PCOR - Procore Technologies: Continuous Momentum In Growth

Summary

- PCOR is tackling an industry that is large and ripe for disruption.

- PCOR's comprehensive platform increases retention rate and opportunities for cross-selling.

- PCOR continues to see strong demand despite the weak macroenvironment.

Investment thesis

I recommend to invest in Procore Technologies ( PCOR ). The industry is extremely large which means the growth runway for PCOR should be long as well. More importantly, I think PCOR's product fits the requirements that users are demanding (as can be seen from its key metrics). While there might be some competitive factors at play here, from Autodesk ( ADSK ), I think the market is large enough to contain 2 or more players.

Business overview

PCOR offers construction management services via cloud. PCOR's platform streamlines complex workflows and promotes effective communication between all involved parties in a project in real time.

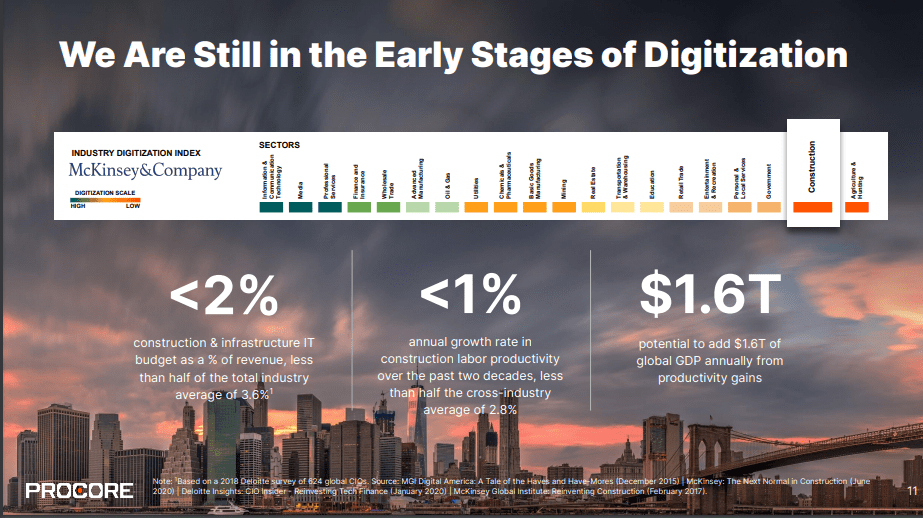

Construction is one of the largest industries but slowest to digitalize

Despite its size, the construction industry has been notoriously slow to adopt new technologies. One of the main reasons for this, in my opinion, is inherent obstacles that it needs to overcome when it comes to digitization that other industries did not. As such, I believe we are in the early innings of this wave. There is a huge window of opportunity to increase construction productivity because so many processes are still done manually and on paper, and because legacy software solutions have not been able to meet the needs of industry stakeholders.

