ZUO - Zuora: A Pioneering Force In The Subscription Management Space

2023-07-27 08:26:52 ET

Summary

- Zuora, Inc. is a leading player in the growing Subscription Management product market.

- The company's competitive edge lies in its ability to handle complex billing scenarios, successful integrations, and a dynamic platform that adjusts billing and cash collection in near-real time.

- The stock is trading at a valuation of 2.8x, making it an attractive investment opportunity.

Thesis

Zuora, Inc. ( ZUO ) has established itself as an early leader in the emerging Subscription Management product category. The Subscription Economy is experiencing significant growth, and effectively managing this business model requires a modern application approach with unique functionalities beyond traditional ERPs. Zuora has been at the forefront of this transformative shift and is well-positioned to capture a substantial portion of the TAM. Despite its strong growth potential, Zuora's valuation is attractive, trading at an EV/revenue multiple of 2.8x to the FY2024 estimate, making the stock an appealing investment opportunity.

Q1 2024 Review and Future Outlook

The management has highlighted that the macroeconomic conditions remain stable and consistent, aligning with the commentary from the Q1 earnings call. The existing pipeline supports the company's guidance for 12-15% Annual Recurring Revenue ((ARR)) growth for FY24. There is also a possibility that the ARR guidance is somewhat conservative, leaving room for potential improvements in the economy throughout the year. Furthermore, the comps for Net Revenue Retention (NRR) and ARR growth in Q4 are expected to be more favorable.

The company's gross retention rates are at record levels due to two key factors. First, the sales team has been successful in identifying prospective customers that align with the company's ideal customer profile in the enterprise market. Second, product innovation has significantly contributed to high customer satisfaction. Unlike in the past, where churn occurred due to selling to customers that didn't fit the ideal customer profile, the current cycle demonstrates the platform's stickiness and mission-critical nature, leading to improved gross retention.

The integration with Snowflake has been well-received by customers, and they can continue using this SKU, even with the Zuora Data Warehouse, including the BYOW release. The main difference for customers with the new warehouse product is that it enables data display and visualization within the Zuora User Interface, eliminating the need to export data and use external tools like Tableau or Power BI. Overall, Zuora's steady growth, focus on ideal customer profiles, product innovation, and successful integrations have contributed to its impressive performance in the market.

{kind=link}

Zuora's Competitive Position in the Market

Many have wondered why ERP vendors have not developed functionalities similar to Zuora Billing. While SAP Hybris BRIM is a competitive solution, it has not achieved the global traction that Zuora has. SAP's platform performs well in Europe with existing SAP customers and supports consumption-based billing, but Zuora has introduced novel and crucial features. For instance, Zuora can handle complex billing scenarios, like mileage-based pricing for services such as Zip Car, while SAP currently lacks support for certain functionalities, especially in prepaid credit-based models like Snowflake.

Snowflake's architecture involves customers buying prepaid credits called "Snowflakes" for a specific period, allowing them to draw down on that figure. However, this model adds significant complexity, and I believe that SAP's current platform does not fully support this functionality. Consequently, the impact of these new payment methods, both on billing and revenue recognition, creates challenges for traditional or custom ERP systems, which has been a driving force for the adoption of Zuora.

The broader question remains: why don't ERP vendors explore subscription billing more deeply? The primary reason is that ERP platforms are primarily designed to manage one-time transactions, supply chain processes, and accounting. Particularly for SAP customers heavily involved in manufacturing, this dynamic becomes crucial for managing their businesses and the complexities of manufacturing. In contrast, Zuora excels in managing subscriptions, as seen in its partnership with Zoom, where constant seat adjustments, varying spending levels, and cross-selling of products with similar complexity significantly impact revenue recognition. Traditional ERP systems' linear processes fall short in effectively managing the dynamic quote-to-cash process that subscription-based businesses require.

Zuora stands out with its dynamic platform that can adjust billing, cash collection, and other aspects of the quote-to-cash process in near-real time. Its "event-based rating agent" enables the platform to respond to real-time subscription changes, ensuring continuous revenue recognition for its customers. In the competitive landscape, SAP Hybris remains Zuora's primary competitor on a global scale in the billing domain. On the CPQ (Configure, Price, Quote) side, Salesforce's ( CRM ) offering, formerly known as SteelBrick, is the most common competitor. Other secondary competitors include Aria Systems, Gotransverse, and Chargebee.

Zuora's innovation is a key factor in maintaining its leadership in the enterprise market, which is the company's primary focus. A significant portion of Zuora's revenue, around 95%, comes from approximately 773 customers spending over $100,000 annually. While Zuora's position remains strong, it must keep an eye on emerging vendors like Chargebee, whose potential for product parity with Zuora could enable them to address businesses with revenue under $100 million.

