ZIMV - ZimVie: Downgrade To A Hold On Valuation And Fundamentals

2023-06-21 00:15:26 ET

Summary

- ZimVie's stock price has increased by 19% since November, but the company's fundamentals have deteriorated significantly.

- The company's revenue guidance for 2023 is set at $848 million, a 6.7% decline from 2022, and LTM CFO has been cut in half from $55 million in Q3/22 to $27 million in Q1/23.

- With deteriorating fundamentals and higher valuations, I lower the rating on ZIMV to a hold and advise investors to wait for better valuations before considering a position in the company.

I last covered ZimVie Inc. ( ZIMV ) back in November, shortly after the company released Q3/2022 financial results. At the time, my conclusion was that ZimVie's shares were attractively valued, trading at less than 5.0x adj. Fwd P/E and P/CF. However, investors would need to have lots of patience, as it may take a few quarters for the company to regain investor confidence after its terrible start as a public company.

Fast forward 7 months and how has the company done? So far, my assessment appears to be correct, as the company has returned 19% compared to the price when I last wrote about the company, although there was a scary plunge in the company's shares in early March (Figure 1).

Figure 1 - ZIMV has rallied 19% since my last article (Seeking Alpha)

What happened in March and what has driven the subsequent rebound in the company's shares? Is ZIMV shares still a buy?

Brief Company Overview

For those new to the ZimVie story, the company was spun out of Zimmer Biomet ( ZBH ) in March 2022. Its business comprises the non-core lower growth dental and spine medical device businesses of Zimmer Biomet.