{kind=link}

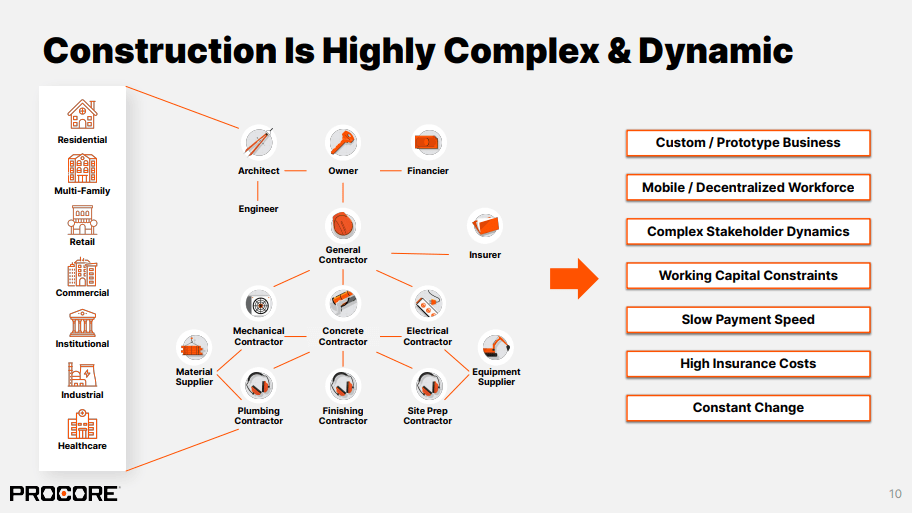

Furthermore, the industry is very fragmented, which makes digitalization more difficult. Coordination among disparate and specialized groups, such as those holding pivotal positions in the construction process, is essential. Change orders, which are requests to add, change, or discarding tasks from the agree design of a project, are a common and complex manifestation of the interdependencies between many stakeholders.

In order to finalize a change order, numerous parties are tasked with addressing a laundry list of tedious tasks and approving processes. Due to the many handoffs that must occur when working with legacy mediums such as paper for project management, even a seemingly straightforward change order can take days or even weeks to resolve. When there are many open change orders on a project, even a delay of a few days can mean weeks or months of additional work and schedule disruptions, not to mention the knock-on effects on resource availability and work sequencing.

Change order management is an example of the complexity and interdependence of construction projects as a whole, which makes it difficult to establish rapport between parties. Because of the system's complexity, its dependence on other parts, and the distrust among its stakeholders, disagreements arise frequently, and blame is often passed around. In my opinion, if all parties involved in an industry worked together more effectively and communicated openly, it would enhance the overall economic value of all stakeholders.

{kind=link}

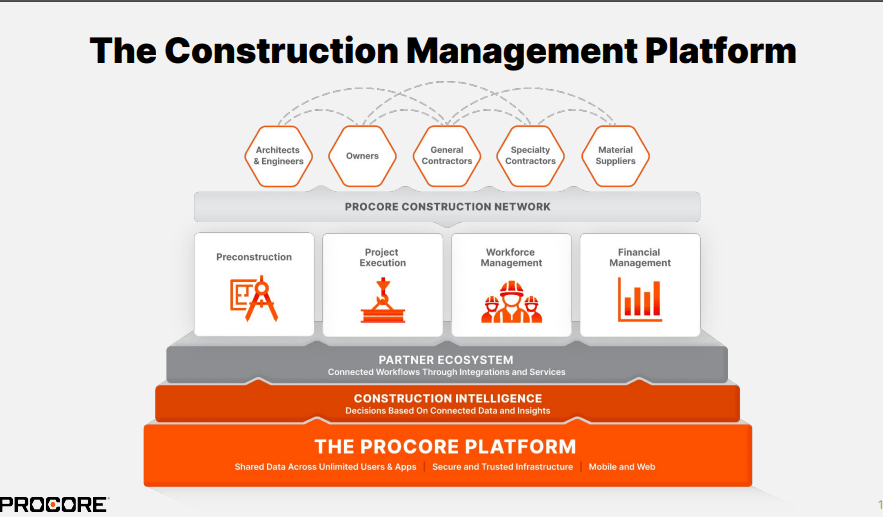

PCOR comprehensive platform is the antidote to this poison

Projects and information across many different workflows can be managed and shared centrally on the PCOR platform. End users can also gain data access provided by external parties and other stakeholders through PCOR products' integrations with external applications. The platform basically lets customers manage the entirety of a construction project's lifecycle. As a result, customers can expect a smoother UX and easier access to project data. Importantly, customers can manage projects and complete many routine tasks without switching between different applications when using products that integrate workflows across the entire project lifecycle.

{kind=link}

Rapid adoption strategy

PCOR's unlimited user model facilitates the rapid, mass take-up of the PCOR platform and assures the capturing of project information. In my opinion, this is an advantage in and of itself because solutions that charge per user prevent widespread adoption, meaning that only a select few people can view project data and that no data can be centralized. PCOR does not charge customers on a per-seat basis, instead basing product pricing on the number of products in use at once, product mix, and volume.

With this pricing structure, I believe PCOR can attract a large user base by making the platform accessible to anyone involved in a project, not just those who have opted to become paying subscribers. This creates a self-sustaining cycle, as contributors who like the platform may decide to become paying subscribers and contribute additional data.

