CA - Zomedica: High Risk High Reward Play In Veterinary Supplies

Summary

- Shares in Zomedica jumped on analyst coverage with $6.00 price target.

- Its buy and build strategy is highly appealing.

- Zomedica has a daunting risk profile.

This is my second look at Zomedica ( ZOM ) following 09/2022's " Zomedica: Growing Veterinary Supply Company, Building Big Things On The Come " ("Big Things"). I remain optimistic about this company despite its many risks.

On the morning of 01/06/2023 Zomedica shareholders got a flash of good news

Zomedica shares trade like Peter Pan's Tinker Bell; they flit up and down. Unfortunately for those shareholders looking for growth, they have shown a recent predilection for the downward flit.

Big Things was published on 9/12/2022. Zomedica opened that morning at $0.2490 and closed that evening at $0.2480 on moderate volume of ~9.3 million shares; it showed minuscule peak to trough movement on the day.

As shown by its price chart below it has done heavy duty flitting over the last year with three noble, albeit short-lived assaults >$0.40.

It has fallen back recently spending much of the Christmas season <$0.20, trading down as low as ~$0.15. it had slowly made its way back up to $0.1920 where it closed on 01/05/2023.

Today (01/06/2023) as I write, it opened strong at $0.2450, jumping to high of $0.2950 after closing the previous day at $0.1920. Unlike previous moves its move on 01/06/2022 was clearly traceable to an analyst call; Dawson James' initiated coverage with a buy recommendation and a price target of $6.00. My thanks to excenter for his Big Things comment alerting me to the analyst action.

Zomedica has an attractive business plan and nice liquidity with which to implement it

Zomedica is still a young company founded in 2015. It is still getting its sea legs. In common with a number of similarly situated companies it does not participate in quarterly earnings calls. As a significantly less useful substitute it does present at diverse investor's conferences, as for example the Dawson James conference referenced above.

The latest (11/29/22) such on its website is "Zomedica CEO Interview with Wall Street Analyzer Updates Company Progress and Plans" (the "Interview"). It featured CEO Heaton providing an overview description of Zomedica. Its overriding goal is to provide economic benefits for veterinarians. It does so by providing tools to improving the quality of care for their pet patients thereby increasing the satisfaction of the pet parents.

Zomedica currently markets products in both diagnostics and therapeutics. He described its diagnostics offering as its:

TRUFORMA system that can provide a diagnostic result within about 20 minutes. We offer the instrument to the clinic with no capital outlay required through our customer appreciation program, and they purchase the individual assay cartridges to run the tests.

The diagnostics system includes:

...six assays, four of which represent the only test of their type available at the point of care; so highly differentiated.

Zomedica intends to expand the available assays for its diagnostics system on an ongoing basis, starting with the equine market.

On the therapeutic side, Zomedica acquired PulseVet in 10/2021. Heaton characterized PulseVet as the worldwide market leader in shockwave therapy for horses. The treatment promotes rapid post surgical healing, addresses lameness, soreness, tendon injuries, osteoarthritis.

Subsequently Zomedica has launched an accessory product that makes the treatment applicable to the small animal market. It has been introducing this product to small animal veterinarians during the course of the year. The market for small animals is 15 to 20 times the size of the equine market.

In 07/2022 Zomedica closed on two additional deals:

- Its acquisition of Revo Squared adding MicroView digital cytology platform to Zomedica's diagnostics capabilities to provide veterinarians with best-in-class image quality while providing the first in-clinic automated slide preparation system the system improves practice workflow efficiency by automating the process to assure a consistent smear and stain to produce a readable slide; and

- its acquisition of the bulk of the assets of Assisi Animal Health expanding its therapeutics business with Assisi's Pulsed Electromagnetic Field (tPEMF™) devices for companion animals that provide a safe, drug-free alternative for treating pain, inflammation, anxiety, or behavioral disorders.

Shortly thereafter in 08/2022, Zomedica finished the build-out and moved into its expanded 12,400 square foot global manufacturing and distribution center in Roswell, Georgia. Over time all manufacturing and distribution will be located there, which will allow it to further reduce costs and improve margins.