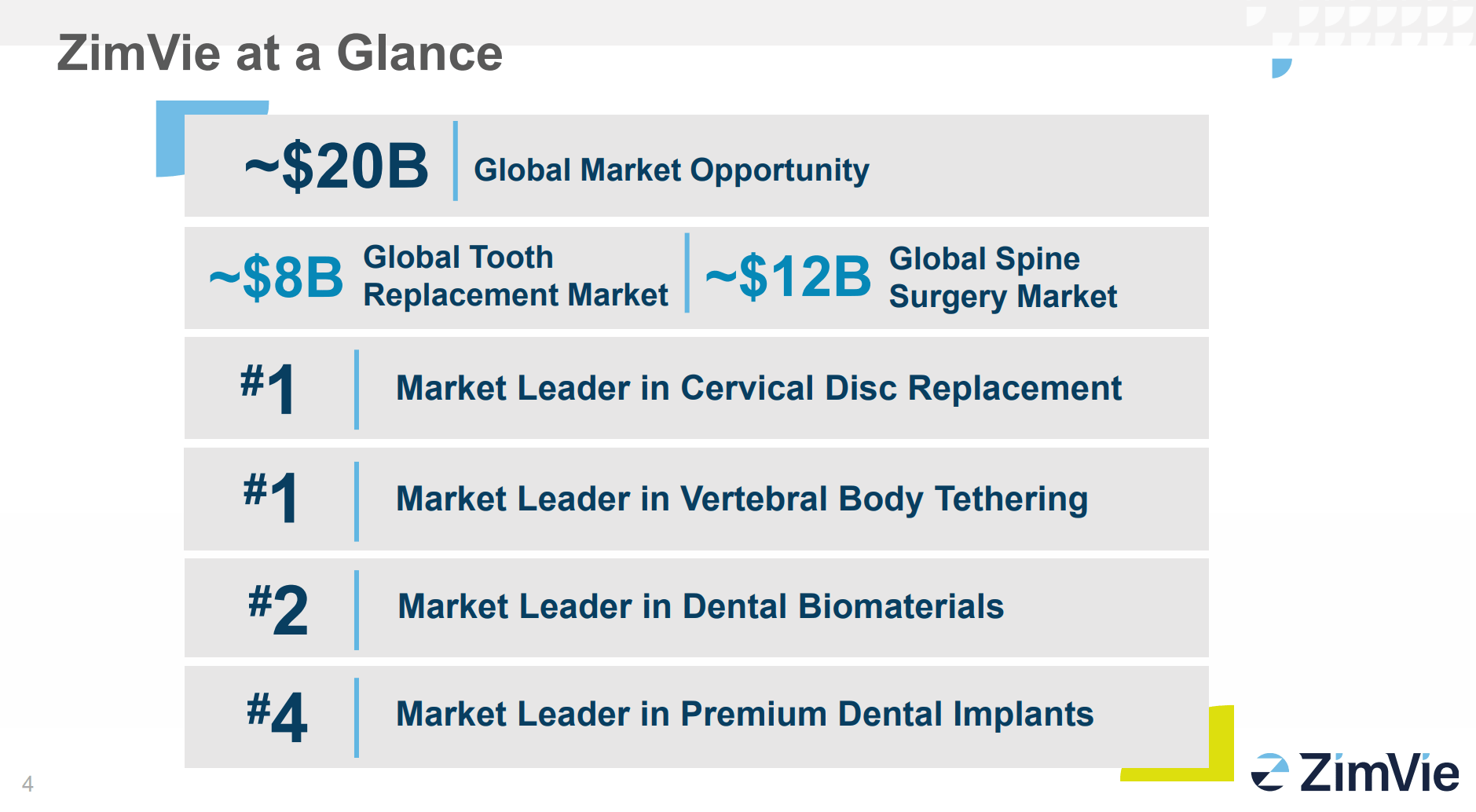

According to the company's estimates, it is the market leader in several sub-markets within the dental and spine medical device markets, including being the #1 market leader in cervical disc replacement and the #2 market leader in dental biomaterials (Figure 2).

Figure 2 - ZimVie overview (Company presentation)

{kind=link}

More company details can be found in my initiation article .

Q4 Was The Kitchen Sink Quarter...

In my last update, I noted that ZimVie was guiding to a pretty weak Q4/2022 earnings:

Taking the company at its word would imply quite a weak upcoming Q4, with revenues ranging between $230 - $245 million and adj. EPS of $0.14 - $0.34

