ZI - ZoomInfo: No Catalysts For Recovery

2023-12-20 14:54:30 ET

Summary

- ZoomInfo's share price has collapsed nearly 40% this year, missing out on the rally in the S&P 500 and other software companies.

- The company's Q3 earnings showed a deceleration in revenue and a reduction in operating margins.

- ZoomInfo faces challenges in its top line growth, stiff competition from larger CRM-style products, and a large debt load.

- Despite deteriorating fundamentals, the stock remains expensive at ~6x revenue.

It's hardly a secret this year that perhaps more than any other profession, salespeople have borne the brunt of corporate layoffs as companies looked to slash opex and realign their workforces to lower demand. And within the tech sector, few companies have suffered from that realignment more than ZoomInfo Technologies Inc. ( ZI ) has.

This sales software company, a virtual "Yellow Pages" of sorts for sales and marketing departments primarily in the tech sector, has seen its share price collapse nearly 40% year to date, missing out on the broad rally in the S&P 500 and among fellow software companies. Still, I think there's further downside to go.

Despite glaring weaknesses, ZoomInfo isn't even cheap

I last wrote a bearish article on ZoomInfo in August, when the stock was trading closer to $19 per share. Since then, ZoomInfo has published an even more disappointing Q3 earnings print that showed both a deceleration in revenue and a slight reduction in operating margins.

Despite the sharp challenges that ZoomInfo faces to its top line, the company has been relatively conservative in resizing its expense base. It did do a round of layoffs, but at only ~120 heads and ~3% of the company's workforce , I'd argue that ZoomInfo's cost cuts are far more benign than that of some of its peers, despite the fact that ZoomInfo is ostensibly facing sharper macro challenges than other software companies.

All in all, I remain quite bearish on ZoomInfo's prospects - especially as profitability wanes and accentuates its debt load. As a reminder for investors who are newer to this stock, here is what I view to be the longer-term bear case for ZoomInfo:

- Slowing growth exposes a very lumpy business: Consensus is expecting ZoomInfo's growth to fall to the single digits in FY24. After dramatically rising in the pandemic, ZoomInfo's growth has decelerated sharply - exhibiting a lumpy growth trend versus the more stable growth patterns that mature, higher-quality software companies have been able to manage.

- Stiff competition: ZoomInfo is one of many CRM-style products and competes with much more recognizable names such as Microsoft Corporation's ( MSFT ) LinkedIn and Salesforce, Inc. ( CRM ). These competitors also have the capability to cross-sell CRM solutions with other platform products, while ZoomInfo stands alone as its own solution. In an environment where many IT departments are trying to consolidate vendors and limit budgets, this may hurt ZoomInfo more than in the pre-pandemic period.

- Large debt load: Unlike many tech peers, ZoomInfo is in a net debt position, and its floating debt structure exposes it to high interest costs.

- Not making progress on profitability: Despite a slowdown in growth rates, ZoomInfo has not made much headway in turning its focus to improving operating margins - despite laying off ~120 employees earlier this year.

Perhaps even worse is the fact that in spite of decaying trends plus longer-term risks, ZoomInfo still isn't cheap - in other words, the stock remains quite dislocated above its fundamental value, in my opinion. And even the recent downside since the start of the year hasn't fully corrected this problem.

At current share prices near $18, ZoomInfo trades at a market cap of $7.01 billion. After we net off the $567.9 million of cash and $1.23 billion of debt on ZoomInfo's most recent balance sheet, the company's resulting enterprise value is $7.67 billion.

Meanwhile, for the next fiscal year, FY24, Wall Street analysts are expecting ZoomInfo to generate $1.28 billion in revenue, up 3% y/y and basically indicating a lack of confidence in ZoomInfo's ability to stage a fundamental rebound. Against this outlook, the stock trades at 6.0x EV/FY24 revenue - richer than many software companies that are expected to grow at a double-digit pace next year.

As such, I don't see any incentive at all to be invested in this stock. Steer clear here and invest elsewhere.