Despite its heavy lifting in building its business, Zomedica closed Q3, 2022 with a nice liquidity in cash, cash equivalents, and available for sale securities of $158.49 million. Zomedica reported 3 and 9 month R&D expenses of $1.13 million and $1.60 million respectively. It reported 3 and 9 month SG&A expenses of $9.02 million and $24.34 million.

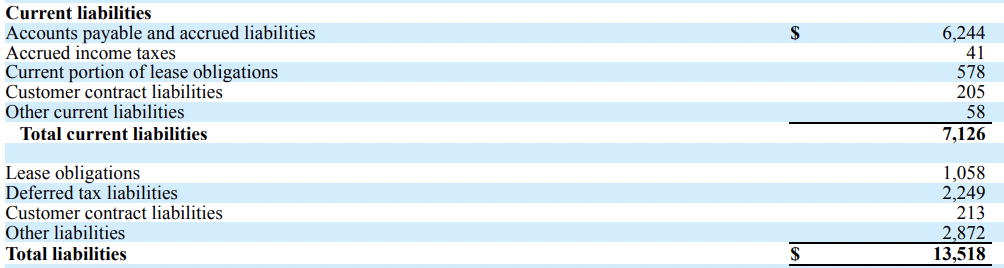

Zomedica's Q3, 2022 10-Q lists only a modest slate of liabilities as follows:

{kind=link}

Zomedica has avoided debt financing. It has effectively used equity and equity related securities and the exercise of stock options and warrants to fund its operations. Indeed its accumulated deficit over its ~7 years of operations amounts to a modest $0.133 billion. Its market cap as I write on 01/08/2023 is ~$229 million.

Despite its attractions, Zomedica is a high risk proposition

As I write this article and ponder on Zomedica's forward prospects, I am still smarting from AEMAD 's terse comment to "Big Things" . As he put it:

AEMAD

Well...the name of author of this article pretty much sums up why you would buy this stock...

At this point I will repeat the closing paragraph from Big Things which remains true today as it did when written:

There can be no doubt that it is highly speculative. None of its businesses has a proven track record, some have no record at all. The one record that is clear is that it currently generates losses and it expects to do so for the foreseeable future.

Zomedica's Q3, 2022 10-Q set out its long range cash requirements at p. 31. its current liquidity should be sufficient through at least 12/2024, it also notes that its business plan is in a constant state of review and flux.

Any such change puts its current shareholders at risk of substantial dilution. Also revisions could result in debt financing with potentially toxic restrictive covenants. In other words today's comfortable financial profile could give way to uncomfortable exigencies tomorrow.

What are the chances of such an awkward turn? They are clearly higher than a Zomedica bull would hope. Zomedica's Q3 release listed revenues of $4.78 million:

...which reflects an approximate 24% increase in the sales of our pre-existing PulseVet ® and TRUFORMA ® products over 2021 levels; and a 17% increase, on a pro-forma basis, over the combined revenue of Zomedica, Pulse Veterinary Technologies ("PulseVet"), and Assisi Animal Health ("Assisi") as standalone companies, of $4.10 million from the same period in 2021.

Such a result causes me to question management's promotional verve. In that regard consider this quote from the Interview where CEO Heaton stated:

So through the first three quarters of the year, our total revenue is up 24,515% as we have grown both our TRUFORMA and PulseVet revenue significantly. TRUFORMA is up 365% versus 2021, and PulseVet is up 35% versus their 2021 sales as a standalone company. So we are truly growing revenue.

Now I am not suggesting that the CEO's above statement is untrue. I am saying, at best, it cherry picks its data.

In order for Zomedica to grow into its potential. it is going to need to keep acquiring more companies. Each time it does so it takes a risk that it overpay or otherwise misjudge the situation. While it has comfortable resources it lacks the bulk that would allow it to easily recover from such a miscue.

Conclusion

Zomedica is a tiny player in an attractive market. So far it has positioned itself well. If its business continues over the next 7 years as it has over the last seven, its investors should thrive.

So far it has essentially pulled itself up from nothing to an operating business with:

- four attractive, albeit unproven assets;

- liquidity >$100 million;

- debt free balance sheet.

Zomedica's management has done admirably so far, albeit more promotional than I prefer. At its current market cap, I continue to consider it a strong buy.

For further details see:

Zomedica: High Risk High Reward Play In Veterinary Supplies