ZS - ZScaler Q1 - Still BUY: Outperformance In 2024

2023-12-01 16:09:00 ET

Summary

- We remain buy-rated on Zscaler, Inc.

- We expect ZS to continue outperforming in 2024 despite a weaker near-term outlook on billings.

- We think it's only prudent that ZS management is more conservative in its outlook considering the current macro reality.

- We expect ZS to continue to gain cybersecurity spend wallet share as more customers' workloads move to the cloud.

- We continue to recommend investors buy the stock opportunistically.

We maintain our buy-rating on ZScaler ( ZS ) p ost- 1Q24 earning results . We think the 1Q24 results underscore the company's unique cloud security architecture and growth trajectory for FY24. We're not too worried about the more conservative billings outlook of ~4% of billings growth upside, and neither is the market; the stock erased all of its pre-market losses and was hovering at the flat line on Tuesday. We think management is setting a "prudent bar" or giving itself room to be vulnerable to macro uncertainty with the current guidance. We think this is a classic buy the rumor, sell the news action play; in our opinion, it works in Zscaler's favor to have a more conservative billings outlook and outperform their guidance.

The stock outperformed the S&P 500 by 18% since our last note from mid-September; our bullish sentiment was due to our belief that Zscaler is more resilient due to its unique position to benefit from the industry-wide shift towards new architecture in the zero-trust market. We think we're seeing our positive thesis play out into 2024 with investor confidence in the company's products reaching new highs. We understand that cybersecurity stocks are more resilient than the rest of the software sector, but we don't think they're entirely immune to macro downturns; we saw this play out earlier this year with Fortinet ( FTNT ). Fortinet stock dropped +14% after lowering its FY sales outlook due to macro headwinds amid reporting 2Q23 earning results, and the cybersecurity peer group traded lower in response. We're updating our thoughts on Zscaler in light of earning results and outlook; our research leads us to believe Zscaler will see a more positive growth narrative playing out through 2024

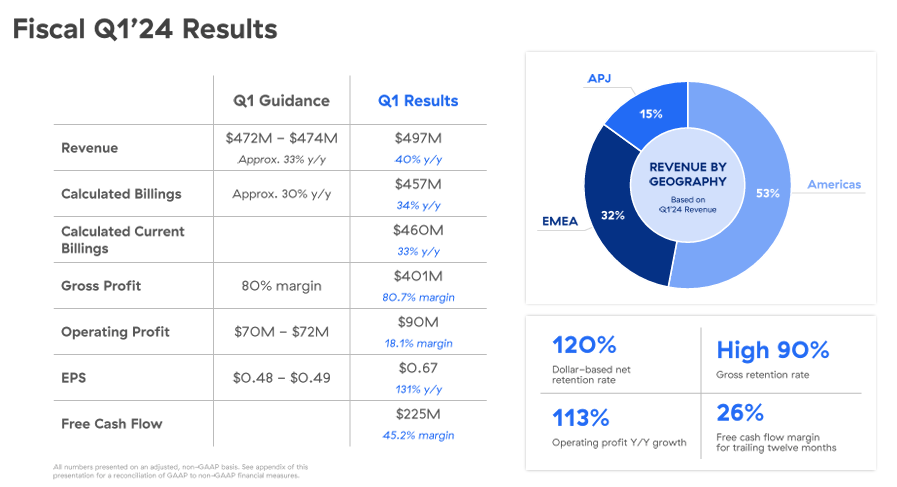

Zscaler reported 1Q24 earning results late last month, on November 27th. For the quarter, Zscaler reported revenue up 40% Y/Y to $497M. The company's calculated billings grew by 34% Y/Y to $457M, and deferred revenue was $1,399M, representing a 39% Y/Y growth. We expect the company to continue to report high double-digit top-line growth through 2024 as enterprise spending improves and cybersecurity remains a top IT spending priority.

We also think Zscaler is uniquely positioned to expand its market share, with its product portfolio at the intersection of AI and Zero-Trust. We believe the Zero-Trust market is still in its early innings and see room for Zscaler to lead the way through its Zero-Trust architecture and protecting cloud workloads.

The below figure summarizes ZS's 1Q24 results.

