history. In my view, a sustained doubling to tripling or more of freight rates will drive significant free cash flow generation for the container shipping industry. This research analysis explains why I believe ZIM is uniquely poised to benefit and why the shares currently offer deep value.

Company Background

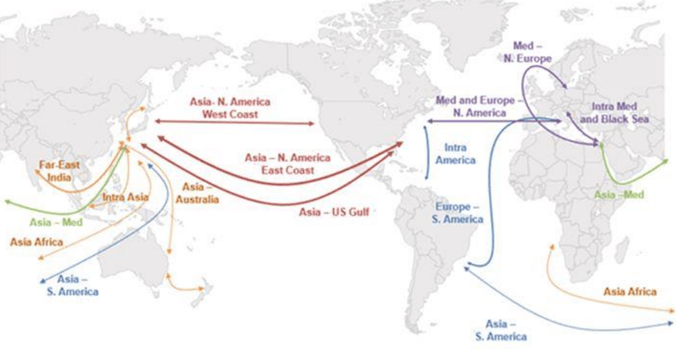

ZIM is an Israeli container shipping company. It's the 10th largest shipping line in the world when measured by twenty-foot equivalent units ((TEU)) of container carrying capacity. This year the company is on track to transport around 3.4 million TEUs all around the world. The company is focused on the Transpacific route as well as intra-Asian trade but also has significant exposure ( 26% ) to Atlantic trade and Cross-Suez trade that is more directly impacted by Suez Canal disruptions. Broadly speaking, ZIM has deployed its fleet in similar proportions to global trade volumes between regions. For reasons I will explain below, I anticipate the entire fleet will eventually be impacted by the Red Sea disruptions as the increase in ton-mile demand flows through globally. The following chart shows the trade routes ZIM serves:

{kind=link}

ZIM has control of 129 containerships and 16 car carriers. The company generates all of its revenues by charging customers to transport containers and cars on the vessels it controls as well as freight forwarding. Uniquely, ZIM charters in the very large majority of its operated vessels. Of the 129 containerships it controls, ZIM has chartered in 120 . The charters that ZIM enters into usually include the cost to crew the boat, and are usually around, on average, 2 years in duration.

The Situation in the Red Sea

In this section, I share my unique insights and learnings I've gathered from my own research as well as from a military expert with real-life experience defending the chokepoints of the Arabian Peninsula. I was able to contact this military expert through former shipping colleagues of mine, and he agreed to provide me with these insights on the condition of anonymity. The context of the discussion was a three-hour conversation and continued follow-on messages with this expert. This military expert served in the Australian Defense Force (ADF) for decades. He did multiple tours of Afghanistan and, after rising up the ranks to Lieutenant Colonel, was posted to the Al Minhad Airbase in the UAE. One of his remits while based in the UAE for 2 years was to oversee Australia's participation and deployment of HMAS Toowoomba in the International Maritime Security Construct (IMSC). The IMSC was set up by a group of like-minded countries to protect vessels transiting the Strait of Hormuz and Bab al-Mandab Strait chokepoints.

Buffett urged investors to focus on the important and determinative facts of an investment situation. In this case, how long the Houthis continue to attack commercial vessels transiting the area or not, will be the most important driver of container freight rates and, therefore, ZIM's earnings. The expert told me that Operation Prosperity Guardian (OPG), the recent American-led navy taskforce tasked with protecting commercial vessels in the Red Sea, was unlikely to be effective at solving the current crisis.

The reasons navy vessels won't be able to protect commercial vessels transiting through the Red Sea are: (1) the expanse of water around the Yemeni coastline is too grand. While the strait appears small on a map, it's deceptively large, and it's not possible to see from one side of land to the other. Given how far missiles can travel, it's practically impossible to defend the entire stretch of sea. This was described to me as like playing whack a mole - you can't be everywhere all at once; (2) the small boat traffic in the Red Sea is too prolific for there to be airtight security of all vessels; (3) the sheer number of vessels transiting the Suez Canal is too large to protect each ship and (4) the Houthi have access not only to missiles and one-way attack drones but also manned and unmanned fast boats that are difficult to consistently prevent reaching commercial vessels.