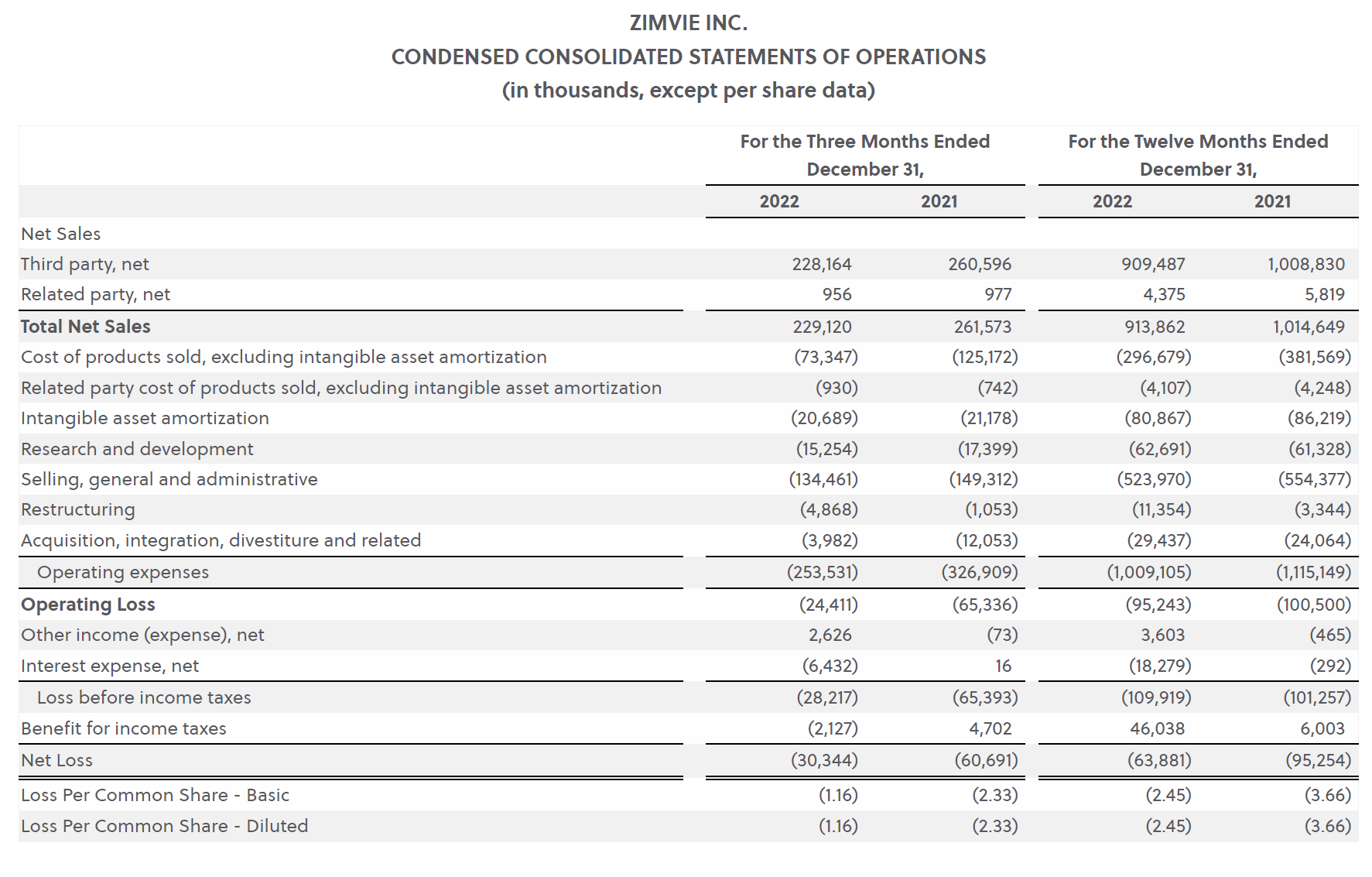

In fact, on March 1, 2023, ZimVie reported a poor set of Q4/2022 results, with top line revenues of only $229 million, missing its own implied range of $230 - 245 million. Adj. EPS was also weak at just $0.16 / share. For the full year, 2022 external sales came in at $909 million and ZimVie reported a GAAP net loss of $64 million, compared to $1.01 billion in external sales and $95 million in net loss in the comparative period in 2021 (Figure 3).

Figure 3 - ZIMV Q4/22 financial summary (Company press release )

{kind=link}

The detail that spooked investor the most was the company's initial guidance for 2023, which only showed $825 - 850 million in net sales and $0.30 - 0.50 in adj. EPS (Figure 4). This was far below consensus , which was looking for $925 million in revenues and $1.29 in adj. EPS at the time.

Figure 4 - ZIMV initial 2023 guidance (Company press release )

{kind=link}

Worried investors capitulated and punished ZIMV's stock severely, with the shares recording a 1-day decline of 44.6% on March 2, 2023.

...While Q1 Showed Modest Improvements

However, the early March drubbing appears to have cleaned out the last legacy shareholders of ZIMV, as the company's stock price have been in recovery mode since bottoming in the low $5s shortly after the Q4 earnings release. The kitchen sink-like guidance also reset expectations, setting up the company for 'beat-and-raise' performance.

