ZS - Zscaler: Valuation No Longer As Attractive (Rating Downgrade)

2024-01-03 19:27:02 ET

Summary

- Zscaler's stock soared in 2023, as it rode the cybersecurity trend of zero trust.

- The company remains well-positioned for growth in the cybersecurity market, with ample opportunities for growth within existing clients, as well as adding new customers.

- However, after its surge in price in 2023, the stock is looking close to fairly valued.

Back in June , I initiated coverage on Zscaler ( ZS ) with a “Buy” rating, saying that despite a potential economic slowdown, the company had plenty of room to grow and that its valuation at the time was attractive. The stock has soared over 65% since that write-up, compared to a 14% gain in the S&P over the same time period. I last wrote about the stock in July , arguing the stock was attractively valued given its growth and that the threat of Microsoft’s ( MSFT ) new security solution was likely overstated. The stock has been up over 50% since then.

Given the huge gains in the stock since I last wrote about it, let’s catch up on the name.

Company Profile

As a reminder, ZS is a cloud security provider that offers three main products: Zscaler for Users, Zscaler for Workloads, and Zscaler for IoT/OT.

With Zscaler for Users, clients can provide their employees with secure access to the internet and apps through its Zscaler Internet Access, or ZIA, solution. The offering also provides Zero Trust Network Access (ZTNA) to internally managed applications with its Zscaler Private Access (ZPA) solution. This solution allows users to gain access to an app without revealing their identities or locations. Through its Zscaler Digital Experience or ZDX, customers can also enhance their users' end-to-end experiences by locating where in the network path an issue is occurring and how it is being caused.

Zscaler for Workloads, meanwhile, protects workloads using its ZIA and ZPA solutions, while Zscaler for IOT/OT delivers zero trust security for connected IoT and OT devices.

ZS’s revenue largely comes from the sale of subscriptions that allow users to access its cloud platform. Pricing is based on the number of solutions chosen (such as ZIA, ZPA, and ZDX) and a number of users or workloads.

Looking Towards 2024

Cybersecurity continues to remain a key area of spending for organizations, as the number of cyber-attacks only keeps growing. Going into 2024, zero trust security, the area where ZS plays continues to be one of the top trends in the space. High profile attacks on casino operators MGM ( MGM ) and Caesars ( CZR ) as well as at rival cybersecurity firm Okta ( OKTA ) only brought more attention to this area.

While zero trust gained a lot of momentum in 2023, expect it and overall SASE (secure access service edge) solutions to continue to converge in 2024 and be a top priority for organizations going forward. Gartner earlier predicted that at least 70% of new remote access deployments would serve predominantly by ZTNA as opposed to VPN services by 2025, so expect the momentum to continue in this space.

Also buoying cyber security in 2024 will be new SEC reporting rules . Companies will now be required to disclose material cybersecurity breaches 4 business days after they are determined to be material. In addition, companies will be required to provide material information regarding their cybersecurity risk management, strategy, and governance on an annual basis. These new rules are likely to prioritize cybersecurity even more for company boards and c-suites given the increased scrutiny from the SEC and more required disclosures.

Looking ahead to fiscal 2024 for ZS, the company projected revenue of between $2.09-2.10 billion when it reported its fiscal Q1 results . That would equate to growth of about 30%. That’s already up from its original revenue guidance for revenue of $2.05-2.065 billion. For 2023, the company grew revenue a robust 48%. It started out its fiscal year reporting revenue growth of 40% to $496.7 million for FQ1 ended October 2023.

ZS guided for adjusted EPS of between $2.45-2.48, up from an initial outlook of $2.20-2.25. It reported adjusted EPS of $1.79 in 2023, so that would be an increase of about 38% at the midpoint.

The company is looking for full-year calculated billings of between $2.52-$2.56 billion. That is the same as its original guidance. In fiscal Q1, calculated billings grew 34% to $456.6 million.

Looking at some other important metrics, the 12-month trailing dollar-based net retention rate was 120%. That was similar to the 121% it reported for 2023. ZS also added 19 new customers with an ARR of $1 million or more, bringing the total to 468 customers. A year ago, it had 348 such customers.

Discussing its upsell and new customer opportunity at a UBS conference at the end of November, CEO Jay Chaudhry said:

"About half of our new logos, I think it is new logo this quarter came from what we call Zscaler for Users bundle. These kind of user bundles combine ZIA, ZPA, ZDX, all 3 things together. We have felt that every customer we have, every user should have those. We are getting there. That's the platform expansion. Then data protection on top of that is a massive opportunity for us. We think we're clicking into data protections. If you ask me, where are the big product areas for growth, Zscaler for Users, which takes everything. I have a large installed base that's still only the ZIA. ZPA is sitting somewhere in the 60% penetration of large customers. But the ZDX, Zscaler Users an upsell opportunity for existing customers and then new logo. That's one. Data protection is sizable. I think we said it was approaching $0.25 billion that at the end of Q4. ... The number has exceeded $0.25 billion. That's good. And the third is emerging all products. Emerging Products, the workload communication side of it, the new products coming to the Risk-360 side of it.”

ZS has often discussed the huge opportunity it has selling into its own customer base, noting it has a 6x upsell opportunity on ZIA and ZPA alone with existing customers. So far, upselling remains an area of strength for the company. Given where cybersecurity trends are heading, I would expect this to be an area of continued growth for the company, as more customers adopt ZPA, ZDX, and other modules.

When it comes to risks, evolving technology is one of them. While ZS has benefited from being a cybersecurity tech leader, the cybersecurity landscape continues to involve how AI will play a role in the future, and how the incumbents react will be both an opportunity and a risk.