Q3 download

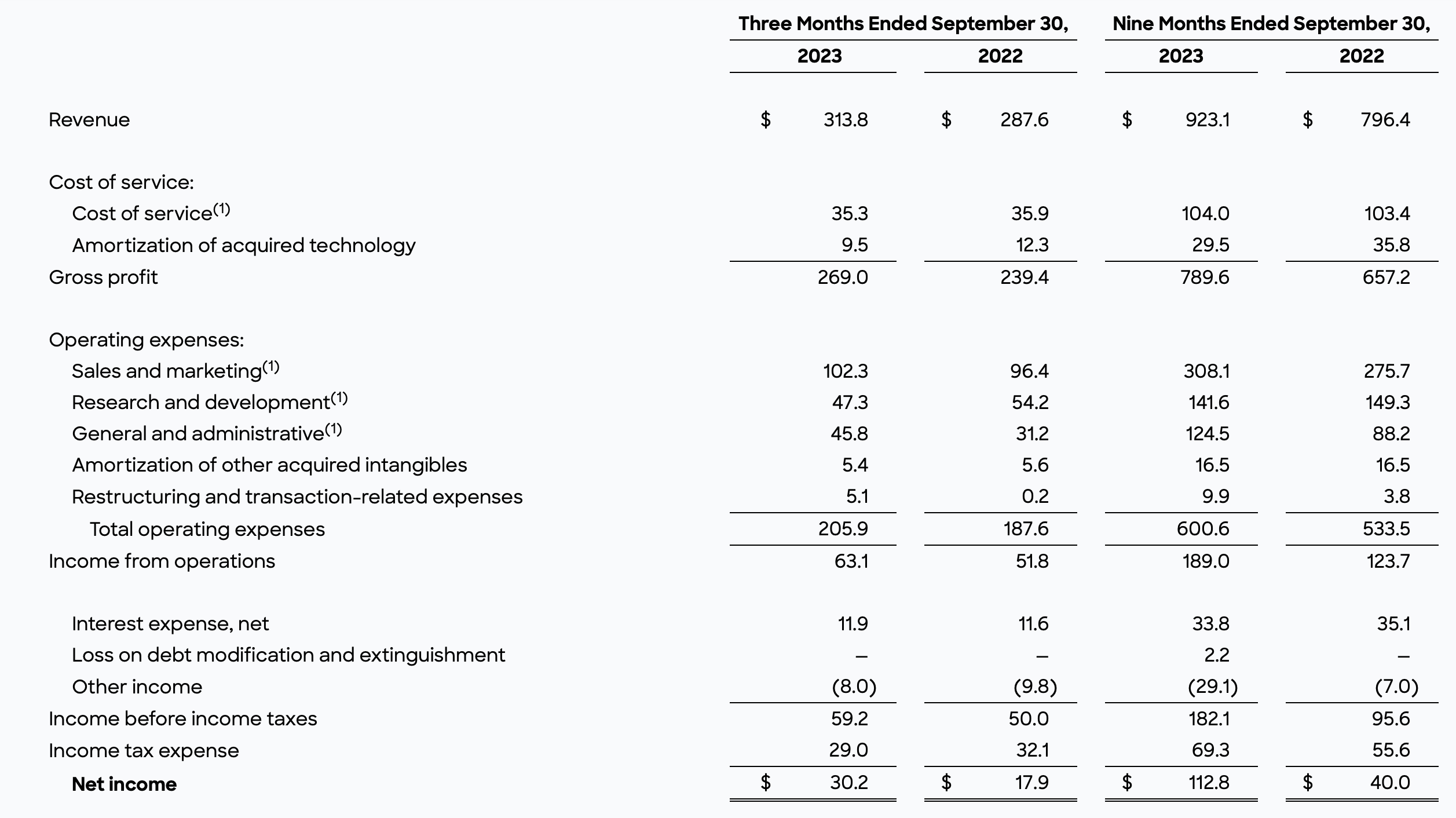

Let's now go through ZoomInfo's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

ZoomInfo's revenue grew just 9% y/y to $313.9 million, slightly ahead of Wall Street's expectations of $310.5 million (+8% y/y). Growth decelerated sharply from 16% y/y in Q2, a product of difficult macro constraints on software companies that serve front-office, sales and marketing-oriented products.

Still - we can't ignore the fact that some of ZoomInfo's most notable competitors are arguably navigating the situation a lot more smoothly than ZoomInfo is. Notably, Salesforce.com has soared to new all-time highs on much stronger-than-expected results. To me, this is one of several indications that amid a tighter budget environment, more IT spending is going to the larger "portfolio software" companies - winner-take-all, essentially.

Here is additional commentary from CEO Henry Schuck's remarks on the Q3 earnings call , detailing the company's sales situation and its priorities for navigating it:

Since early last year, we have highlighted the challenges of this operating environment, which include fewer up-sells, more seat down-sells, and elevated churn levels. As a platform that helps customers grow and one that serves some early-cycle industries, we have seen net revenue retention and our overall growth rates come down, as customers have had to rebalance growth and profitability.

This is a market phenomenon impacting companies across the spectrum of front-office applications and is not unique to ZoomInfo. When the cycle ends and we are in a more normalized operating environment, companies will be looking to drive growth and we will continue to be uniquely positioned to help them do just that. In this operating environment, we are committed to controlling the controllable and delivering industry-leading levels of profitability, while we invest in our customers' success and improve the Company for the long term.