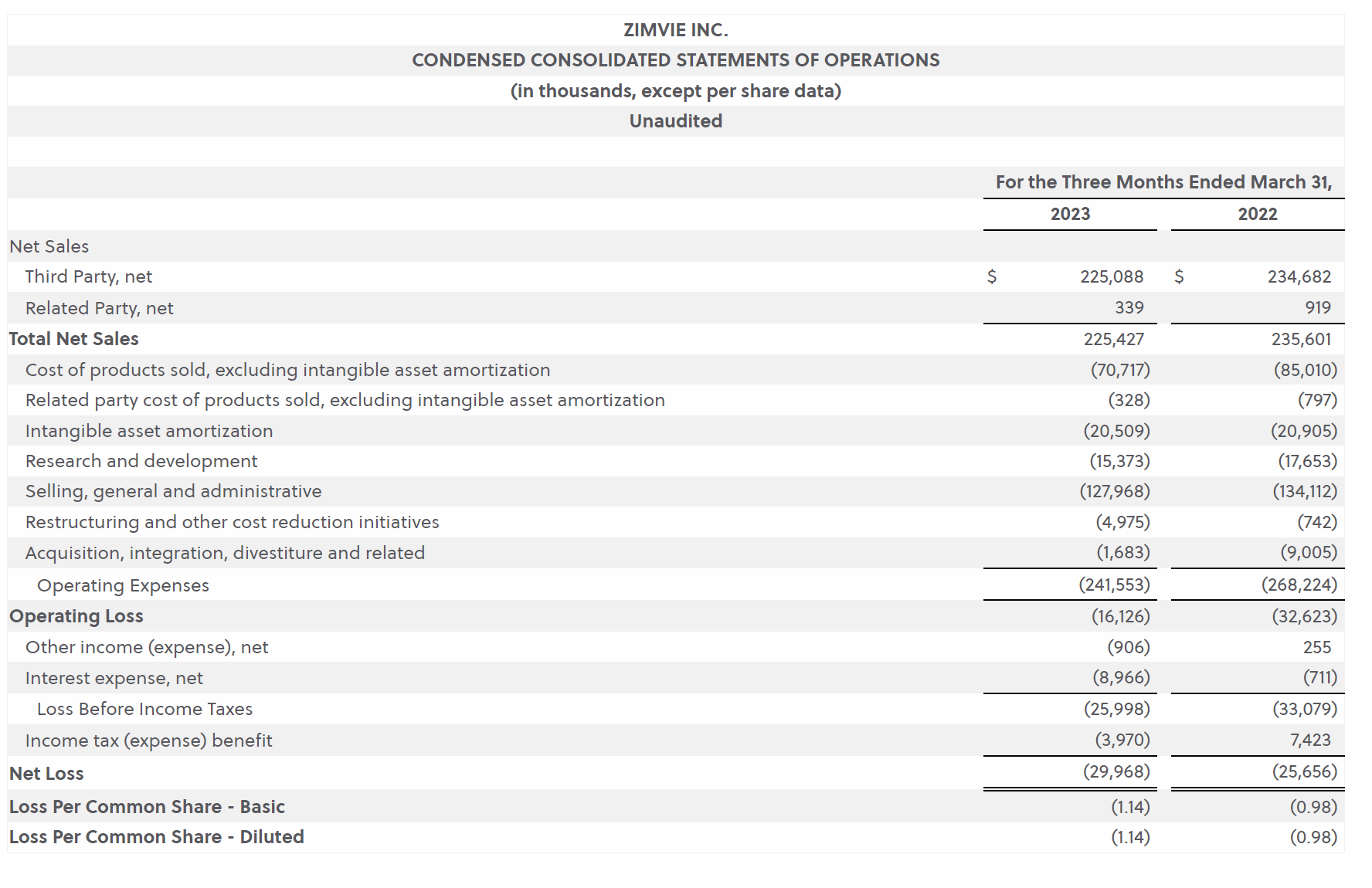

A few weeks ago, ZimVie reported Q1/23 results that came in ahead of consensus , with revenues of $225 million and adj. EPS of $0.25 compared to $207 million and $0.05 expected by analysts (Figure 5).

Figure 5 - ZIMV Q1/23 financial summary (Company press release )

{kind=link}

Importantly, while ZimVie beat consensus by $18 million in revenues and $0.20 in adj. EPS, the company only raised full year guidance by $12.5 million in revenues and $0.10 in adj. EPS (Figure 6).

Figure 6 - ZIMV updated guidance (Company press release )

{kind=link}

Management explained the difference as the company being 'conservative' due to the uncertain macro environment. As a veteran of investor conference calls and company quarterly results, I interpreted the conservatism as management trying to keep expectations low so they can continue the 'beat and raise' momentum.

