ZUO - Zuora: Expect Growth With Expanding Margins Ahead

2024-01-16 04:57:24 ET

Summary

- Zuora's growth remains positive despite the macro condition, and its profit margin is expanding, indicating positive future earnings growth.

- The company has a strong pipeline of future revenue from contractual relationships, indicating potential for continued growth.

- Despite the current macroeconomic conditions, ZUO's performance and improving metrics suggest that the situation can only improve in the future.

Summary

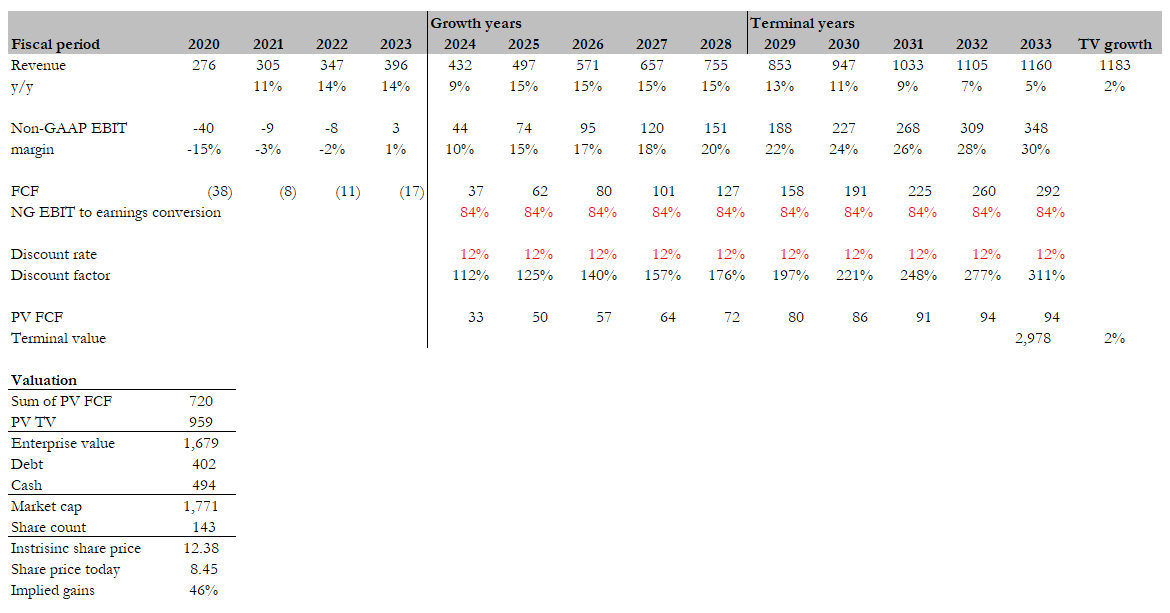

Following my coverage of Zuora ( ZUO ), which I recommended a buy rating due to my belief that ZUO can accelerate its growth as it finds success in pivoting its sales strategy, my expectation was that the new sales strategy would enable ZUO to acquire new customers even in a tough macro backdrop. As growth accelerates, valuation should follow through by re-rating upwards. This post is to provide an update on my thoughts on the business and stock. I continue to see ZUO as an attractive investment target as leading operating metrics continue to point to growth ahead. More importantly, ZUO has shown the market that its profit margin can continue to expand from here, which means earnings are going to grow much faster than the top line. Based on my long-term DCF model, my target price is $12.38.

Investment thesis

After my post last October, the stock rallied to ~$10, which I thought was a sign that the market has taken a positive view of ZUO's performance after its 3Q24 performance . I believe that ZUO is performing very well against my expectations, and I expect the stock price to gradually reflect my target price over time. In the recent 3Q24 quarter, ZUO revenue grew 9% organically, in line with my FY24 estimates, with subscription revenue growing 14% organically. ZUO's profitability also saw improvements, where gross margins expanded 660bps to 73.7%, and notably, subscription gross margins were up 200bps sequentially to 82.7%. As a result, non-GAAP EBIT margins were reported at 14.6%, a 580bps sequential improvement.