To that end, we are doubling down on product excellence and customer success, investing in improved ease of use and driving quicker time to value for our customers. These investments have driven a 20% increase in product engagement since the beginning of the year. Customers are using more of the platform more often. We are doing this while prioritizing investments in AI, data-as-a-service, and marketing OS, and building our industry-leading data coverage and accuracy across the globe. We've rolled out new pricing and packaging at the low end of the market, enabling us to capture more of the market efficiently, while simultaneously growing our contributors. And we announced a number of leadership changes that have flattened the organization and given me the opportunity to get closer to our customers and how we win them, serve them, and grow them."

With challenges in closing deals at the high end of the market, the company has also rolled out additional self-service e-commerce tools for small and lower middle-market customers, in an attempt to close more "free" deals that don't require sales support.

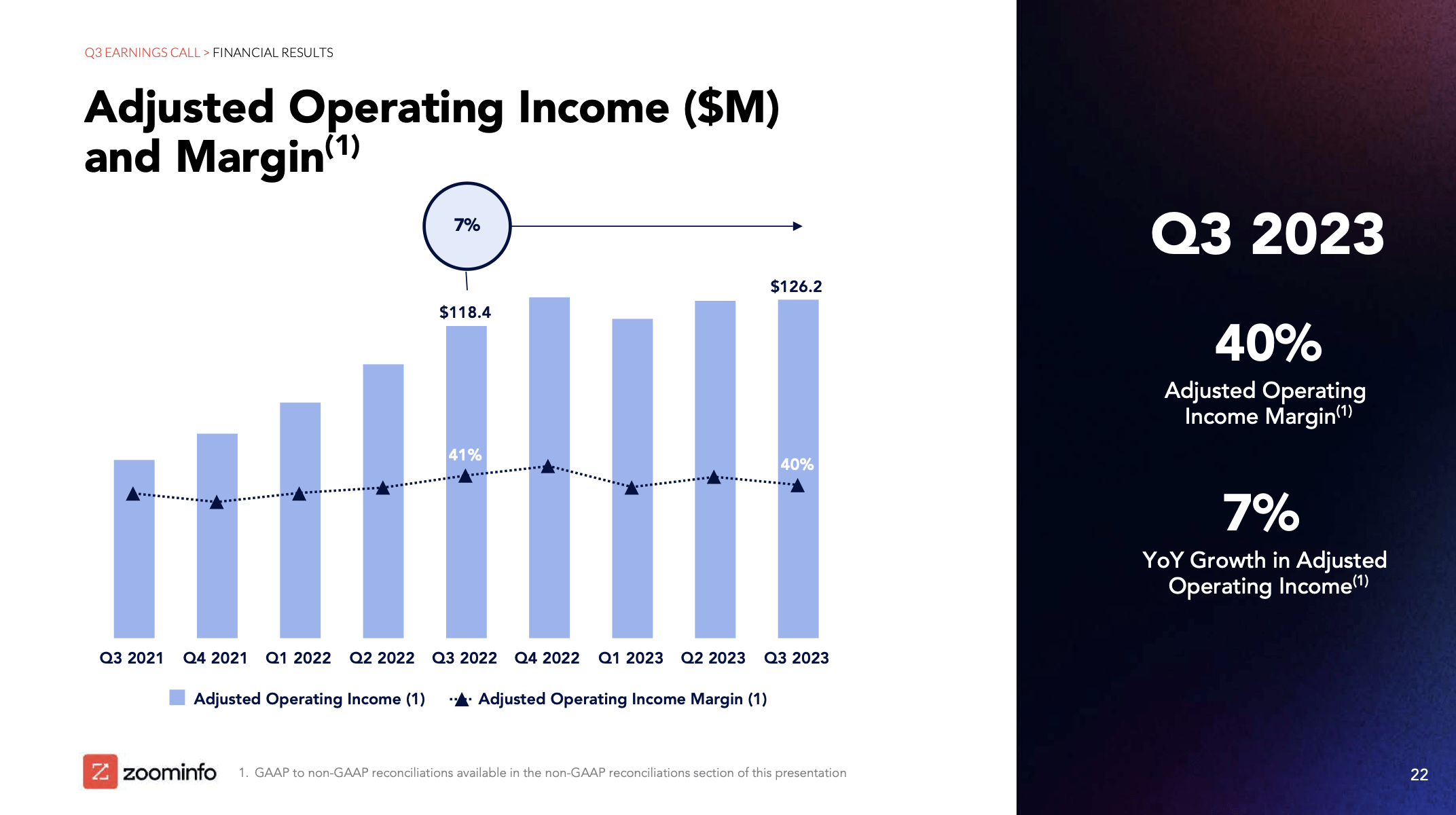

Unfortunately, even amid growth slowing down, ZoomInfo has not been able to raise its profitability profile. Adjusted operating margins shed 1% to 40% in Q3, making for just 7% y/y growth in adjusted operating income.