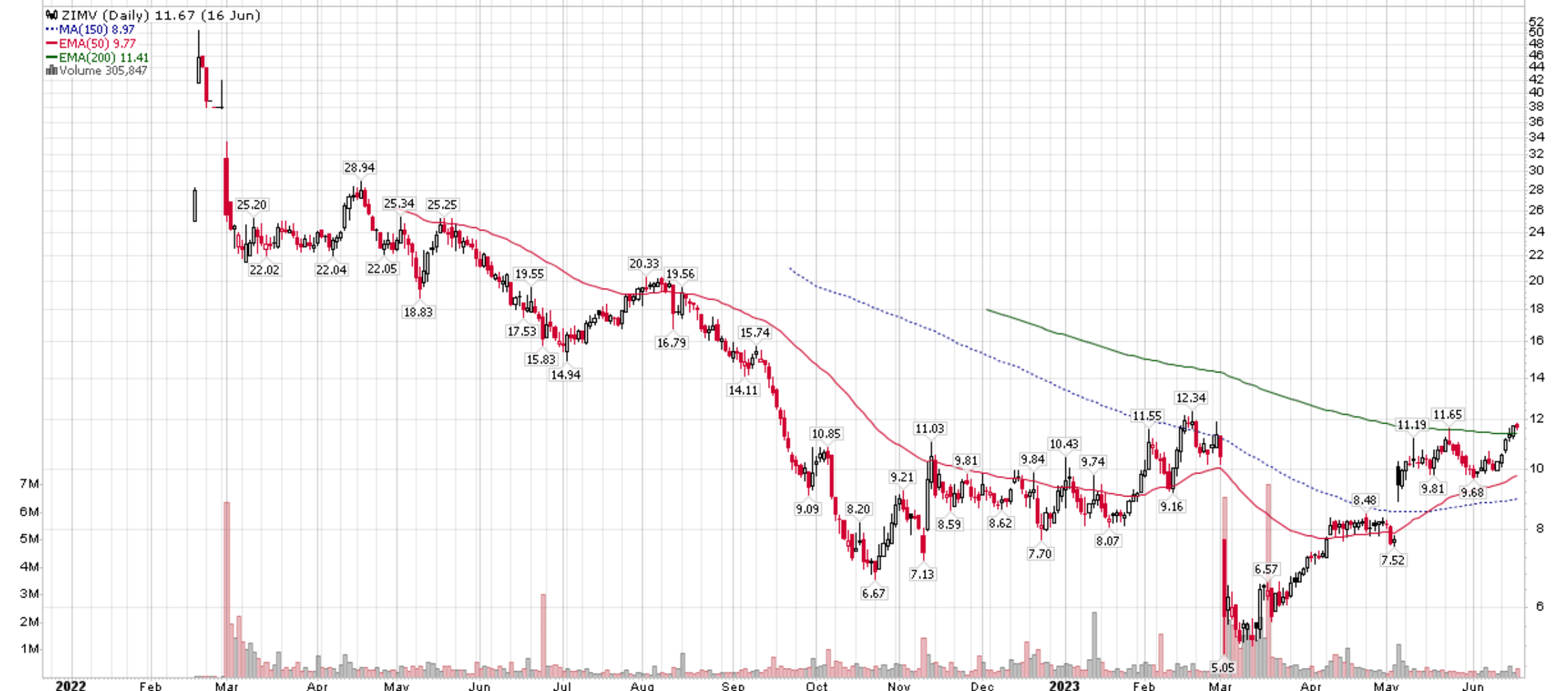

Regardless, investors appear happy with the company's performance, as the stock gapped higher on the Q1 earnings release and has now fully recovered all of the Q4/2022 earnings plunge and more (Figure 7).

Figure 7 - ZIMV stock has recovered March plunge and more (Stockcharts.com)

