ZI - ZoomInfo: AI Investment Amid Market Challenges And Valuation Considerations

2023-11-04 03:08:30 ET

Summary

- ZoomInfo Technologies provides a go-to-market intelligence platform, showing strong historical and current financial performance.

- The company's growth is decelerating, but it maintains positive net income and is investing in AI to combat market challenges.

- I recommend a hold rating due to the modest upside potential.

Summary

ZoomInfo Technologies, Inc. ( ZI ) is a software company that provides go-to-market intelligence platform for its customers. This platform aims to equip teams with data on organizations and individuals so that it helps them in areas such as identifying target audiences, sales, and marketing. I recommend a hold rating for ZI. Although they have shown strong historical and current financial performance, they do face some challenges now. Based on the weak growth outlook and modest upside potential, I recommend a hold rating for ZI at this moment.

Financials

Over the past four years, ZI has demonstrated consistent growth, but it is decelerating. In 2019, it was 103%, but in 2022, it dropped to 46%. However, growth was still at high double-digit rates, and it has a CAGR of 50%. These results underscore the effectiveness of its business model and suggest that its products and services resonate well with its customers. When it comes to profitability, ZI has maintained a positive net income since 2021, setting them apart from many of its peers, most of whom still report negative net income.

Valuation

Based on my view of the business, I anticipate a 12% growth in ZI’s revenue for FY23, followed by 4% revenue for FY24. This growth outlook aligns with the general market consensus. The decelerating growth outlook is influenced by the following factors. Although ZI posted both strong current and past revenue growth rates, it has been decelerating, and I expect this trend to carry forward into the future. During the earnings call, management also highlighted that they are currently facing headwinds such as lower upsells and an increase in churn. However, this trend is not just specific to ZI but to the overall market. This suggests that the entire market is facing headwinds, which I anticipate will decelerate ZI’s future growth. In a bid to combat this market challenge, ZI is investing onto AI and also partnering with big players such as Google. I expect this initiative to offset of the weakness it is currently facing.

Based on author's own math

Peers overview:

{kind=link}

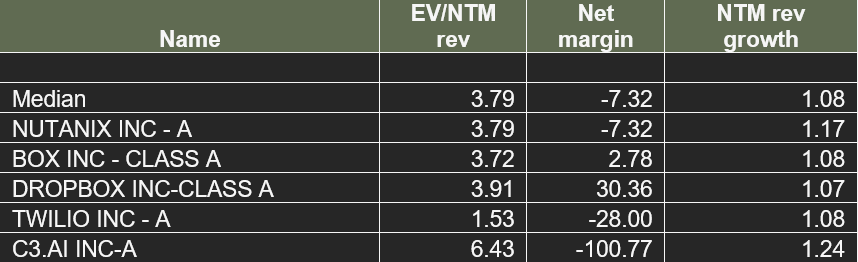

Currently, ZI is trading at a forward revenue multiple of 4.7x, which is notably higher than the peer median of 3.8x. This premium is justified by ZI's superior net margin and promising growth outlook. Specifically, ZI boasts a net margin of 7%, in stark contrast to the peer median which stands at a negative 7%. Furthermore, ZI's projected growth rate for the upcoming year is 12%, outpacing the peer median of 8%. With a forward revenue multiple of 4.7x, my valuation places ZI's price at $13.16, a mere 5% increase from its recent trading price. The broader market has already factored in ZI's strengths into its current valuation. Given these considerations, my recommendation for ZI is a hold now.

Comments

In the third quarter of 2023, ZI reported revenue of $314 million, a year-over-year growth of 9% which in my opinion is impressive given the challenging market condition. Its adjusted operating income was $126 million. Its non-GAAP EPS was $0.26, which is the same as the previous quarter. This suggests that net income margins contracted slightly as revenue growth outpaced EPS growth.

In the earnings call, ZI’s management emphasized that they are prioritizing AI investments so that it can be integrated into their existing products to upgrade it. Due to this investment, ZI has seen a rise of 22 points in the Net Promoter Score [NPS] for Chorus year over year and an increase of over 20% in overall product engagement. NPS measures customer loyalty, and I believe that this investment is going to improve on its high churn rate.

In addition to investing in AI, ZI also integrated with Google Analytics Hub to give data science teams access to ZoomInfo insights and models within Google's BigQuery. This allows businesses to make better decisions in less time and with fewer resources spent on implementing AI projects. Overall, I believe ZI’s investment is well spent and is expected to produce positive results for them.

However, it is not all good news. During the quarter, fewer up-sells, more seat down-sells, and increased churn have all been highlighted as difficulties faced by ZI. This challenge started since the beginning of the year. Net revenue retention and overall growth rates have decreased for ZI as their customers have had to rebalance growth and profitability. This is not an issue exclusive to ZI but rather a market phenomenon affecting businesses using any variety of front-end software. Management also stated once this cycle ends and return to a more normalized operating environment, they will be ready to capture the recovery. From this, I infer that this issue is not just contained within this quarter but might be carried into the next year.

In response to the prevailing challenges, ZI emphasized its commitment to controlling what is within its reach. ZI is committed to maximizing its controllables and delivering industry-leading levels of profitability in the current operating environment, all while investing in the long-term success of its customers and the growth of the company. In order to achieve this goal, ZI is putting an increased emphasis on product quality and customer satisfaction by accelerating time to value and enhancing user friendliness, which has led to an increase in product engagement. Overall, it seems like management is not fazed by the challenges. In fact, they are embracing it and preparing themselves well for the future to ensure that revenue continues to growth and margin will not be sacrificed for just top line revenue growth.

Risk & conclusion

One risk for ZI is the competitive nature of its industry. As technology evolves, there will be an increase in the number of new entrants. On top of that, established players will also step up their innovations. These could lead to an increase in competition for ZI and put pressure on its profit and revenue, as ZI would have to increase R&D in order to compete and hold its market share.

In conclusion, ZI has shown strong past and current financial performance. However, it does come with its own set of challenges, such as fewer up-sells, more seat down-sells, and increased churn. This challenging environment is not an issue exclusive to ZI but rather a market phenomenon. In response, ZI is actively prioritizing AI investments that are bearing results. However, its growth outlook remains bleak, with an anticipation of a deceleration in growth rates for future years. With these factors in mind and a modest upside potential, I recommend a hold rating for ZI at this moment.

For further details see:

ZoomInfo: AI Investment Amid Market Challenges And Valuation Considerations