{kind=link}

Valuation

I am impressed with the cost-saving measures taken by Zuora while awaiting an improved macroeconomic environment. Over the past few years, Zuora has undergone a product and platform transformation, which has enhanced its competitive positioning. In terms of competition, I don't see SAP, Oracle ( ORCL ), or Salesforce as significant threats to Zuora. These companies are likely to focus on their core competencies during this challenging period rather than directly competing with Zuora.

It is worth noting that Zuora has substantial exposure to the technology vertical, which has affected its growth. As investors evaluate Zuora's prospects, they should consider its potential as a steady grower. The company's increasing focus on profitability also indicates the possibility of scaling margins upon economic recovery. Zuora has retained sufficient quota-bearing rep capacity to manage a recovery, which should lead to solid operating leverage when the macroeconomic conditions improve.

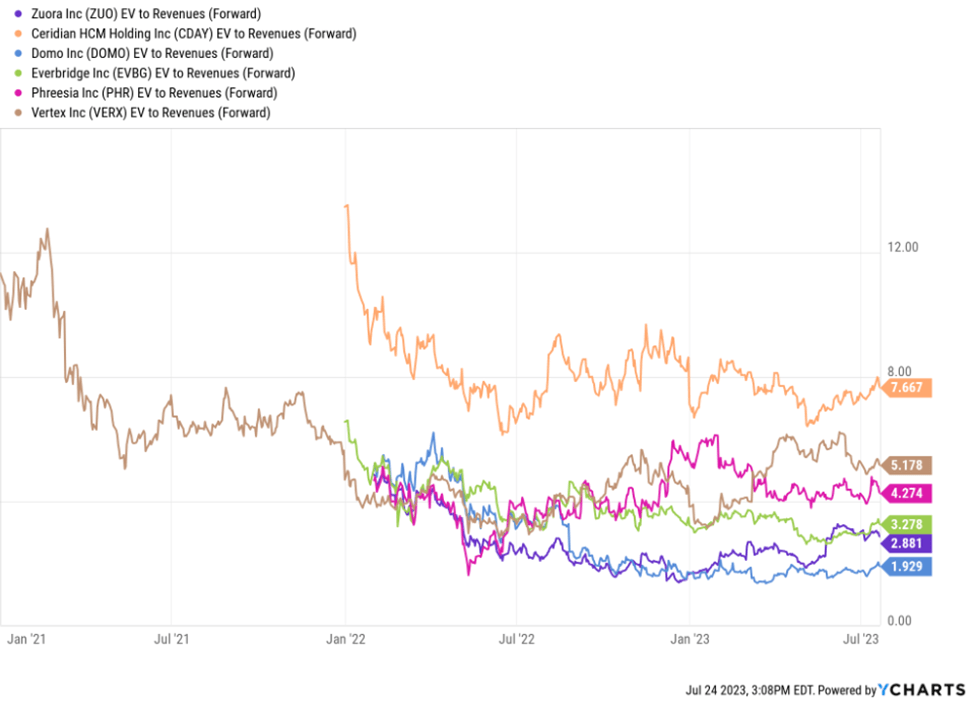

During the past 8 years, ZUO has traded at a median EV/Sales of 5.37x but is currently trading at a 2.8x EV/Sales, below its valuation comp. The comps serve enterprise customers with a primary focus on ERP-adjacent solutions similar to Zuora. While the comps, on average, are growing faster than Zuora, I expect the company's growth to accelerate and reach the same rate as these comparable vendors. I view the stock as a buy and have an end-of-year price target of $13 based on an EV/Sales multiple of 3x to the FY25 revenue estimate.

{kind=link}

Risks

Zuora's Software-as-a-Service (SaaS) delivery model allows customers to switch easily, leading to potential challenges in retaining customers if the company loses its competitive edge or faces operational issues. Moreover, while the subscription management software space has significant growth potential with a large and long-term TAM, however, I believe the market awareness remains limited. As a result, the industry sees longer than average sales cycles compared to other companies in the enterprise software universe. This limited awareness of product complexity often drives initial customer purchasing decisions towards custom, homegrown solutions rather than commercial solutions. Although I believe customers ultimately come back to commercial solutions, I believe this lack of awareness can create unpredictable sales cycles at times.

Conclusion

Zuora has established itself as the leader in the complex and evolving Subscription Management software space. The Subscription Economy is experiencing significant growth, and effectively managing this business model requires a more modern application approach with unique functionalities compared to traditional ERPs. With an attractive EV/revenue multiple of 2.8x, I see Zuora as a compelling investment opportunity at current levels.

For further details see:

Zuora: A Pioneering Force In The Subscription Management Space