{kind=link}

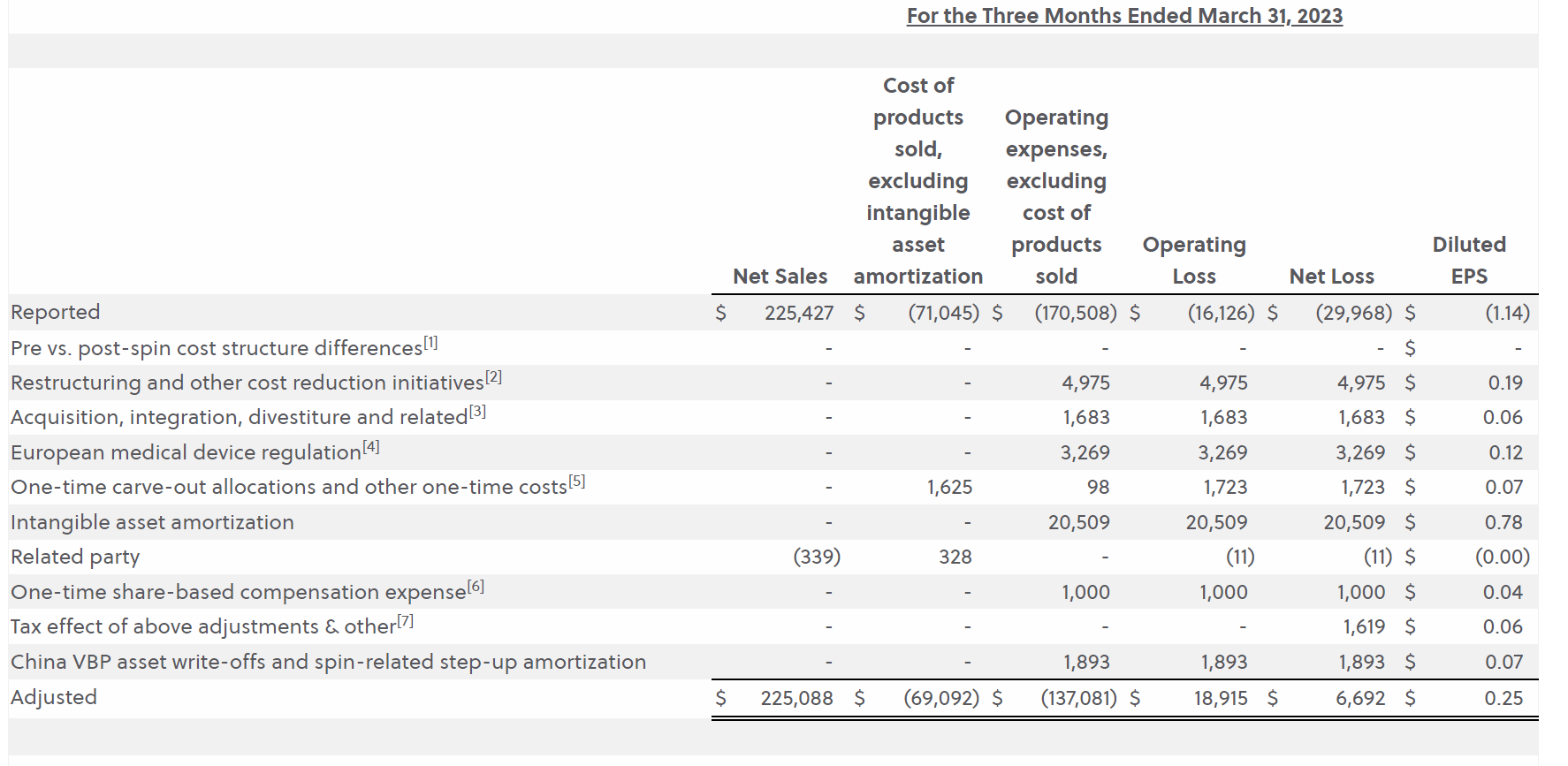

Results Continue To Be Adjusted, CFO Shows Deterioration

Although ZIMV's stock performance has improved, actual fundamentals have deteriorated. One ongoing concern I have with the company is that its financial results remain heavily 'adjusted', more than a year after it has been spun out of Zimmer Biomet. (Figure 8).

Figure 8 - Financials remain heavily adjusted a year after spin out (Company press release)

{kind=link}

At what point do restructuring costs stop being adjusted? Shouldn't 'European medical device regulation' costs be part of the costs of doing business for a global medical devices company? Doesn't intangible assets (patents, brands) lose value over time? It is very odd that the company continues to issue 'adjusted earnings' a year after the spin out and Wall Street analysts continue to give management a pass on the issue. Adjustments in Q1 were able to turn a $1.14 / share quarterly loss into a $0.25 / share adjusted gain.

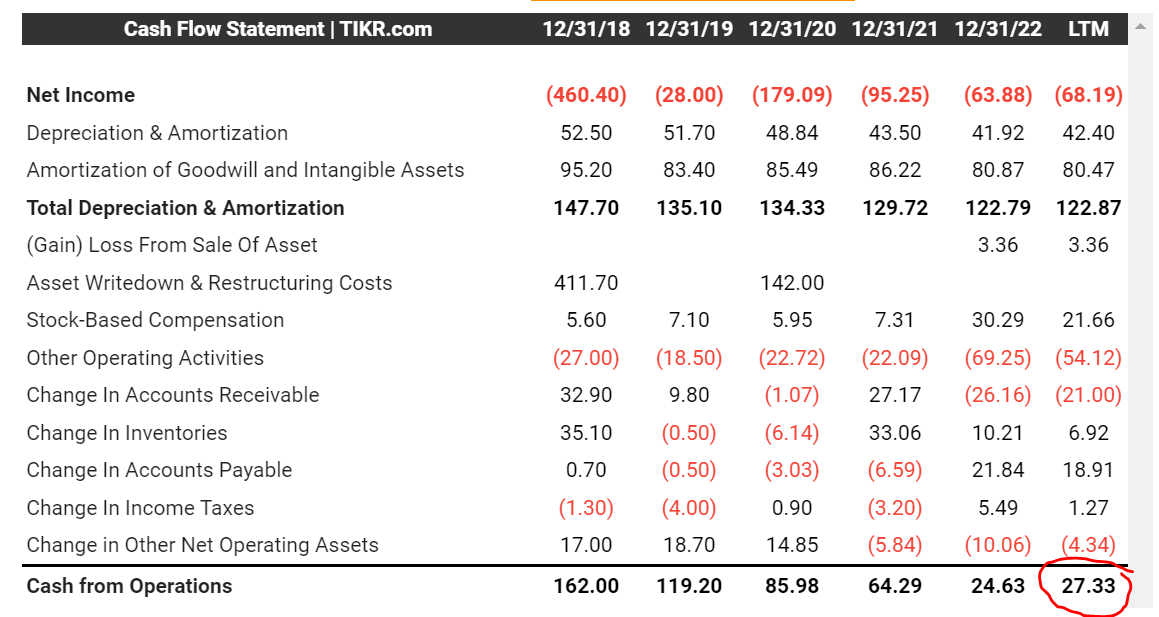

Instead of analyzing the heavily adjusted earnings figure, I continue to recommend investors look at the harder to manipulate cash flow from operations ("CFO") figure, which shows the extent of deterioration in ZIMV's businesses. ZIMV reported LTM CFO of $27.3 million as of Q1/23, less than half of the $54.9 million in LTM CFO as of Q3/22, when I last wrote about the company (Figure 9). In fact, $27.3 million in LTM CFO is less than a quarter of 2019's full year CFO of $119.2 million, showing the rapid deterioration of ZIMV's businesses.