The economy and workforce reduction are another risk, as ZS often gets paid on a per user basis. Thus, less workers could mean less paying users as well.

Valuation

SaaS companies are generally valued based on a sales multiple given their high gross margins and the companies wanting to pump money back into sales and marketing to grow.

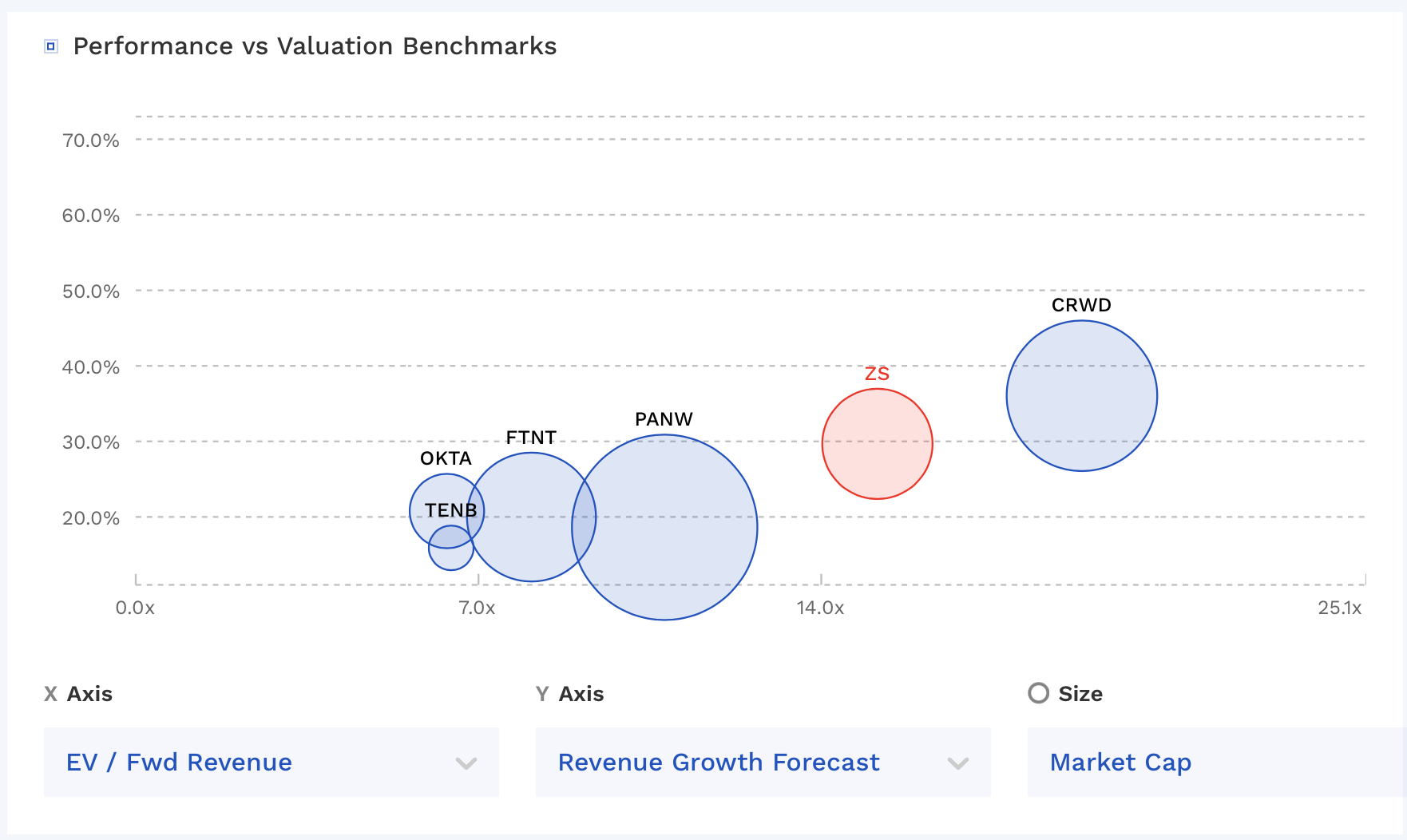

ZS is projected to generate $2.11 billion in revenue in fiscal 2024 (ending July) and $2.64 billion in fiscal year 2025. It trades at EV/sub revenue multiple of 14.4x and 11.5x, respectively.

Revenue is projected to grow nearly 30% this fiscal year and 25% next year.

ZS Valuation Vs Peers (FinBox)

{kind=link}

ZS currently trades towards the upper end of other cybersecurity firms. It and CrowdStrike ( CRWD ) command premiums given their stronger growth.

Given its 25-30% growth rate, ZS should be able to command between a 10-15x EV/S multiple. Based on FY25 revenue projections, which would place a fair value of between $194-$283. The midpoint is $238.50.

While I did not give a target previously, this valuation range would be higher than my prior expectations when I would have used a slightly lower multiple on 2024 revenue (given lower growth expectations of 20-25%), versus now using 2025 revenue and higher growth expectations. Thus my prior expectation would have been for a target of around $180 when I first wrote about it when it was trading near $130.

Conclusion

ZS has been doing a nice job growing within its existing user base as well as adding new customers. Net dollar retention would be a key metric I'd continue to monitor, as while it remains strong, it has dipped a bit from the 125%+ level it was prior. That said, current cybersecurity trends still bode well for the company in 2024. Expected ZTNA and SASE to remain hot in 2024 and for ZS to be a prime beneficiary as one of the top companies in this cybersecurity niche.

That said, given its strong performance, ZS is no longer as attractively priced as before. As such, I’m going to take the stock to “Hold.” My target is $240.

For further details see:

Zscaler: Valuation No Longer As Attractive (Rating Downgrade)