{kind=link}

1Q24 earning results

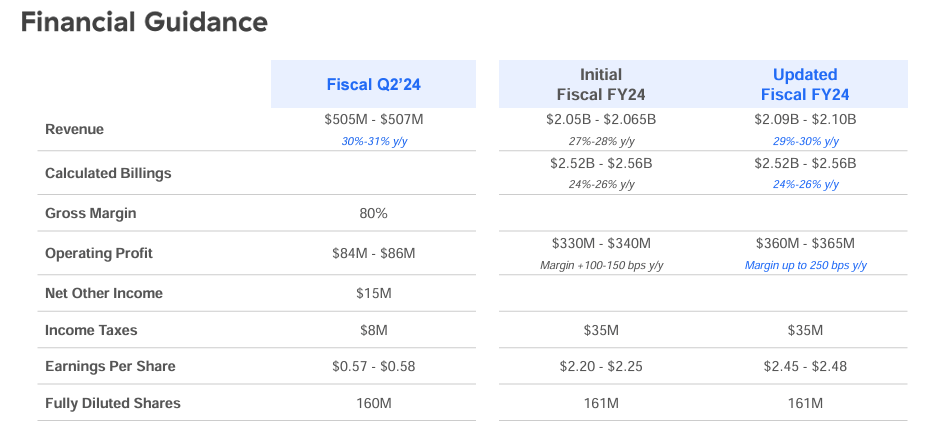

Additionally, Zscaler management positively revised the fiscal year 2024 outlook; the company now forecasts FY revenues from $2.09-$2.10B, up from the previous estimate of $2.050-$2.065B. We believe this adjustment indicates confidence in continued top-line growth; we think Zscaler is better positioned now to outpace the industry average growth rate. For the upcoming 2Q24, Zscaler projects revenues between $505M and $507M. We think it's only prudent that ZS management is more conservative in its outlook considering the current macro reality. We think the company should be able to beat its guidance for next quarter or be in-line with the mid-point of guidance; we think the more conservative outlook is due to fears of slower deal cycles with macro uncertainty. Still, we think the new guidance is realistic and should be well within reach. The following outlines Zscaler's financial guidance for FY24 and the next quarter.

{kind=link}

1Q24 earning results

As the industry workloads move to the cloud, the company's ability to secure growing cybersecurity spending will be a testament to its robust product offerings and market relevance. We expect Zscaler to continue to gain cybersecurity spend wallet share as more customers' workloads move to the cloud. We expect large deals that were previously on hold to resume in 1H24.

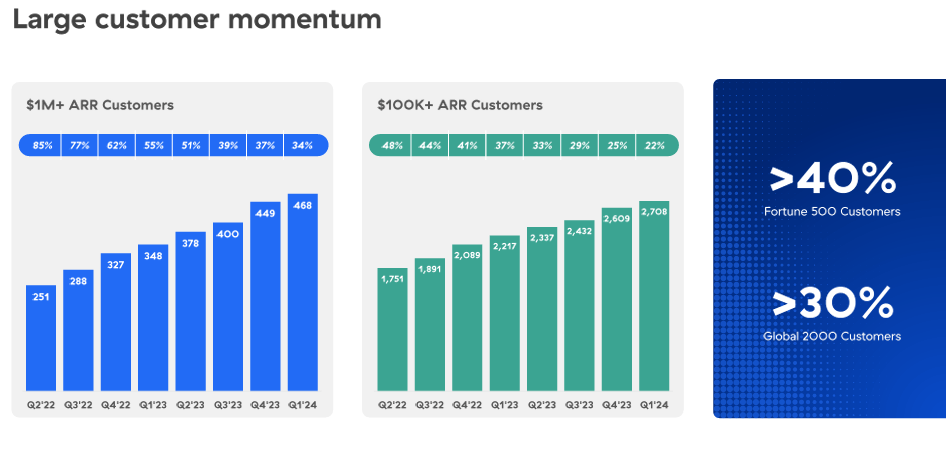

Below is a slide for the ZS earnings deck showcasing large customer momentum:

{kind=link}

1Q24 earning results

The core of Zscaler's competitive advantage lies in its early investment in AI and ML technologies, positioning itself as a leader in the expanding cloud security landscape. Additionally, we think the market opportunity in AI and Zero-Trust is big enough to encompass multiple players in the SSE market, including Microsoft ( MSFT ) and others. The Zero-Trust security market would grow at a 16.9% CAGR between 2023-2028. We think the company has a wide enough customer base to support its share expansion, including more than 40% of the Fortune 500 and 30% of the Global 2000 customers.

Valuation

Zscaler is trading above the peer group average; the stock is a high growth stock, in our opinion. The stock is expensive, but we think the growth rate for 2024 as the SSE opportunity expands justifies the higher multiple; we think there is fair value in the multiple as the market is pricing in future earnings that we expect in 2024. We believe Zscaler should be seen on an Enterprise to Value ratio; for CY24, the stock is trading at 11.8x EV/C2024 Sales compared to the industry average of 7.9x. On a Price-to-earnings ratio, Zscaler is trading for CY24 at 72.8x with an EPS of $2.64 versus the peer group average of 81x. We believe ZS is at the forefront of a large secular growth opportunity as architecture moves to the cloud in the SSE environment.

The below figure was made using Refinitiv data and outlines ZS's valuation.

TSP

Word on Wall Street

Wall Street shares our bullish sentiment on the stock. Of 43 analysts covering the stock, 31 are buy-rated, and the remaining are hold-rated. Using the median of the Wall Street price target of $210 and the mean price target of $207, we can calculate a potential upside of 8-9%.

The below outlines ZS sell-side ratings and price-targets.

TSP

What to do with the stock

We remain buy-rated on Zscaler; we expect the stock to outperform the S&P 500 and peer group through 2024. The stock is up 23% since our last note in mid-September, outperforming the S&P 500 by 21%. We expect Zscaler to continue to gain cybersecurity spend wallet share as more customers' workloads move to the cloud. We think the market is slowly waking up to Zscaler's potential, especially after its bounce back post-earnings last month. We think a unique window exists to buy the stock ahead of 2024. We continue to recommend investors buy the stock opportunistically.

For further details see:

ZScaler Q1 - Still BUY: Outperformance In 2024