ZoomInfo adjusted operating margins (ZoomInfo Q3 earnings release)

{kind=link}

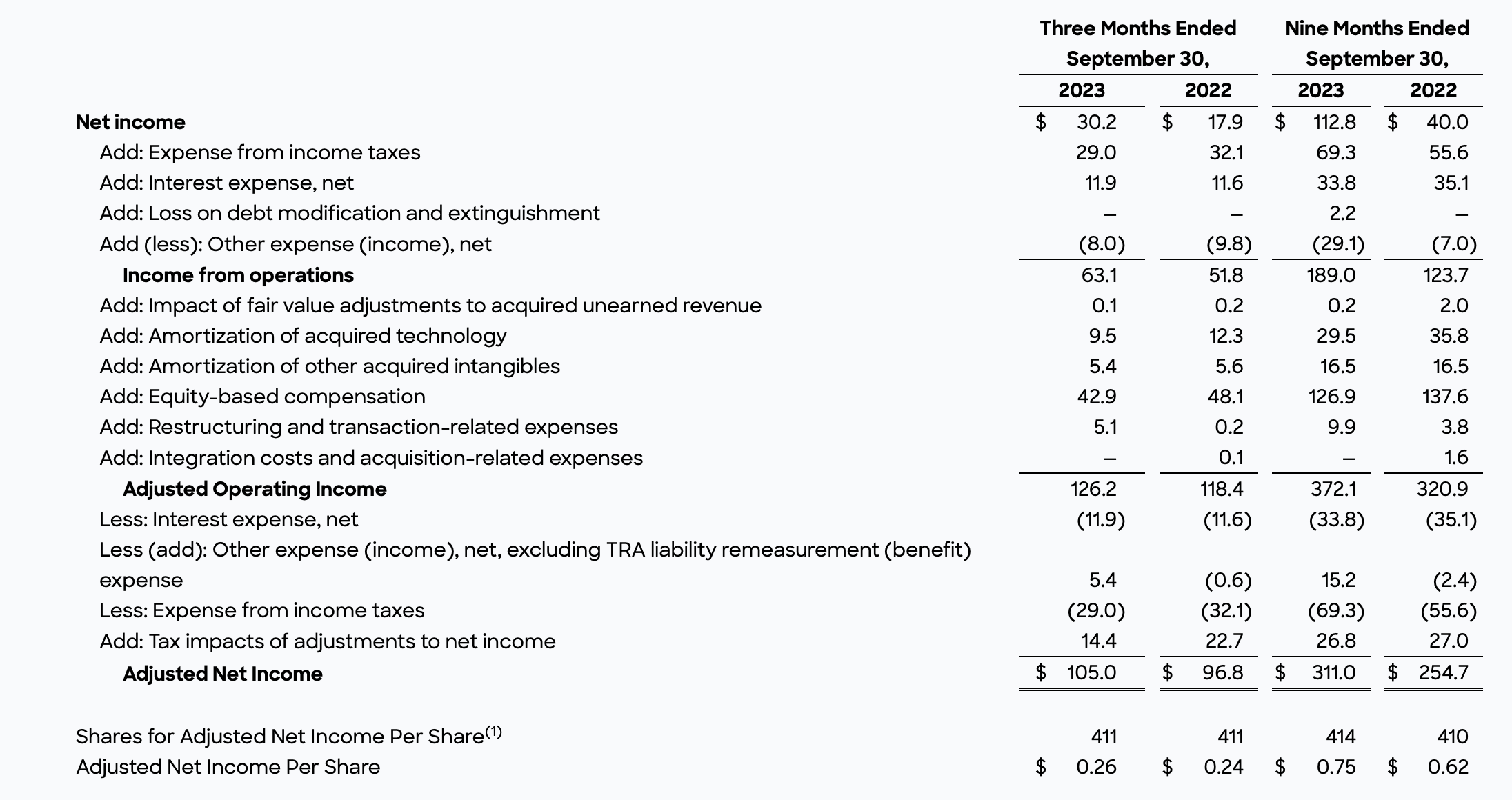

Note in the first place that ZoomInfo has quite hefty non-standard add backs to arrive at adjusted operating and net income. Note that the company added $63 million (worth 20 margin points alone!) to adjust the fair value of deferred revenue.

{kind=link}

With this in mind, plus a 14% margin worth of adjustments for stock-based compensation, I wouldn't buy into ZoomInfo's 40% "adjusted operating margin" as truly being much better than peer software companies (where a 0-10% pro forma operating margin is more common for companies of ZoomInfo's rough scale).

Key takeaways

In my view, there is more risk than reward to investing in ZoomInfo at current levels. Not only is growth decelerating and margins contracting, but the stock also remains unbearably expensive for softening fundamentals - and in a tough macro for sales-oriented software products, too. Continue to avoid this name.

For further details see:

ZoomInfo: No Catalysts For Recovery