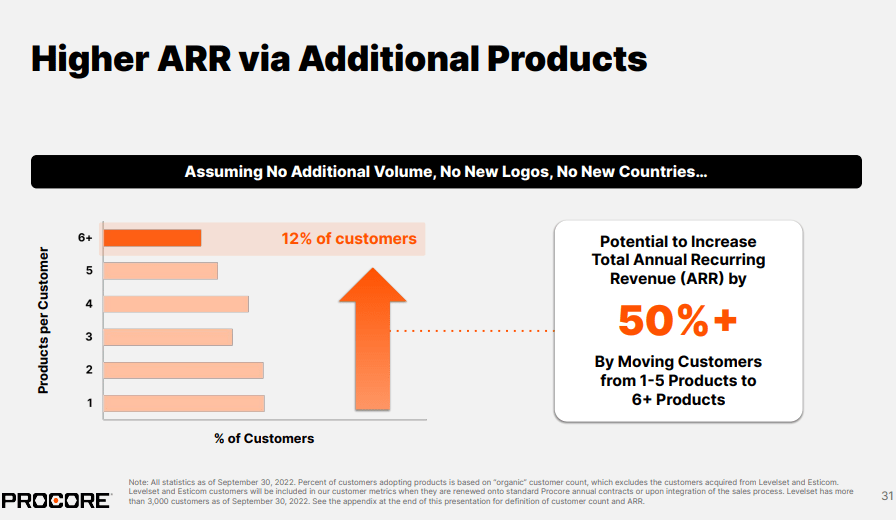

Cross-sell opportunities

Despite the growth of the PCOR platform, cross-selling opportunities have not fully matured. As was mentioned up top, Procore's functionality goes far beyond traditional project management thanks to the platform's app marketplace. I think this integration is crucial to PCOR's long-term success because it allows the company to extend its reach beyond its core customers. Even though slightly more than 40% of customers have adopted more than 4 modules (can go up to 6+), I believe there is still abundant opportunities remain for continued cross-sell within PCOR customer base.

{kind=link}

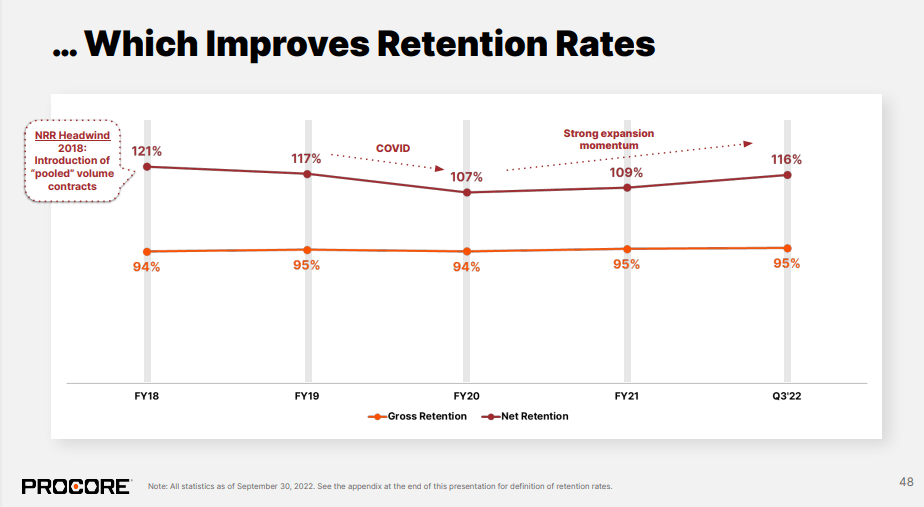

Retaining customers is another advantage of cross-selling and providing a full service offering. The reasoning is straightforward: as more and more people use a product, PCOR becomes ingrained in the process. This would indicate that PCOR platform adoption will increase as a result of increased usage by end users. All of these factors contribute to PCOR's increased stickiness. The numbers released by PCOR seem to support this reasoning as well.