Figure 9 - ZIMV's LTM CFO has shrunk by more than 50% (Tikr.com)

{kind=link}

Valuations No Longer 'Cheap'

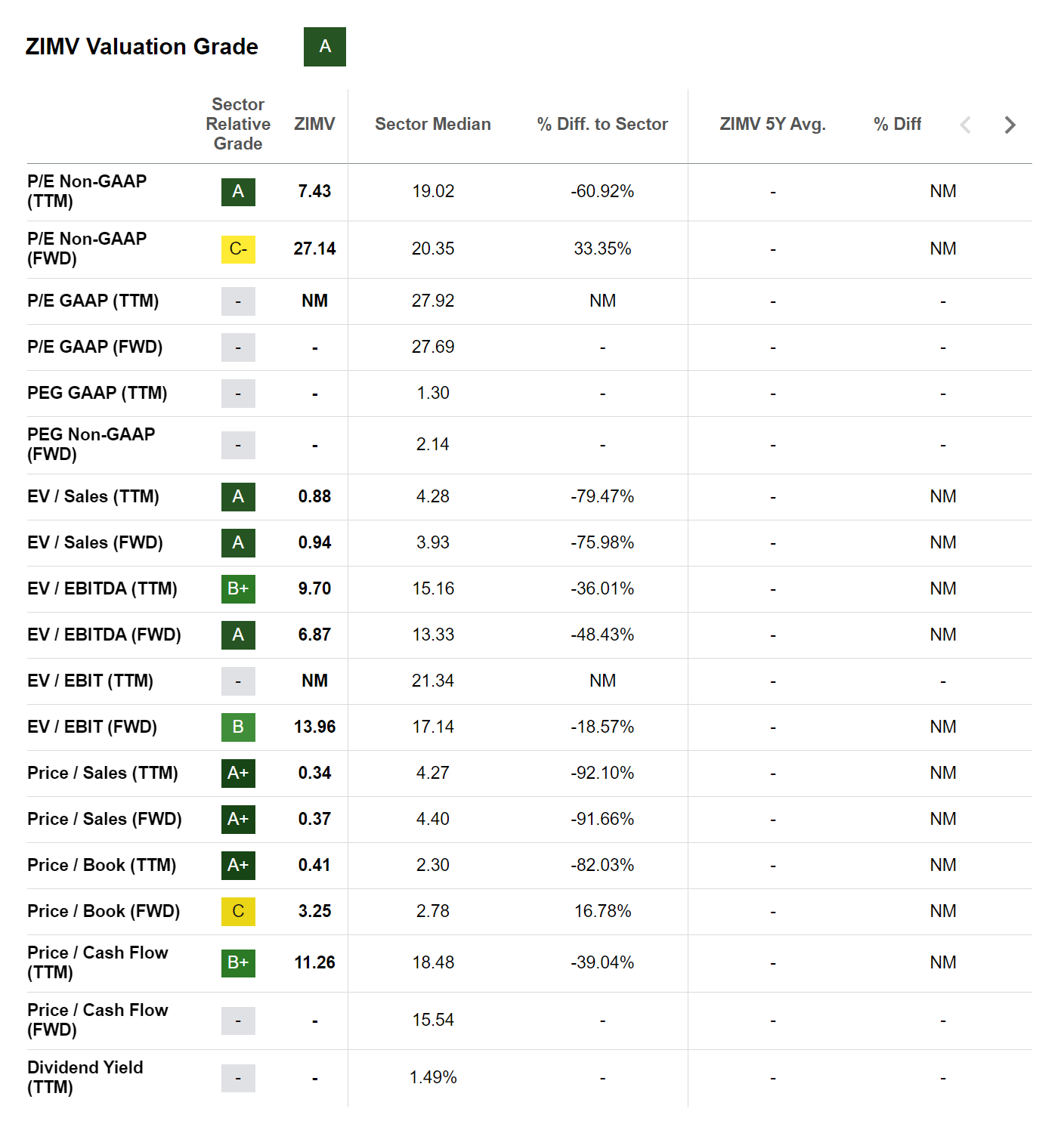

Based upon management's guidance for $0.40 - 0.60 in 'adjusted EPS' for 2023, ZIMV's shares are currently trading at 19.5x - 29.2x adj. Fwd P/E, compared to the sector median at 20.4x. Wall Street consensus is looking for $0.43 in adj. EPS or 27.1x in adj. Fwd P/E (Figure 10). Neither metric screens cheap anymore, as expectations for the business have been reset lower.