Additionally, in my view and those of the experts, recent US airstrikes are unlikely to stop the Houthis from attacking commercial vessels. Empirically, even after the initial strikes on Western Yemen, the Houthis fired missiles at both commercial and navy vessels as well as launched fast boat attacks along the Yemeni coast. The Houthis have survived more than 25,000 missiles being fired at them for over a decade by the Saudi-US coalition during the previous civil war. This forced the Houthis to protect their mobile rocket-launching infrastructure far below ground where it can't be hit. According to experts on the group , Houthi leadership sees American attacks as an opportunity to make up for previous governing errors and to increase their popularity and effective control over Yemen. It's for these reasons, along with the difficulty of defending the Red Sea from varied threats that I surmise the crisis will be long-lasting.

Industry Transition

I have previously worked for a shipping container manufacturing business, which provided me with many contacts in the industry. I contacted a former colleague who used to be the managing director of one of the largest 3 global shipping lines based in Australasia and now works for a major port infrastructure business in the Middle East. He agreed to speak to me on the condition of anonymity. The insight he provided me is that, due to the Red Sea shipping crisis, the rules of the container shipping industry had changed. Shipping companies used to engage in behavior akin to "maximum competition" throughout the Covid spending boom, ordering as many ships to be built as they could get their hands on. But now with oversupply, the major lines all have an incentive to go the long way around the Cape of Good Hope. The longer voyage will more than offset the previous oversupply, enabling the industry to become profitable once again. If all the major shipping lines oblige, then they will all benefit. As a result, the container shipping industry has transitioned from a period of "maximum competition" to "covert cooperation."

The net judgment from the insights and expert feedback I've gathered is that the disruption to the Red Sea will last for a long time. As I'll discuss in the valuation section, the longer the disruptions last, the more free cash flow ZIM will be able to provide shareholders.

Impact on Supply and Demand for Container Shipping Industry Generally

Because of the Houthi threat mentioned in the previous section, the top 10 shipping lines, which make up 85% of the total global fleet , have decided to detour their ships around the Cape of Good Hope rather than through the Suez Canal. This results in a major increase in ton-mile demand. Around one-third of global container vessels previously transited through the Suez Canal. Normally, one-way, it would take around 30 days to sail from Shanghai to Rotterdam through the Suez Canal. Sailing around the Cape of Good Hope, however, takes around 43 days. If 33% of the world's container fleet travels an extra 43% in time, then I'd expect to see an increase of 14% in ton-mile demand.

A 14% increase in ton-mile demand is significant. To place this change in industry circumstance into context, I estimate that the freight rate boom (more than 10-fold increase in container freight rates) due to the heightened consumer spending over Covid was driven by a 20% increase in demand for imported goods. I estimate that the more than 10-fold increase in tanker charter rates since the start of the Ukraine War was caused by an 8% increase in ton-mile demand. While it's well-recognized that the global supply of container ships has increased around 6% in 2023 net of scrapping, the net increase in ton-mile demand is still significant enough (around 8%), in my view, to produce at least a two or three-fold rise in container shipping rates. To be conservative in my estimate, I haven't included the impact on ton-mile demand from continued disruptions to the Panama Canal either. Global container freight indices have already risen by around double and, as the disruption continues, the impact will continue to trickle through. As a result of this shock to container shipping supply and demand, I believe it's likely we'll see at least a 2-3 fold rise in container freight rates for a lengthy period of time.

ZIM Financials and Valuation - Why Red Sea Developments Impact ZIM the Most

What would a lengthy demand shock caused by continued Red Sea disruptions mean for ZIM? I believe that an extended Red Sea shipping crisis would be a boon for ZIM in particular. ZIM is likely to benefit in particular because it has more leverage to raise freight rates. Unique to the industry, ZIM charters in 120 of its 129 operated container vessels rather than taking an ownership stake. Almost all its charters require the owner to operate and pay for the operating costs of the vessel. The charters ZIM enters into have around, on average, around 26 months until maturity. This chartering structure, compared to a traditional ownership structure, means that ZIM has a relatively more fixed cost base. As variable freight rates rise, the lift in revenue goes straight to the bottom line.