Two important metrics or factors that I believe point to growth ahead are:

- ZUO's total RPO (remaining performance obligation). In 3Q23, total RPO was up 20%, while cRPO (current remaining performance obligation) grew by 28%. For starters, RPO represents the total future performance obligations arising from contractual relationships. As the term suggests, I see these metrics as a proxy for ZUO's revenue growth potential if it doesn't acquire any new contracts. ZUO currently has an RPO of $554.9 million, which is more than 1x ZUO's LTM revenue run rate.

- ZUO won seven deals with an ACV (annual contract value) of at least $500k. This is great as it points to the continued successful execution of ZUO's new go-to-market strategy. Notably, ZUO also won two deals with ACV > $1 million, which management specifically called out because they continued to see strength.

The last part of the growth equation that has yet to recover is the macro condition, where management has made it clear that the macro has not improved and sales cycles remain extended. This might seem like a negative point, but I think given how ZUO has performed, it simply means that things can only go up from here once the macro situation recovers. While I am not a macro expert, I believe the fact that the Fed is leaning towards rate cuts is a good sign that the macro situation is at least moving in the right direction. Also, the fact that the net retention rate has improved sequentially from 107% in 2Q24 to 108% in 3Q24 makes me believe that the cycle might be in its first innings of turning around.

Aside from growth, I believe ZUO has demonstrated to the market that it is able to grow profitability even when times are tough. To reference again, non-GAAP EBIT margin improved by 580bps sequentially to an all-time high of 14.6%, and adj EBITDA margin expanded 600bps to 18.4%, an all-time high as well. The improvement in margins should be sustainable and not a one-off situation, as management has revised its FY24 non-GAAP EBIT margin guidance upwards to 10.2% from 8.1% previously. For FY25, management expects to exit the year at a "rule of 30" run rate, which means the sum of revenue growth and non-GAAP EBIT margin would be at least 30%. This is a huge guide, as it implies either growth will accelerate to 20% or non-GAAP EBIT margin will expand by a couple of hundred basis points over the next 2 years (assuming growth comes in as I expected, a low-to-mid-teens percentage).

Valuation

{kind=link}

My target price for ZUO based on my DCF model is $12.38. I have switched my model methodology from a relative one to a long-term DCF as ZUO profitability is on track to continue inflecting upwards from here. For the revenue line, my model assumes that ZUO can at least continue to grow in the mid-teens percentage level in the growth years, especially with the macro situation recovering eventually. After the growth years, growth should gradually taper to 2% in the terminal year (2% is the long-term inflation rate). However, because of ZUO's improving margin, growth at the non-GAAP EBIT and FCF levels is much better than top-line. Management guidance is for FY24 non-GAAP EBIT to come in at $44 million at the midpoint and FCF of $37 million. Using management guidance as a base, I am modeling non-GAAP EBIT margin to improve by ~100bps a year until FY28 as ZUO needs to balance growth and profitability, followed by continuous expansion to ~30%. I used 30% by comparing ZUO's financials to Salesforce.com ( CRM ), which is a much more mature software business and has a similar gross margin to ZUO. Given that ZUO is not a capital-intensive business that requires constant investment in CAPEX, I expect FCF to stay at very high levels (same as the FY24 guided level). As for discount rates, given the nature of ZUO in business (which is very exposed to macrocycles), I used a higher discount rate of 12% to reflect the risk.

Risk

The implicit assumption that I have made is that the macroeconomy will start to recover in the coming quarters. Suppose that is not the case, growth could remain sluggish, ranging from high single-digits to low teens. To support growth, ZUO might need to reinvest more than expected into sales and marketing, which could hinder the pace of margin expansion.

Conclusion

I remain positive about ZUO, as the business continues to grow as expected and profit margins are expected to continue inflecting upwards from here. This indicates that ZUO is successful in executing its sales strategy. Key indicators such as total RPO and significant ACV deals suggest that growth will continue to be positive from here. While macroeconomic conditions have yet to recover, I think the fact that ZUO is able to continue growing and expand margins means that things can only improve from here if macroeconomic conditions recover.

For further details see:

Zuora: Expect Growth With Expanding Margins Ahead