{kind=link}

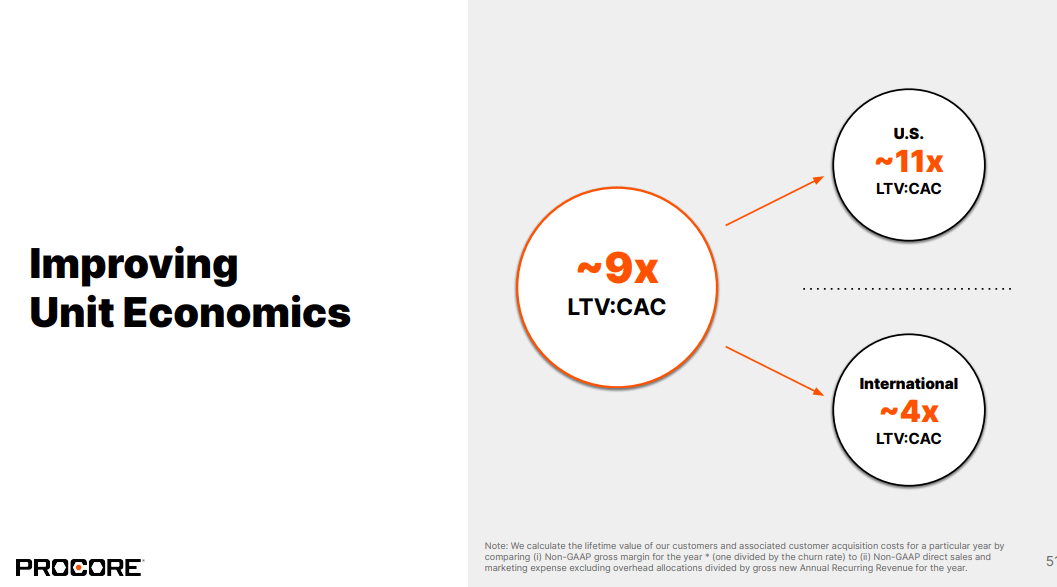

Attractive unit economics

PCOR should continue investing in anticipation of a large market opportunity, so I do not anticipate it becoming FCF positive anytime soon. However, I do anticipate that the company's upfront investments will eventually yield profits due to the company's strong unit economics, as evidenced by its high LTV/CAC ratio. The fact that PCOR has such a high customer retention rate is further evidence of the platform's vital importance to the company's success. Therefore, relatively high LTV should continue to be the result of a combination of low churn rates and healthy gross margins.

{kind=link}

Macro weak but demand remains strong

In addition to the increase in guidance in the third-quarter results, I believe it is important to highlight the strong expansion momentum and robust large-deal activity as core drivers of RPO outperformance in the third quarter. Management was also upbeat about the macro environment, citing healthy demand from all stakeholders and customers of all sizes through the third quarter as evidence. The length and variety of its end-customers' project backlogs were cited as potential buffers in a prolonged downturn, both of which are positives in my book.

Valuation

My model suggests PCOR is worth $79.79, if it trades at an 8x forward revenue multiple in FY24.

Model walkthrough:

- Revenue to follow management full year guidance in FY22. Afterwards, I expect revenue to continue growing at a similar pace but slightly lower due to a larger revenue base (but net revenue adds should grow).

- I have my belief that valuation could go up a lot higher than the 8x forward revenue PCOR is trading today. The catalyst would be PCOR accelerating growth (past my market expectations). That said, even at 8x forward revenue the possible upside is 47%.

Own calculations

Risks

Competition

It seems to me that ADSK, with its powerful adjacent product and channel distributors, poses the greatest threat among competitors. However, in my opinion, there is room for two dominant players in this market.

FCF burn

It's encouraging to see PCOR expanding rapidly, but the company needs to start generating positive free cash flow soon. Investors' tolerance for growth may wane much more quickly than anticipated, dragging down valuation, depending on the state of the market.

Conclusion

Considering the massive size of the industry, PCOR has a lot of room to expand. Also, I believe PCOR's product meets the needs of its target market, which is the crux of the entire thesis – PCOR is selling something that end users need. Although ADSK competition could be a factor, I believe this market is big enough for at least two major competitors.

For further details see:

Procore Technologies: Continuous Momentum In Growth