Figure 10 - ZIMV valuation (Seeking Alpha)

{kind=link}

Moreover, those valuations are based on adjusted earnings. The company is not expected to generate GAAP earnings in the near future and has not reported GAAP earnings in the prior 5 fiscal years (from figure 9 above).

On a Price-to-cashflow basis, ZimVie is also no longer dramatically cheap, as its LTM CFO has declined substantially from $54.9 million to $27.3 million, giving the company a 11.3x P/CF multiple compared to the sector median at 18.5x.

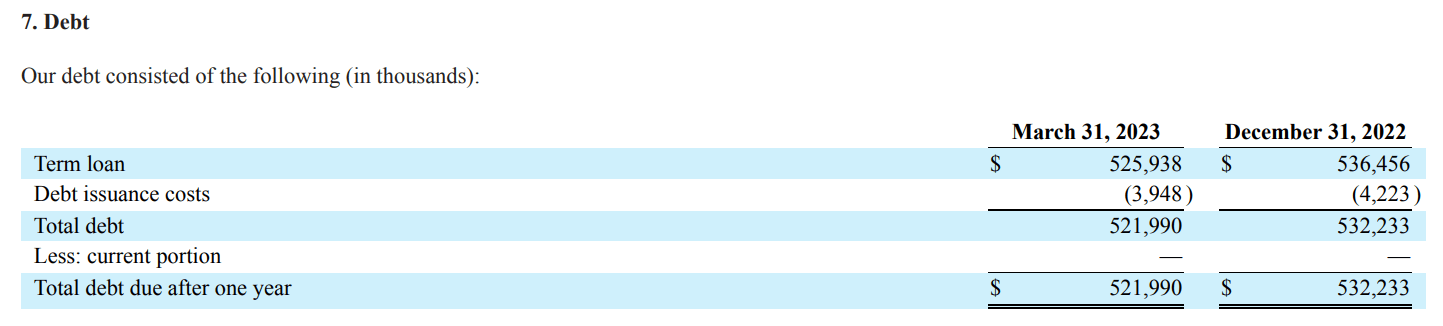

Heavy Debt Load Remains A Concern

As part of the spin-out, ZIMV was saddled with hundreds of millions in debt in order to reduce Zimmer Biomet's debt load and pay a special dividend to the parent company. Although ZimVie is currently several quarters ahead in its term loan amortization schedule, there is still $522 million in term loans outstanding (Figure 11).

Figure 11 - ZIMV's debt load remains heavy (ZIMV 10Q report)

{kind=link}

With $66 million of cash on the balance sheet, ZIMV has $456 million in net debt against management's guidance for $117 million in adj. EBITDA for 2023 ($847.5 million in midpoint revenues multiplied by 13.75% in midpoint EBITDA margin), or 3.9x Net Debt / adj. EBITDA.

Compared to my previous article from November (3.6x Net Debt / 2022 adj. EBITDA), ZIMV's leverage has actually gotten worse despite the outstanding term loan balance decreasing from $535 million to $522 million as Net Debt has increased from $438 million to $456 million and 2023E adj. EBITDA of $117 million is less than 2022's adj. EBITDA estimate of $123 million in November.

Conclusion

In conclusion, although the market has re-rated ZimVie's stock price 19% higher from my November article, the company's fundamentals have actually deteriorated significantly. ZIMV's revenue guidance for 2023 is currently set at $848 million, a 6.7% decline from 2022's $909 million in external 3rd party sales. LTM CFO has been cut in half from $55 million in Q3/22 to $27 million in Q1/23. Finally, Fwd Net Debt / adj. EBITDA has deteriorated from 3.6x to 3.9x.

Based on the company's 2023 adj. EPS guidance midpoint of $0.50, the company is currently trading at 23.3x adj. Fwd P/E, a premium compared to the sector median of 20.4x.

With deteriorating fundamentals and higher valuations, I am lowering my rating on ZIMV to a hold . Current shareholders may wish to reduce their holdings and investors on the sideline should wait for a better valuation (either a decline in price or an improvement in fundamentals) before they consider opening a position in the shares of ZimVie.

For further details see:

ZimVie: Downgrade To A Hold On Valuation And Fundamentals