Because previous charters were struck at relatively high rates during the Covid spending boom, after freight rates reverted back to normal ZIM started to make a normalized loss of around $207 million per quarter. But as freight rates rise, the percentage change in ZIM's profitability will rise much more than its competitors since its earnings rise off a lower base. Additionally, since ZIM is the 10th largest shipping line and is very small compared to the biggest 3, the marginal producer of a competitive industry usually has the biggest profit changes when a shock occurs.

Additionally, ZIM's cost base will fall compared with time as older and more expensive charters mature. As these old charters roll off and new charters are struck, including for the remaining 33 deliveries throughout 2024, ZIM's cost base will gradually fall. This process and benefit to ZIM should largely run its course throughout 2024.

My analysis above discussed why I believe charter rates could at least double for more than 12 months. In the following table, I show what this supply and demand shock would mean for ZIM's earnings power:

Estimate of Normalised ZIM Quarterly Earnings (ZIM Company Reports and Author Calculations)

If ocean freight rates doubled from their averages in 2023 Q3 across the world, then ZIM would go from losing $1 billion over the course of a year to earning around $4 billion per year (please be cognizant of the risks section related to this forecast). The company's book value would rise from around $2.5 billion to about $5.7 billion (I provide the calculation below). In the past, ZIM has showered its investors with special dividends to pass on the free cash flow the business earned. Unlike other shipping lines, this is possible for ZIM because the company doesn't need large amounts of working capital to buy new vessels since it charters instead. Much of the return for shareholders would likely come in the form of either share buybacks or special dividends.

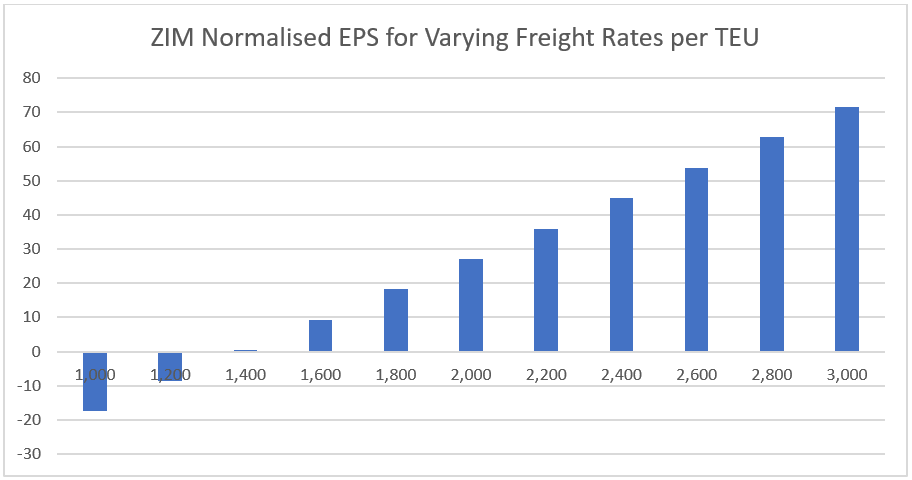

Assuming an effective tax rate of 20%, the following chart shows my estimate of ZIM's annualized earnings per share for varying freight rates per TEU:

ZIM Normalised EPS for Varying Freight Rates per TEU (ZIM Company Reports and Author Calculations)

{kind=link}

In the third quarter of 2023, ZIM reported an average freight rate per TEU of $1,139. At current global container shipping rates, which have already nearly doubled according to Drewry , ZIM would be earning around $2,280 per TEU. While it takes a couple of quarters for the impact of higher spot rates to fully feed through, since many customers strike short-term deals, I'd expect ZIM's average freight rate to rise above $2,400 per TEU as the Red Sea shipping crisis persists and the shock trickles through globally. In the next chart, I illustrate what varying freight rates for one year would mean for ZIM's book value in 12 months' time:

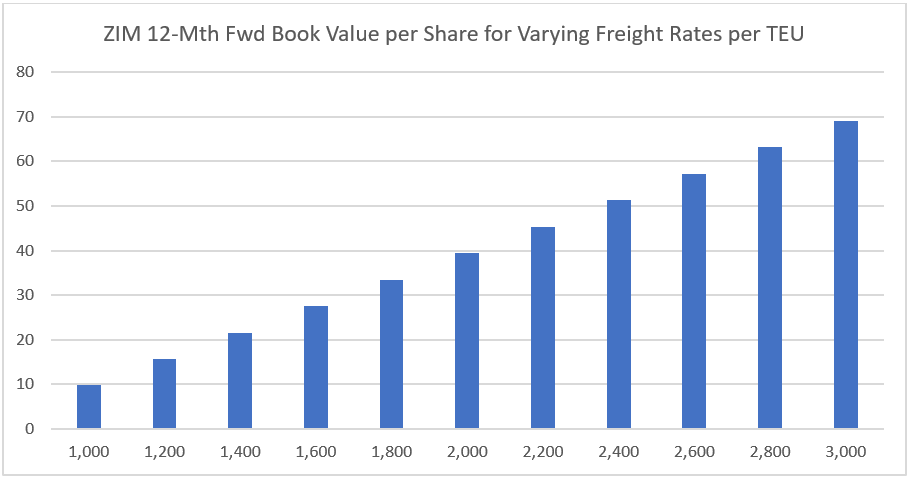

ZIM 12-month Forward Book Value per Share for Varying Freight Rates per TEU (ZIM Company Reports and Author Calculations)

{kind=link}

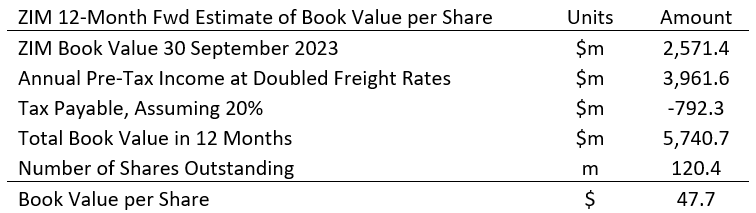

It's notable that if ZIM's earnings power doubles as in my base case, then it would result in a book value of around $48 per share after one year. I run through my calculations in the following table:

ZIM 12-Month Forward Estimate of Book Value per Share (ZIM Company Reports and Author Calculations)

{kind=link}

My estimate of the fair value for ZIM is based on a conservative doubling of global freight rates. The reason I believe this estimate to be conservative and not speculative is because, according to various sources, global freight rates have more or less already doubled. In my fair value estimate, I don't assume the impact of the Red Sea crisis further trickles through the global fleet like previous supply-demand shocks have. Continued disruptions to the Panama Canal as I outlined in my note on StealthGas ( GASS ), will likely cause the shock to be even larger than I have estimated for. To be conservative, I have not factored this impact in. Excluding these other impacts, my conservative fair value estimate of around $48 per share represents around 258% upside from the current price.

Risks

The main risk that would undermine my thesis is if Red Sea disruptions subside, causing freight rates to fall back to levels prevailing before the crisis began. In the current geopolitical climate, it's possible that the Red Sea shipping crisis could abate quickly. In such a scenario, ZIM would likely trade around where it was before the attacks began at around $8-10 per share. While this is the key speculative risk to the investment concept, I believe that the potential rewards far outweigh this risk at current price levels, creating both an asymmetric risk-reward profile and a meaningful margin of safety.

Summary

Given the expert insights I've scuttlebutted my way to understanding along with the research I've done, my judgment is that the Red Sea shipping crisis will prevail for a lengthy time. ZIM will earn revenues at heightened freight rates throughout this period that it can use to shower shareholders with free cash flow. If freight rates stop increasing and stabilize at current levels, then I estimate the fair value of ZIM's shares to be around $48 per share. This represents around 258% upside from the prevailing price.

For further details see:

ZIM Integrated: Why The Red Sea Shipping Crisis Could Allow It To Shower Shareholders With Free Cash Flow